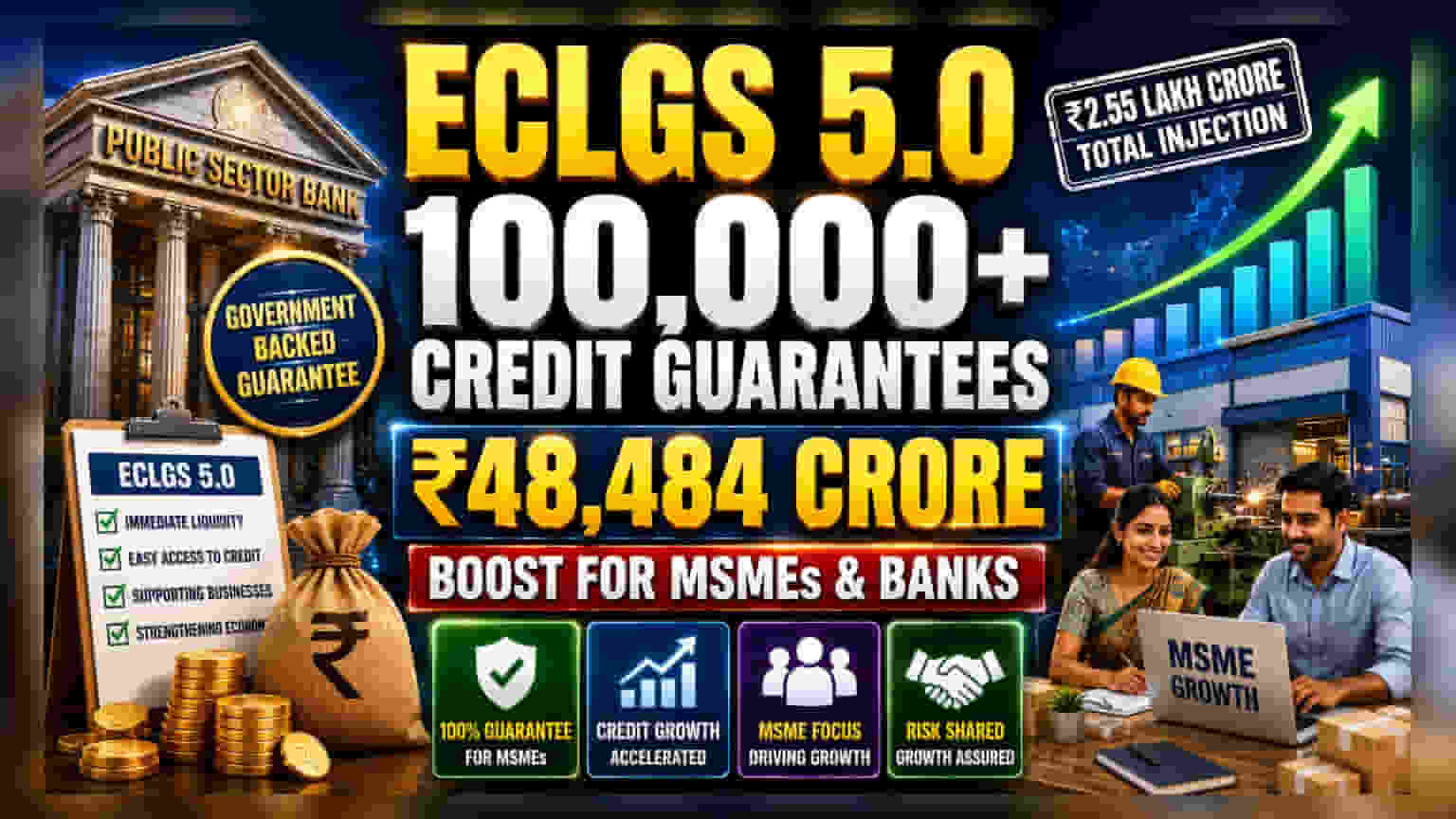

The Emergency Credit Line Guarantee Scheme (ECLGS) 5.0 has rapidly injected over ₹48,484 crore into the economy, with public sector banks leading the distribution to MSMEs. This scheme aims to boost credit growth while reducing lending risk for banks through government-backed guarantees.

What Happened

The government-backed Emergency Credit Line Guarantee Scheme (ECLGS) 5.0 has seen a significant uptake in its first month, with banks issuing over 100,000 credit guarantees. The total value of these guarantees has reached ₹48,484.26 crore. The Ministry of Finance reported this rapid deployment, noting that the scheme is designed to provide immediate liquidity to businesses facing financial constraints. The program intends to inject a total of ₹2.55 lakh crore into the Indian economy, acting as a support mechanism for businesses in need of working capital.

Why This Matters For Banks

For investors in the banking sector, particularly public sector banks, this scheme is a significant development. Lending to Micro, Small, and Medium Enterprises (MSMEs) is traditionally viewed as a high-risk activity due to the volatile nature of these businesses and their vulnerability to economic cycles. By providing a government-backed guarantee—100% for MSME loans and 90% for non-MSME entities—the scheme effectively lowers the risk for banks. This allows banks to expand their loan books more confidently. Public sector banks, which processed 96% of the guarantees, are the primary beneficiaries of this risk-sharing structure, enabling them to boost their credit growth without a corresponding rise in perceived risk.

The MSME Focus

The scheme has prioritized the MSME sector, which accounts for 96% of the guarantees by number and 86% by total value. MSMEs often serve as the backbone of local employment and manufacturing. However, they frequently struggle to secure affordable loans because they lack large assets to pledge as collateral. By shifting the risk to the government, ECLGS 5.0 bridges this gap, allowing banks to extend credit to a segment that is essential for broader economic growth but otherwise difficult to lend to.

Understanding the Risk Benefit

While the scheme provides immediate relief to borrowers and encourages bank lending, it is important for investors to understand the nature of the guarantee. The government essentially acts as a safety net. If a borrower defaults, the government covers a large portion of the loss. This does not mean the bank can lend without checking the borrower’s ability to repay. Banks must still follow their standard lending processes. The risk for banks and shareholders is that while the guarantee covers a significant loss, the process of claiming this guarantee can be time-consuming or subject to specific documentation requirements. Investors often monitor whether these loans eventually turn into productive assets that can repay their debt without relying on government protection.

What Investors Should Track

The rapid rollout is a positive sign for short-term credit demand, but the long-term success of the scheme will depend on the repayment behavior of these borrowers. Investors may want to monitor the following areas in future bank earnings reports:

First, watch for updates on how much of these loans transition into regular, performing assets once the initial support period ends.

Second, keep an eye on credit growth trends in public sector banks. Since these banks are leading the rollout, any acceleration in their loan portfolios could be partly linked to such government-backed schemes.

Third, look for management commentary on the quality of the new loan book. While the government guarantee reduces risk, the underlying ability of MSMEs to generate cash flow remains the most important factor for long-term bank health.