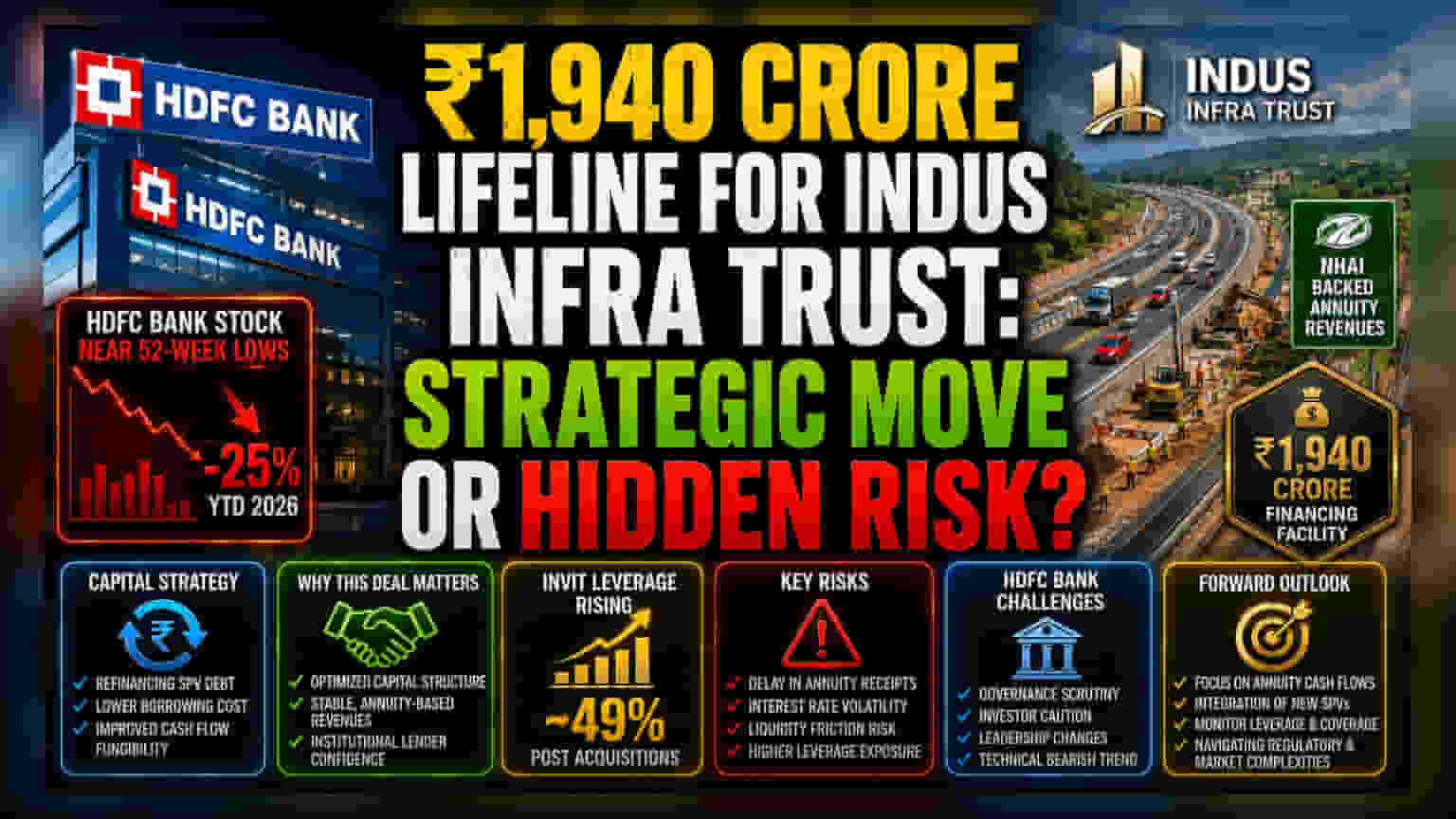

The Capital Strategy

The ₹1,940 crore financing facility extended to Indus Infra Trust underscores a calculated effort to optimize the financial structure of the trust’s newly acquired Special Purpose Vehicles. By refinancing existing, potentially higher-cost debt at the project level, the trust seeks to consolidate its obligations and improve long-term cash flow fungibility. This move aligns with broader industry trends where infrastructure investment trusts (InvITs) leverage their stable, annuity-based revenue streams—primarily backed by the National Highways Authority of India—to secure more favorable borrowing terms from institutional lenders.

HDFC Bank’s Infrastructure Positioning

This deal arrives as HDFC Bank continues to navigate a challenging fiscal period. With the bank’s stock currently trading near 52-week lows and facing significant investor caution—exacerbated by governance scrutiny and a broader pullback in domestic equities—the bank remains heavily active in the infrastructure debt segment. The lender’s participation in such substantial project financing reflects its strategy to maintain capital deployment in sectors deemed critical to India’s long-term economic growth. Despite technical indicators suggesting a bearish trend and consistent underperformance relative to its banking peers, the bank’s institutional focus on project finance continues to serve as a cornerstone of its credit portfolio.

The Forensic Bear Case

While this financing provides immediate relief for the Indus Infra Trust, it highlights the inherent dependencies of the infrastructure sector. The trust’s leverage, which is projected to rise toward 49% following recent asset acquisitions, remains a monitorable metric for risk-averse investors. Any delay in annuity receipts from the National Highways Authority of India—even if current records show timely payments—could create liquidity friction at the trust level. Furthermore, the reliance on refinancing as a tool for financial efficiency assumes a stable interest rate environment; a shift in macroeconomic policy could pressure the trust's coverage ratios. Investors should also note the broader context: HDFC Bank itself is currently contending with significant skepticism from the street, with analysts citing valuation concerns and recent leadership turnover as catalysts for the stock’s 25% decline year-to-date in 2026.

Forward Outlook

Market analysts remain divided on the near-term path for HDFC Bank, with some identifying deep-value opportunities while others emphasize the risks associated with current governance hurdles. For the infrastructure sector, the continued utilization of InvITs to recycle capital remains a key trend. As the trust integrates its new SPVs and manages this fresh tranche of debt, the focus for stakeholders will remain on the consistency of annuity cash flows and the bank’s ability to manage its exposure in an increasingly complex regulatory and market environment.