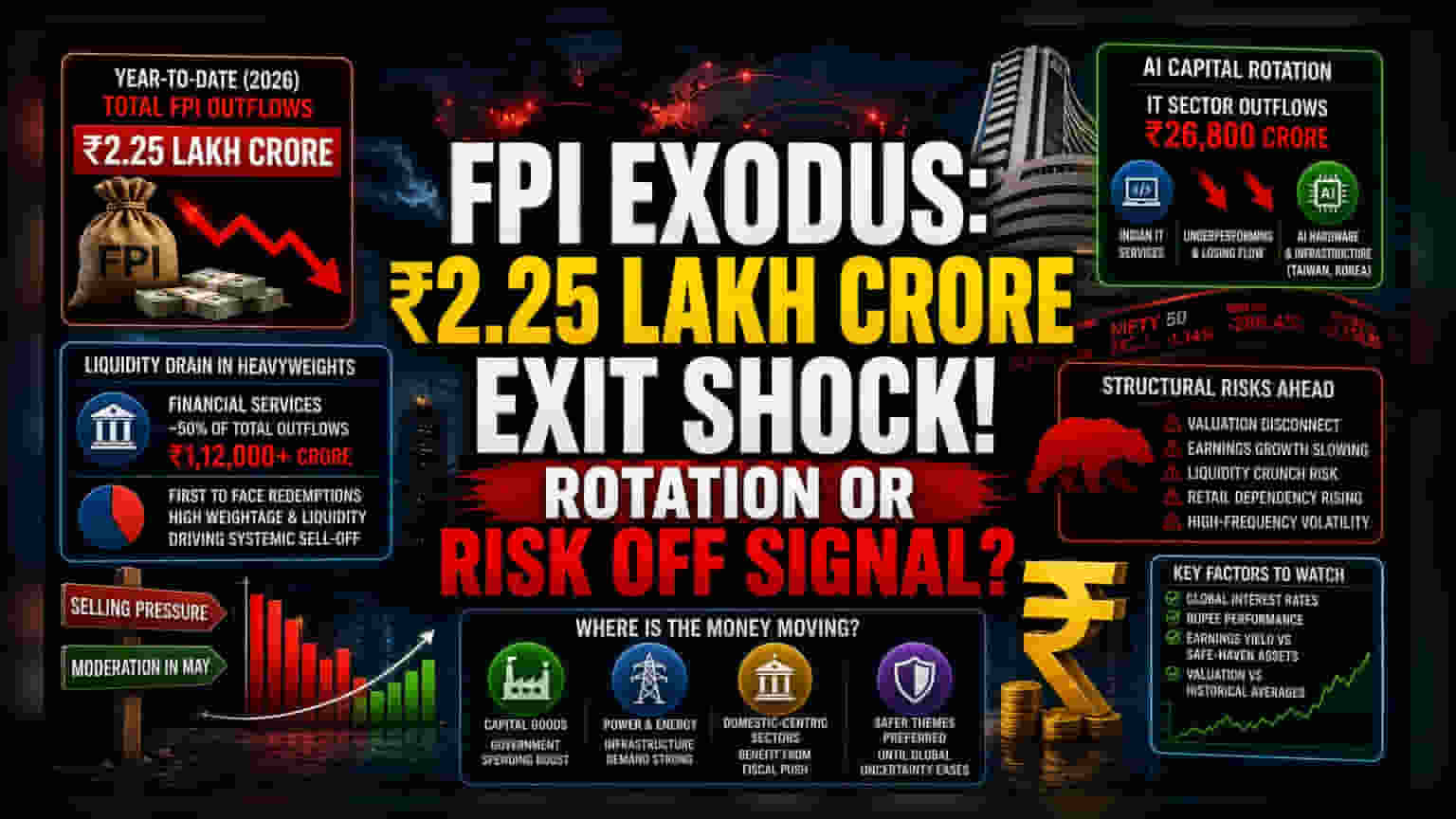

The Liquidity Drain in Heavyweights

The exodus from Indian financial services, which accounted for roughly half of the total ₹2.25 lakh crore in year-to-date outflows, is not merely a reactionary sell-off but a significant portfolio rebalancing act. Financials traditionally serve as the proxy for the broader Indian economy in international portfolios. When institutional sentiment sours, these stocks are the first to face the brunt of redemptions due to their liquidity and high weightage. The systematic nature of these sales suggests that major global funds are reducing their beta exposure to the Indian market, favoring regions with lower interest rate risk or higher direct exposure to the current generative AI hardware cycle.

The AI Capital Rotation

The IT sector’s underperformance, marked by ₹26,800 crore in outflows, stems from a fundamental disconnect between Indian service-oriented IT models and the capital-intensive infrastructure requirements of the global AI race. While Indian firms grapple with margin compression and the slow adoption of proprietary AI agents, global capital is migrating to semiconductors and cloud infrastructure providers in Taiwan and South Korea. This shift reflects a tactical preference for firms that own the physical bottlenecks of AI production rather than those providing tertiary software implementation services. This reallocation suggests that global allocators no longer view Indian IT as a high-growth hedge but as a stagnant asset class ripe for pruning.

Structural Risks and the Valuation Trap

The Bear Case rests on the persistent valuation disconnect in the domestic market. Despite the market correction, many Indian financial and consumer staples companies maintain price-to-earnings multiples that appear increasingly disconnected from their recent earnings growth trajectories. Historically, when FPIs reduce exposure at this pace, they do so not just to book profits, but to escape potential liquidity crunches in emerging markets. The domestic institutions (DIIs) have largely absorbed the selling pressure, but this creates a dependency that may struggle to sustain if the retail participation rate experiences a seasonal or trend-based dip. Furthermore, the reliance on high-frequency, algorithm-driven trading in the financial sector exacerbates volatility, making price discovery more difficult for long-term investors.

Assessing Future Inflows

Market participants are now monitoring the delta between current valuations and historical long-term averages to identify potential re-entry points. While the moderation in selling during May provides a glimpse of stabilization, the outlook remains tethered to the global interest rate environment and the performance of the rupee. Institutional focus is currently shifting toward capital goods and power infrastructure—sectors that benefit from direct government spending rather than consumer sentiment. Consequently, a rotation into these domestic-centric themes may persist until global macroeconomic uncertainty diminishes and the earnings yield on Indian financial services becomes more competitive against safe-haven assets.