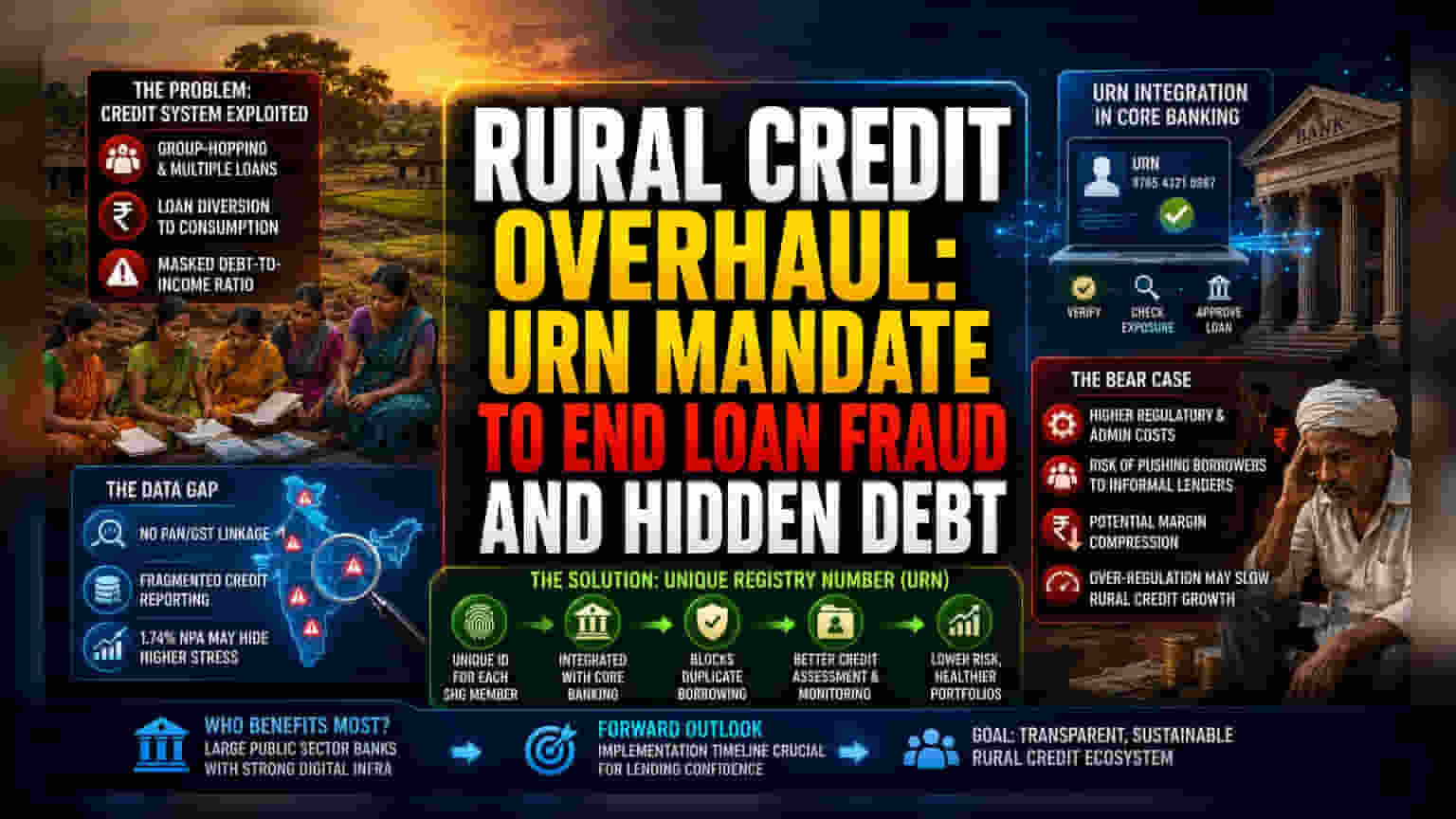

The Credit Integrity Crisis

The push for structural reform in rural lending stems from a growing awareness that the current SHG-bank linkage model is being exploited by sophisticated circular debt cycles. While the stated goal of these groups is to facilitate micro-entrepreneurship, banking sector data suggests that a significant volume of credit is being diverted into consumption, or worse, leveraged by individuals gaming the system through participation in multiple, overlapping groups. By integrating URNs directly into Core Banking Systems (CBS), lenders intend to neutralize this "group-hopping" behavior, which effectively masks the true debt-to-income ratio of rural borrowers.

The Data Gap and Regulatory Friction

The move toward a central registry reflects a broader trend in financial institutional rigor. Unlike corporate borrowers or formal MSMEs, most SHGs operate outside the purview of PAN or GST-based credit reporting. This creates a dangerous blind spot for commercial banks, as they currently lack the data infrastructure to cross-reference credit exposure across different lending institutions. Analysts suggest that the 1.74% NPA figure likely masks a higher degree of hidden stress, as banks currently rely on fragmented, group-level reporting rather than individual-member, PAN-linked credit visibility. A centralized URN mandate would allow banks to treat SHG credit history with the same scrutiny applied to individual retail borrowers, effectively bringing rural micro-credit into the formal fold.

The Bear Case for Micro-Lending

While the mandate for URNs may appear as a simple technical upgrade, it carries significant risks for the micro-finance industry. Critics within the development sector argue that over-regulating SHGs could stifle the velocity of capital in rural economies. Should the government implement a rigid, high-friction registration process, there is a risk that vulnerable populations will be pushed toward informal, predatory money lenders who operate without the oversight of the National Rural Livelihoods Mission. Furthermore, for banks, the administrative cost of maintaining a real-time, verified registry for millions of low-ticket accounts may outweigh the benefit of slightly reduced NPA rates. Investors should note that increased regulatory burden often leads to margin compression in banking portfolios heavily exposed to rural micro-credit.

Forward Guidance

Industry participants are closely monitoring the next round of banker committee meetings, where the implementation timeline for these registry requirements will be finalized. The shift is expected to favor large-cap public sector banks with existing digital infrastructure, as they are better positioned to integrate these new verification protocols than smaller, resource-constrained regional rural banks. The ultimate outcome hinges on whether this digital-first approach restores lending confidence or forces a contraction in the rural credit supply.