A new Crisil Ratings report finds that Indian gold loan companies are well-protected against potential gold price drops. Despite regulatory rules allowing for higher loan-to-value limits, lenders have maintained conservative internal policies, keeping credit losses minimal even during market volatility.

What Happened

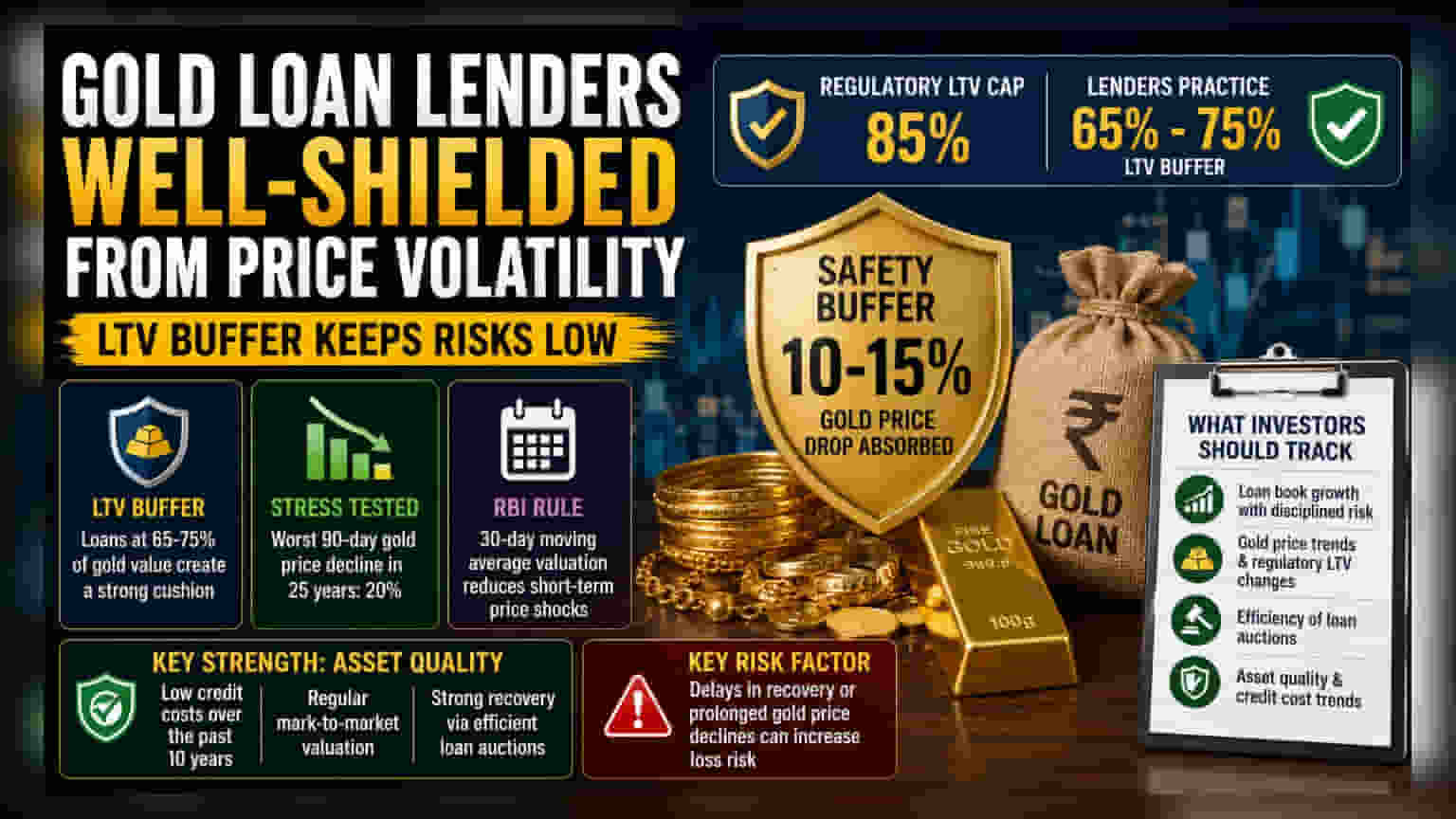

A new report by Crisil Ratings suggests that domestic gold loan lenders remain well-shielded from risks related to gold price volatility. Even though regulators recently increased the allowable loan-to-value (LTV) cap to 85%, lenders have continued to follow more conservative practices, typically lending between 65% and 75% of the gold's value. This gap provides a safety cushion for lenders if gold prices were to fall suddenly.

Why The LTV Buffer Matters

For investors, the core strength of these companies lies in their asset quality. When a customer takes a loan against gold, the lender calculates how much money to give based on the gold’s market value. By lending only 65-75% of the value, the lender creates a 'buffer.' This means even if gold prices drop by 10% or 15%, the value of the collateral remains higher than the loan amount.

Crisil’s analysis, which stress-tested 25 years of daily gold prices, showed that even during sharp market downturns, the worst price decline in a 90-day window was 20%. Because lenders use a 30-day moving average to value gold—a method mandated by the Reserve Bank of India—they are less affected by sudden, short-term shocks in gold prices.

The Risk Factor

While the sector is generally protected, the risk to the business model does not disappear entirely. The primary challenge for gold loan lenders is the timely recovery of loans. If a borrower defaults, the company must auction the pledged gold to recover the dues. The effectiveness of this process depends on how quickly and accurately the company can value the gold and execute the auction. If gold prices crash and stay low for a long time, or if auction processes are delayed, the risk of loss on individual loans increases.

Sector and Business Context

Companies in this space, such as Muthoot Finance and Manappuram Finance, have expanded their loan books significantly in recent years. Their ability to manage risk has been a key factor in their financial stability. Over the past decade, credit costs—the money set aside for bad loans—have remained low. This success is largely due to regular mark-to-market valuations, where lenders check the value of the pledged gold against current market rates frequently.

What Investors Should Track

Going forward, the performance of gold loan companies will depend on a few key factors. Investors should watch the growth of their loan portfolios, as companies try to balance higher growth with strict risk controls. Additionally, any significant change in gold price trends or shifts in regulatory LTV policies will be important. Finally, monitoring how efficiently these firms handle loan auctions during periods of price pressure will provide insight into their operational strength.