Canara Bank and Indian Bank’s first-quarter reports show credit growth significantly outpacing deposit growth. While this reflects strong loan demand, it creates a potential challenge for banks to fund this expansion without squeezing profit margins. Investors should track how these lenders manage their cost of funds moving forward.

What Happened

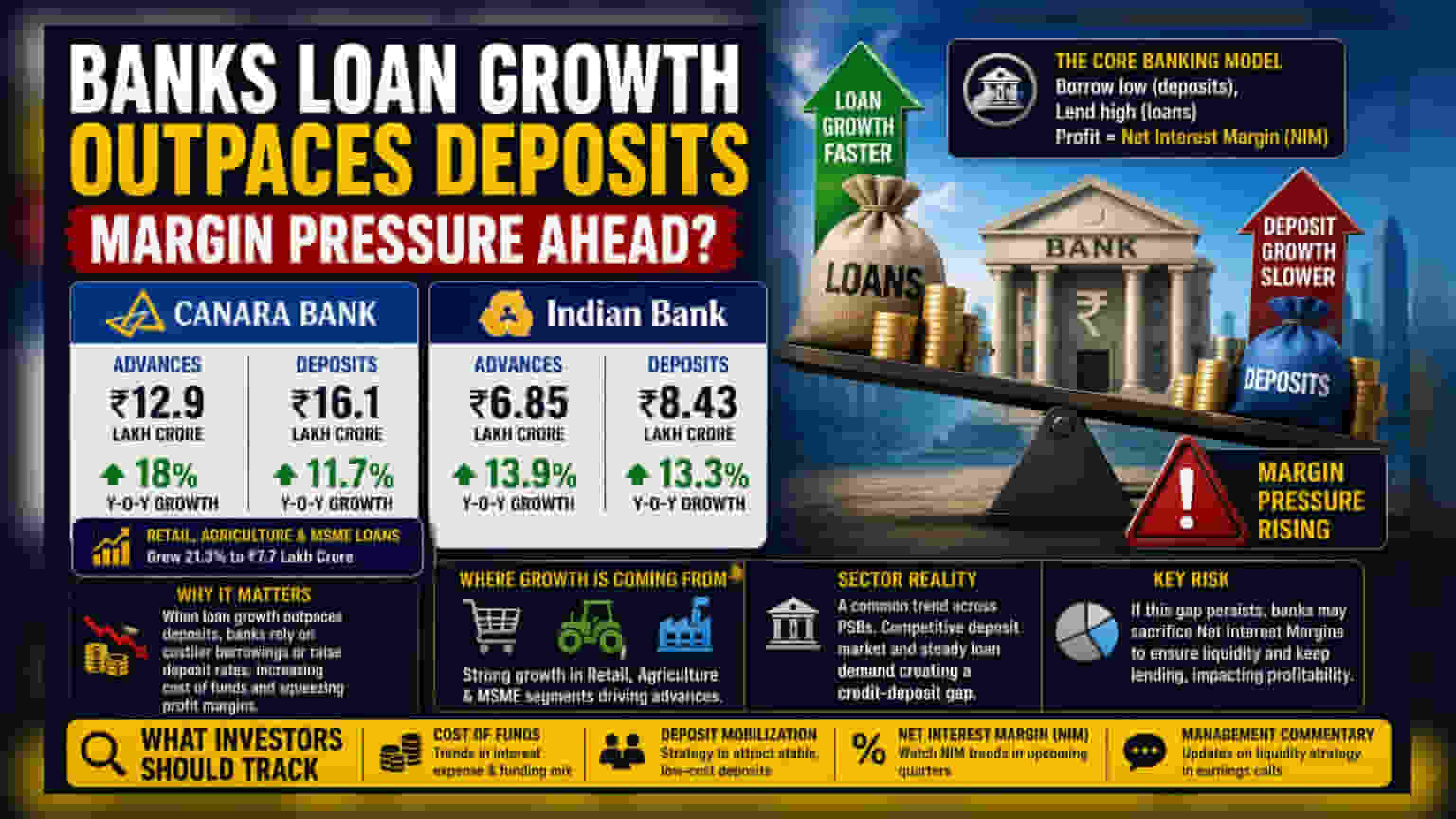

Canara Bank and Indian Bank have reported their first-quarter performance for the current financial year, highlighting a common trend across the banking sector: loan demand is growing faster than the money being deposited by customers.

Canara Bank reported an 18% year-on-year increase in advances, which reached Rs 12.9 lakh crore by the end of June. In the same period, its deposits grew at a slower pace of 11.7%, totaling Rs 16.1 lakh crore.

Indian Bank showed a similar pattern. Its advances grew by 13.9% to Rs 6.85 lakh crore, while deposit growth stood at 13.3%, reaching Rs 8.43 lakh crore.

The Profit Margin Challenge

For any bank, the core business is to take deposits from customers at a lower interest rate and lend that money out to borrowers at a higher interest rate. The difference between these two rates is known as the Net Interest Margin (NIM), which represents the bank's profit from its lending activities.

When a bank’s loan growth consistently outpaces its deposit growth, it faces a liquidity challenge. The bank cannot simply create money; it needs deposits to fund new loans. If deposits do not grow fast enough, the bank has two options: rely on more expensive market borrowings or raise interest rates on fixed deposits to attract more savers. Both of these actions increase the bank’s cost of funds, which can put pressure on profit margins if the bank cannot pass on these higher costs to its borrowers.

Where The Growth Is Coming From

At Canara Bank, the expansion in loans was not uniform across all sectors. The bank’s retail, agriculture, and MSME (Micro, Small and Medium Enterprises) lending segments were the primary drivers, growing at a robust 21.3% to Rs 7.7 lakh crore. This growth in these specific segments was significantly faster than its wholesale or corporate lending. While this indicates strong economic activity at the grassroots level, it also suggests that the bank is aggressively expanding in areas that require high operational focus.

What This Means For The Banking Sector

This trend is not unique to these two lenders. Many public sector banks in India are currently navigating a competitive landscape where depositors are seeking higher returns, while loan demand remains steady.

For investors, the risk is that if this "gap" between lending and deposits persists, banks may have to sacrifice some of their profit margins to ensure they have enough cash to keep lending. The market will be watching closely to see if banks can effectively balance their loan growth with the need to attract stable, lower-cost deposits.

What Investors Should Track

Going forward, the key monitorables for shareholders will be the banks' cost of funds and their ability to mobilize deposits. Investors may watch for management commentary in upcoming earnings calls regarding their strategy to attract deposits without significantly increasing interest expenses. Additionally, any changes to the bank’s Net Interest Margin in the coming quarters will be a critical indicator of whether this credit-deposit gap is affecting profitability.