What Happened

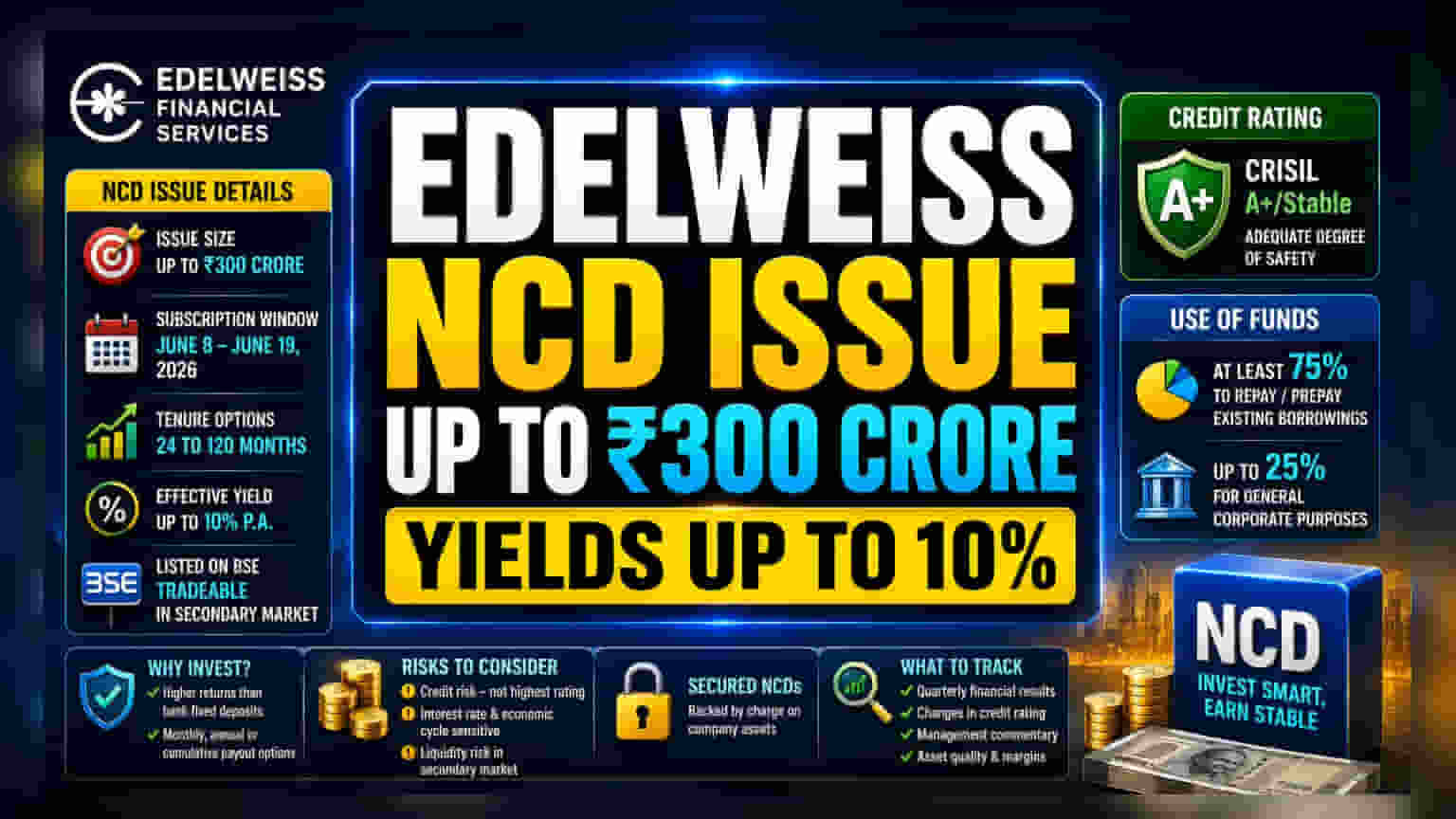

Edelweiss Financial Services Ltd (EFSL) has launched a public issue of secured, redeemable non-convertible debentures (NCDs) to raise up to ₹300 crore. The issue consists of a base size of ₹150 crore, with an option to retain oversubscription up to another ₹150 crore. The subscription window opened on June 8, 2026, and is scheduled to remain open until June 19, 2026, unless closed earlier by the company.

Investors can choose from multiple series with tenures ranging from 24 months to 120 months. The company is offering effective annual yields of up to 10%. These NCDs will be listed on the BSE, allowing for trading in the secondary market.

Why This Matters For Investors

For investors seeking fixed income, this NCD issue offers interest rates that are generally higher than standard bank fixed deposits. The NCDs provide flexibility with monthly, annual, and cumulative interest payout options. However, these returns come with credit risk. Because EFSL is a financial services company, its ability to pay interest and return the principal depends on its own financial health and its ability to manage its loan book effectively.

The Credit Rating and Safety

CRISIL Ratings has assigned a 'CRISIL A+/Stable' rating to these NCDs. In the world of credit ratings, an A+ rating indicates an adequate degree of safety regarding the timely servicing of financial obligations. However, it is important for investors to understand that this is not the highest safety rating. Instruments rated AAA or AA typically carry lower credit risk than those rated A+.

Investors should be aware that credit ratings are subject to periodic review. If the company’s financial position or the sector’s health changes, the rating could be revised, which in turn can influence the market price of the NCDs if they are sold before maturity.

Usage of Funds

Edelweiss Financial Services plans to use at least 75% of the money raised to repay or prepay existing borrowings. The remaining 25% will be used for general corporate purposes. Using funds for debt repayment is a common practice for non-banking financial companies (NBFCs) to manage their cost of borrowing and ensure they have enough liquidity to meet their ongoing obligations.

Risks and Considerations

While these NCDs are secured, meaning they have a claim on the company's assets, the process of recovering money in the event of a default can be lengthy and complex. Investors should consider that NBFCs operate in a sector sensitive to interest rate changes and economic cycles. If borrowing costs rise or if there is stress in the loan segments where the company operates, it could impact their profitability.

Furthermore, while these instruments are listed on the exchange, liquidity—the ease of buying or selling—can vary. There may not always be enough buyers if an investor wants to exit the investment early, and the price on the exchange may fluctuate based on interest rate trends.

What Investors Should Track

Investors interested in this issue should keep an eye on a few key areas. First, monitor the company’s quarterly financial results to ensure stable profitability and asset quality. Second, stay updated on any changes in the credit rating assigned by CRISIL. Finally, observe the company's management commentary regarding its lending business and expansion plans. Understanding the company's debt levels and its success in maintaining healthy margins will be important for assessing the long-term safety of the investment.