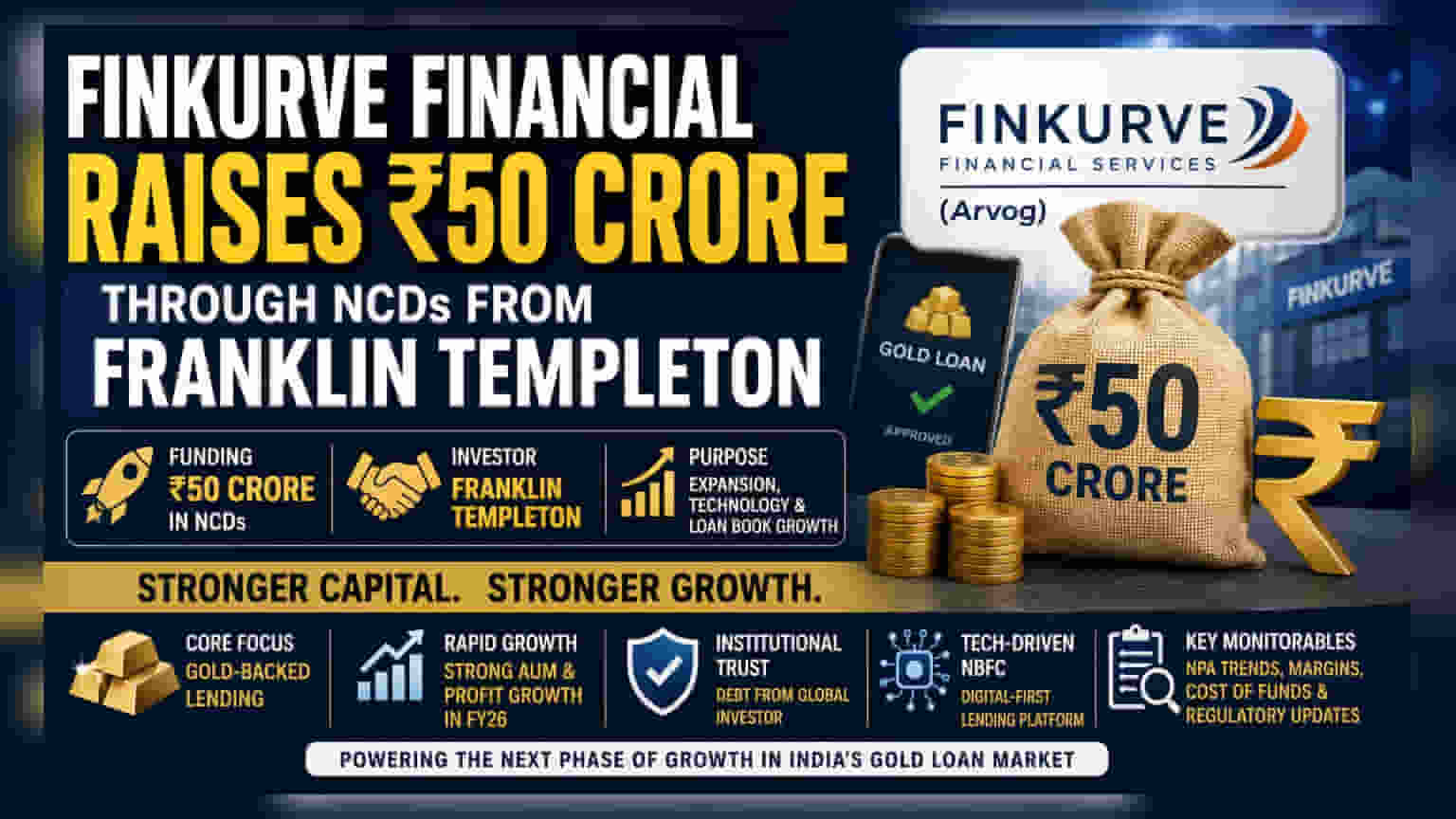

Finkurve Financial Services has secured ₹50 crore through a Non-Convertible Debenture (NCD) issuance from Franklin Templeton to fuel its gold loan business expansion. This capital infusion arrives as the NBFC continues to scale its operations amidst competitive pressures and evolving regulatory standards in the lending sector.

What Happened

Finkurve Financial Services Limited, a technology-driven Non-Banking Financial Company (NBFC) also known by its brand name Arvog, has raised ₹50 crore through the issuance of Non-Convertible Debentures (NCDs) to Franklin Templeton. The funding is structured in two tranches, with an initial ₹24 crore already secured. This capital is earmarked to support the company’s expansion plans, enhance its technology platform, and grow its loan book, particularly in its core segment of gold-backed lending.

Why It Matters For Investors

For shareholders and market observers, this funding serves as a significant liquidity event. By securing debt from a global institutional player like Franklin Templeton, Finkurve aims to strengthen its balance sheet and diversify its borrowing sources. In the NBFC sector, the ability to raise long-term capital at competitive terms is often viewed as a signal of institutional trust in the company's business model and risk management practices. This capital will likely be deployed to scale the company's co-lending model and increase its footprint in both new and existing territories.

Financial And Business Context

Finkurve operates as part of the Augmont Group, leveraging an integrated gold ecosystem to provide asset-backed credit. The company has been in a phase of rapid expansion, with recent filings showing significant growth in Assets Under Management (AUM) and net profit in the fiscal year ending March 2026. However, this growth has been heavily supported by debt, with the company utilizing various borrowing instruments including term loans from banks and NCDs to finance its lending operations. The company's business model is centered on a digital-first approach to gold loans, which faces intense competition from both large banks and established gold loan NBFCs.

The Risk And Regulatory Landscape

While the capital injection provides immediate support, investors should remain aware of the risks inherent to the NBFC sector. Credit rating agencies have previously noted that while Finkurve maintains adequate capitalization, its operations are subject to regulatory risks, particularly concerning its personal loan segment and the broader, evolving regulatory framework governing NBFCs in India. Furthermore, aggressive loan book expansion funded by debt can put pressure on margins and liquidity if not matched by strong asset quality. The company’s resource profile remains moderately diversified, but maintaining a healthy cost of funds is crucial for protecting net interest margins in a competitive lending environment.

What Investors Should Track

Looking ahead, the key monitorables for investors include the utilization of the remaining tranche of the ₹50 crore facility and any updates on the company’s cost of borrowing. Investors may also track the company's quarterly performance for signs of sustainable margin growth, trends in Gross and Net Non-Performing Assets (NPAs), and adherence to evolving RBI guidelines. Management commentary regarding the integration of new capital and the company’s ability to manage its debt-to-equity ratio will be essential for understanding the long-term impact of this funding on shareholder value.