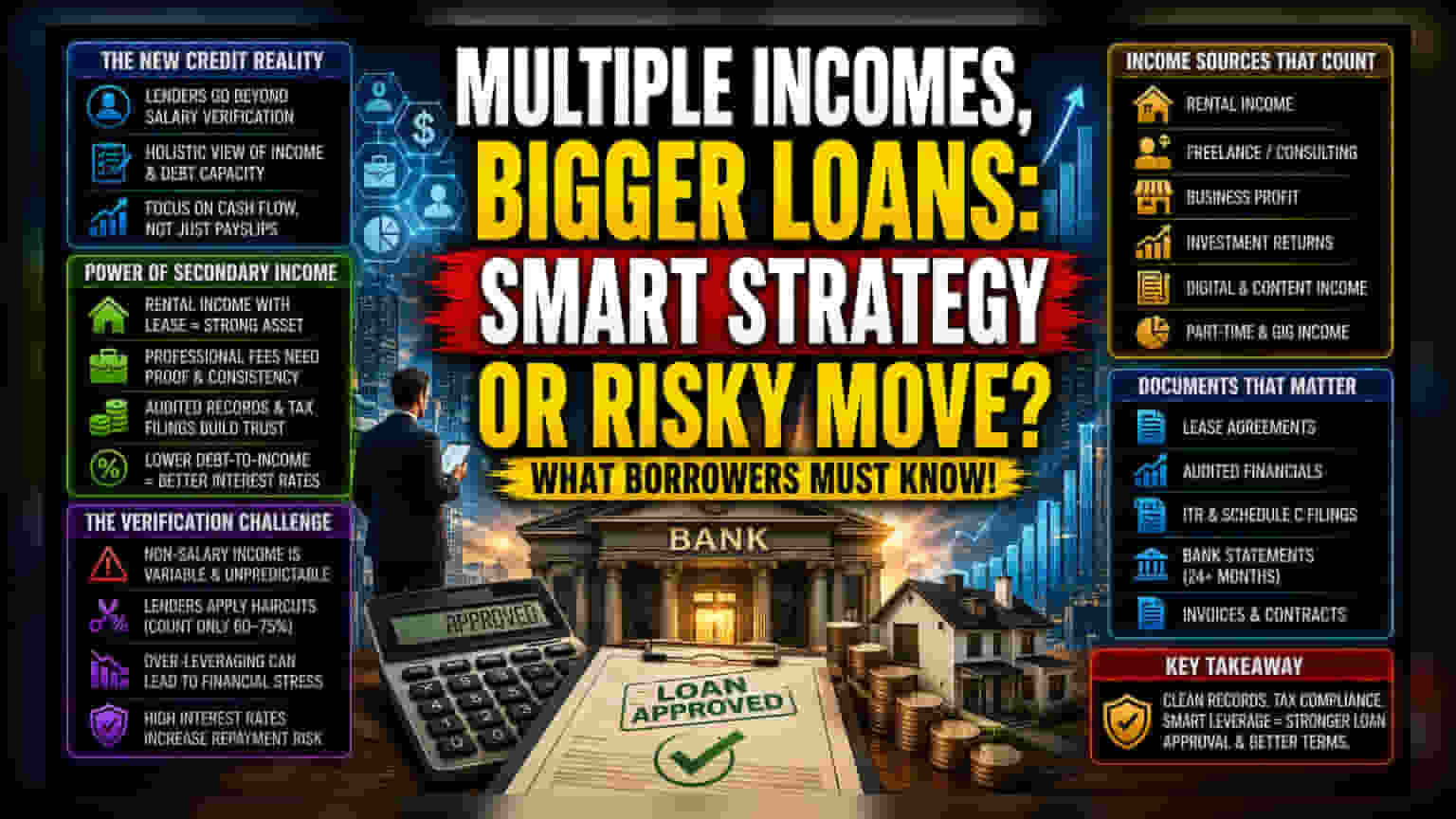

The Shift in Credit Assessment

Institutional lenders have moved away from legacy models that relied exclusively on primary employment verification. This transition acknowledges the rise of the diversified income earner, moving toward a holistic debt-service-coverage ratio that incorporates side ventures and passive assets. For the borrower, this change is not merely an administrative shift; it provides a mechanism to bridge the gap between their actual cash flow and the restrictive borrowing limits imposed by automated underwriting systems.

Quantifying Secondary Revenue Streams

Successfully leveraging multiple income streams requires moving beyond casual bookkeeping. Banks currently prioritize consistency over volume. A significant rental deposit appearing once will be ignored, whereas a two-year track record of rental receipts attached to a formal lease agreement is treated as a core asset. Professional fees and business profits require an even higher evidentiary burden, typically necessitating audited financial statements or consistent Schedule C tax filings. When these figures are consolidated, the borrower effectively lowers their debt-to-income ratio, which often triggers an automatic reduction in risk-based pricing, potentially securing interest rates reserved for higher-income brackets.

The Forensic Bear Case: Verification Risks

While the ability to aggregate income creates opportunity, it introduces significant friction in the approval process. The primary risk factor involves the variability of non-salary income. Unlike a W-2 or a standard salary certificate, income from investments or freelance work is frequently subject to market volatility or contract cancellations. Consequently, lenders apply steep 'haircuts' to secondary income, often counting only 60 to 75 percent of the total figure toward repayment capacity. Borrowers who over-leverage based on gross secondary income often find themselves in precarious positions if those revenue streams contract, particularly in a high-interest-rate environment where debt servicing costs remain elevated.

Strategic Documentation and Market Outlook

Maximizing loan eligibility today depends on the integration of financial records with tax transparency. Lenders are increasingly utilizing automated data-scraping tools to verify recurring deposits against tax filings. Discrepancies between bank inflows and reported income are now the primary cause of application rejection. As the financial sector continues to refine these risk models, the premium on clean, documented financial history will only increase. Applicants who maintain rigorous separation between personal and business finances while ensuring all secondary income is tax-compliant will find themselves in a dominant position when negotiating loan terms in an tightening credit environment.