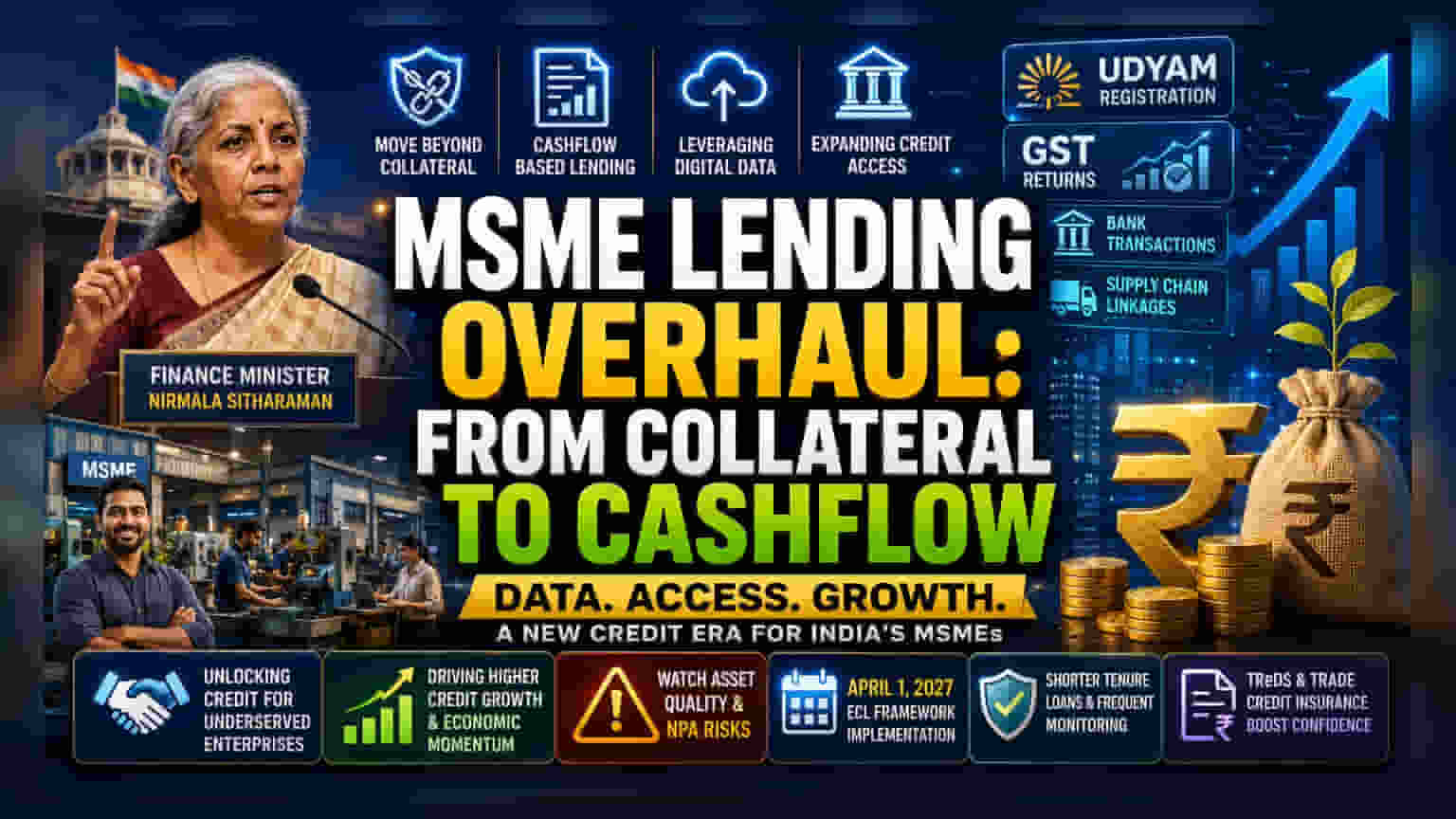

Finance Minister Nirmala Sitharaman has pushed lenders to move from traditional collateral-based lending to cashflow-based models for MSMEs. By leveraging digital data from platforms like Udyam, banks hope to increase credit access. Investors should monitor how this change impacts bank asset quality, credit growth, and preparedness for the upcoming Expected Credit Loss (ECL) accounting framework in 2027.

What Happened

Finance Minister Nirmala Sitharaman has called upon Indian financial institutions to overhaul their lending practices for micro, small, and medium enterprises (MSMEs). The directive aims to move banks away from a heavy reliance on collateral—such as property or physical assets—toward credit models based on the actual cashflow and business health of the enterprise. The government is encouraging banks to utilize the wealth of digital data available through platforms like Udyam and GST filings to assess the creditworthiness of small businesses.

Why This Matters For Investors

For investors, this shift represents a potential change in how banks and non-banking financial companies (NBFCs) grow their loan books. MSMEs are a vital engine for the Indian economy, but many have historically struggled to get loans because they lack the high-value physical collateral that traditional banks demand.

If banks successfully adopt cashflow-based models, they could unlock a massive, underserved market. This could drive higher credit growth for lenders with strong MSME exposure. However, for investors, this also creates a need to watch asset quality closely. Lending without hard collateral requires sophisticated data analytics to ensure that borrowers can actually repay. If this process is not handled well, it could lead to higher bad loans, known as non-performing assets (NPAs).

The Move Toward Data-Driven Lending

Banks are increasingly using 'digital footprints' to replace physical security. This includes analyzing GST returns, bank transaction patterns, and supply-chain linkages to understand if a business is thriving or struggling. Some lenders are already launching schemes, such as those that allow loans to be backed by credit guarantee funds, reducing the need for the borrower to pledge assets. This shift is intended to help banks reach enterprises in smaller cities and Tier-II and Tier-III markets, where the concentration of businesses is high but access to formal credit has traditionally been low.

Why Investors Should Track the ECL Framework

An important date on the horizon is April 1, 2027. This is when the new Expected Credit Loss (ECL) framework is set to become effective. Unlike the current 'incurred loss' model, where banks provide for a loss only after a default occurs, the ECL model requires banks to make provisions for potential losses before they happen.

This change will force banks to be more careful. If a bank’s MSME portfolio is viewed as risky, the ECL framework could force them to set aside more capital, which might squeeze their profit margins. Investors should pay close attention to how banks adjust their lending practices to prepare for this tighter regulatory environment. The use of shorter-tenure loans and more frequent monitoring of business cashflows are strategies banks may use to mitigate these risks.

Managing the Risks of Delayed Payments

A persistent challenge for the MSME sector is the delay in payments from larger corporate customers, which often leaves small businesses with cash flow problems. Initiatives like the Trade Receivables Discounting System (TReDS) are designed to help these businesses get paid faster by discounting their invoices. The integration of trade credit insurance into these platforms is a positive step for financier confidence. Investors monitoring the banking sector should keep an eye on how these platforms evolve, as they provide a safer way for banks to lend based on the strength of the corporate buyer rather than just the MSME itself.

What Investors Should Track Next

Investors may want to monitor a few key areas in the coming quarters. First, watch for updates on how banks are adopting cashflow-based lending technologies. Second, keep track of NPA levels in the MSME portfolios of banks with high exposure to this sector. Finally, listen for management commentary regarding their readiness for the 2027 ECL framework. These factors will be critical in understanding whether the push for wider MSME credit will result in sustainable growth or increased pressure on bank profitability.