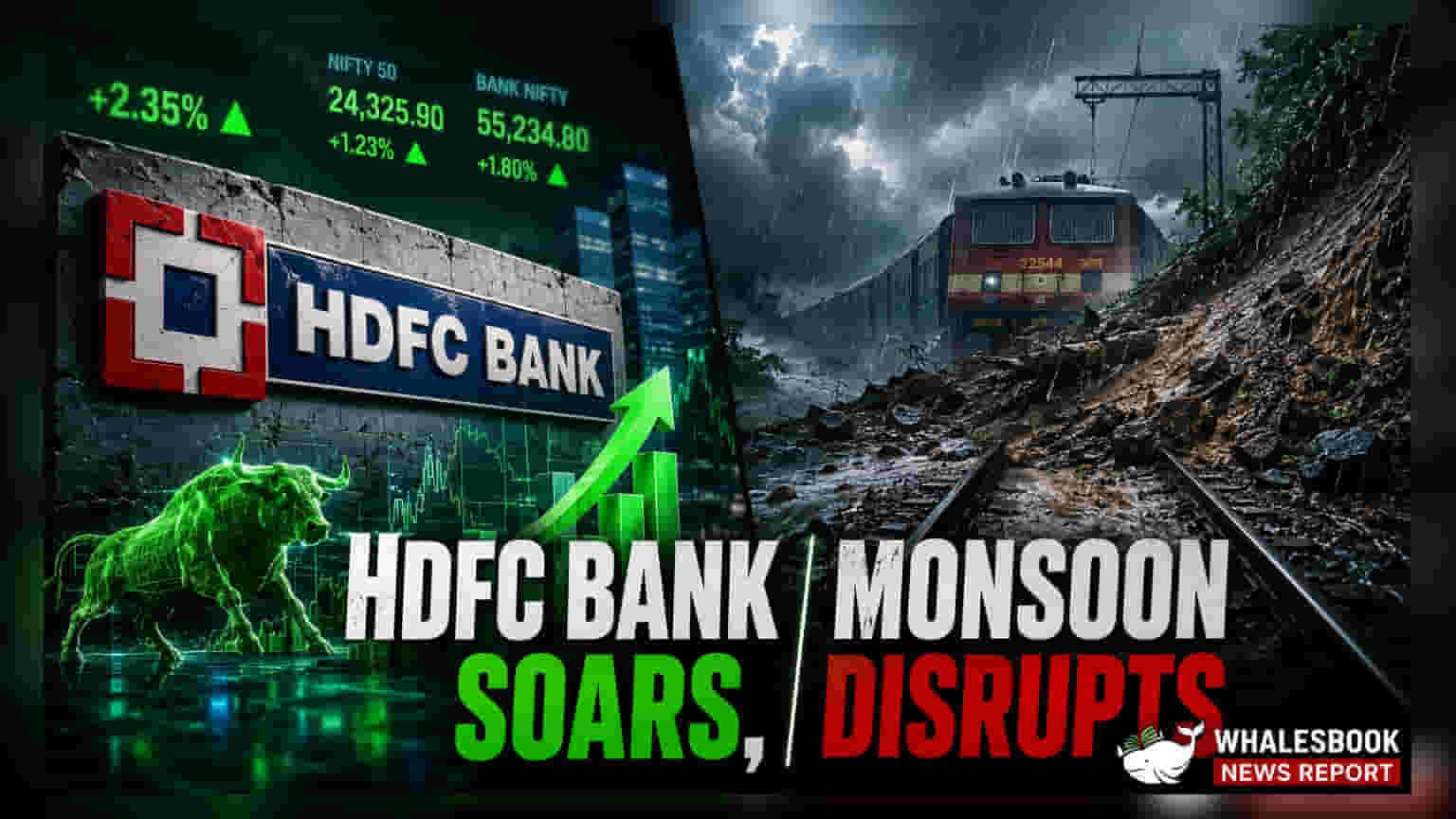

HDFC Bank reported loan and deposit growth for the June quarter that surpassed market expectations. This marks the private lender’s strongest performance in five quarters, signaling resilience in its lending operations. Investors will now watch for the upcoming full financial results to assess the impact of this credit growth on the bank's net interest margins.

HDFC Bank Ltd. has released its business update for the quarter ended June 30, 2026, showing a positive trend in its core operations. The lender recorded robust growth in both loans and deposits, a performance that exceeded analyst expectations and represents its fastest pace of expansion in the last five quarters. This growth indicates that the bank continues to attract significant credit demand even as the banking sector manages the broader economic environment.

For investors, the primary takeaway from this update is the volume of business expansion. HDFC Bank, which holds a significant share of the private banking market in India, relies heavily on consistent loan growth to support its earnings. While this update provides a clear view of the bank's business momentum, the next important step for shareholders will be reviewing the bank’s official quarterly financial results. These results will clarify how this loan growth translates into actual profit, specifically regarding the Net Interest Margin, which is the difference between the interest income earned on loans and the interest paid on deposits.

Historically, the bank has maintained a focus on balancing credit expansion with prudent asset quality management. Since its merger with the erstwhile HDFC Ltd., the bank has been working to optimize its balance sheet and integrate its mortgage business effectively. Ongoing monitorables include how the bank manages its liquidity and whether it can maintain competitive pricing on deposits to fund its lending activities.

In the broader sector context, private banks are currently navigating a competitive landscape where deposit mobilization remains a key priority to fund credit growth. HDFC Bank’s ability to meet these expectations in the June quarter serves as a barometer for the health of private credit in India. Investors should continue to monitor future disclosures regarding asset quality, specifically non-performing assets, to ensure that the rapid loan growth is supported by high-quality lending standards.