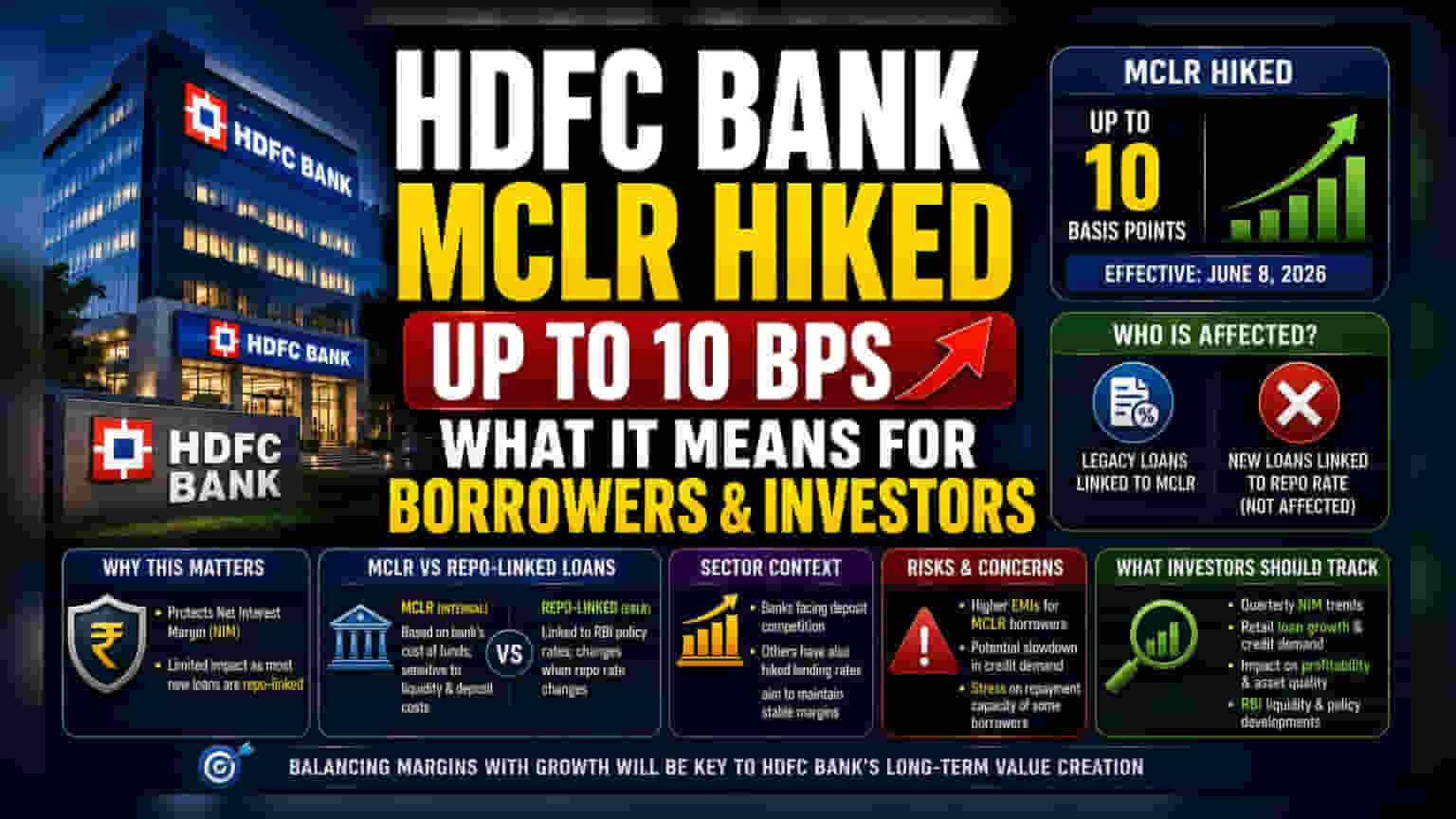

What Happened

HDFC Bank has implemented an increase in its Marginal Cost of Funds-based Lending Rate (MCLR) by up to 10 basis points across various tenures. This revision, which became effective on June 8, 2026, means that the interest rates for certain loan products will adjust upwards. The bank periodically reviews its MCLR to align with its internal cost of funds and broader liquidity conditions in the banking system.

Why This Matters For Investors

For shareholders and market observers, this move is a reflection of how the bank manages its Net Interest Margin (NIM), a critical profitability metric for lenders. When banks face competition for deposits or see shifting liquidity, they may adjust lending rates to protect their interest income. This specific hike is targeted at legacy loan accounts, as most new retail loans in the Indian banking system are now linked to external benchmarks, such as the repo rate, rather than the internal MCLR. Consequently, the immediate impact on the bank's overall lending portfolio is limited to the subset of borrowers still tied to the older MCLR framework.

Understanding the Lending Benchmark

It is important for investors to distinguish between the two types of loan pricing mechanisms currently in use. The MCLR is an internal benchmark that considers the bank's own cost of funds. Because it is internal, it tends to be more sensitive to the bank's liquidity and deposit cost situation. In contrast, loans linked to the External Benchmark Lending Rate (EBLR) are directly tied to the Reserve Bank of India’s policy rates. This means that while existing borrowers on MCLR-linked loans will see their Equated Monthly Instalments (EMIs) or loan tenures adjust following this hike, those with newer, repo-linked loans are not directly affected by this specific change.

Sector and Competitive Context

This recalibration of lending rates is not unique to HDFC Bank and is part of a broader trend within the Indian banking sector. Several banks have been navigating a period where deposit growth has been a key priority. When banks face pressure to attract deposits, the cost of funds can rise, often prompting lenders to increase their benchmark lending rates to maintain stable profit margins. Comparing this to peers, other large lenders have also taken similar measures in recent months to ensure their lending rates remain in sync with the costs they incur to source funds from depositors.

Risks and Concerns

While raising rates helps protect profit margins, it does carry business risks. The primary concern for investors is whether higher borrowing costs could dampen credit demand. If lending rates rise too sharply or stay elevated for too long, retail and corporate borrowers may delay new loan applications or look for alternative financing options. Furthermore, persistent high interest rates can occasionally lead to stress on the repayment capacity of more vulnerable borrower segments. Investors should be mindful that the bank needs to find a balance between passing on funding costs to protect its margins and maintaining competitive rates to ensure healthy loan book growth.

What Investors Should Track

Moving forward, the key monitorable for investors is the bank's quarterly performance regarding its NIMs. Shareholders will be watching to see if these adjustments effectively shield profitability against the backdrop of deposit competition. Additionally, monitoring the bank's commentary on credit demand and the overall growth of the retail loan book will be essential. If the bank manages to maintain strong loan growth despite these rate adjustments, it would indicate a resilient market position. Keeping an eye on any future, sector-wide shifts in lending benchmarks or liquidity management strategies by the Reserve Bank of India will also provide necessary context for the bank's future rate decisions.