Bank of Baroda has introduced the 'bob Legend FCNR(B) Deposit Scheme' for non-resident Indians, offering up to 6.25% interest on five-year U.S. dollar deposits. This initiative aims to attract stable foreign currency inflows. While the scheme helps the bank boost its liquidity, investors will monitor if these competitive rates pressure the bank's overall cost of funds and profit margins in the coming quarters.

What Happened

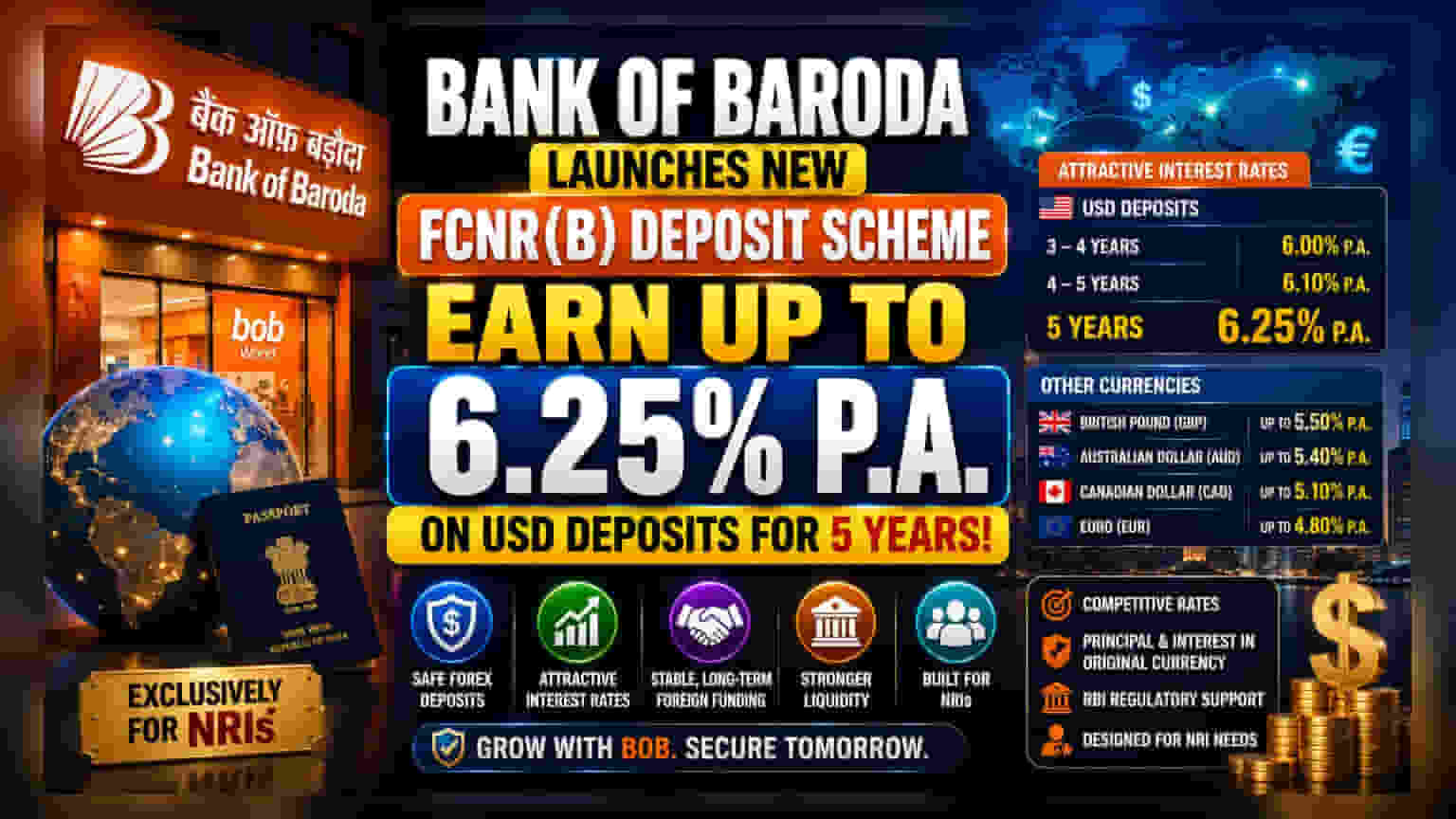

Bank of Baroda has launched a new deposit product called the 'bob Legend FCNR(B) Deposit Scheme,' specifically designed for Non-Resident Indians (NRIs). The scheme offers interest rates of up to 6.25% annually on U.S. dollar deposits with a five-year tenure. The bank is also offering tiered rates for shorter durations, with 6% for terms between three and four years, and 6.1% for terms between four and five years. The bank has also set interest rates for other major currencies, including the British pound, Australian dollar, Canadian dollar, and the euro.

Why This Matters For Investors

For a bank, attracting Foreign Currency Non-Resident (FCNR) deposits is a strategic move to secure stable, long-term foreign currency funding. By offering higher rates, the bank can attract capital from NRIs who prefer to keep their funds in foreign currencies rather than converting them into Indian rupees. This eliminates currency fluctuation risk for the depositor, as both the principal and interest are maintained in the original currency. For the bank, these deposits act as a useful source of liquidity.

How Investors May Read This

Investors often look at how deposit growth affects a bank's net interest margin, which is the difference between the interest a bank earns from loans and the interest it pays to depositors. While aggressive deposit schemes help banks grow their asset base and meet loan demand, they also increase the cost of funds. If a bank pays higher interest rates to attract depositors, it needs to ensure that it can deploy these funds into high-yielding loans to protect its profit margins. Investors will be watching the bank's quarterly results to see if this new scheme effectively grows the deposit base without significantly squeezing profit margins.

The Bigger Business Context

Indian banks have been facing intense competition to attract deposits to support their credit growth. With the credit-to-deposit ratio remaining a key monitorable for the banking sector, many institutions are rolling out specific products to capture stable, long-term capital. The Reserve Bank of India also provides regulatory support to help banks manage these foreign currency deposits, including allowing them to absorb hedging costs for specific tenures. This regulatory environment is designed to encourage banks to bring in more foreign currency to bolster liquidity.

What Could Go Wrong

The primary risk for shareholders in such schemes involves the cost-benefit balance. If the bank attracts a large volume of deposits at these higher rates but struggles to find enough high-quality lending opportunities, the cost of these deposits could negatively impact the bank's profitability. Additionally, the success of such schemes depends on the interest rates offered by global investment alternatives. If global interest rates rise significantly, these bank deposit rates may become less attractive, potentially limiting the success of the campaign.

What Investors Should Track

The most important factor to track is the bank's deposit growth numbers in the upcoming quarterly updates. Investors may also look for management commentary on the 'cost of funds' and whether they see margin pressure from these deposit initiatives. Monitoring the credit-to-deposit ratio will also provide insight into how efficiently the bank is putting these new funds to work. Finally, any changes in the RBI's regulatory stance on hedging costs or foreign currency inflows will be important for understanding the long-term viability of these schemes.