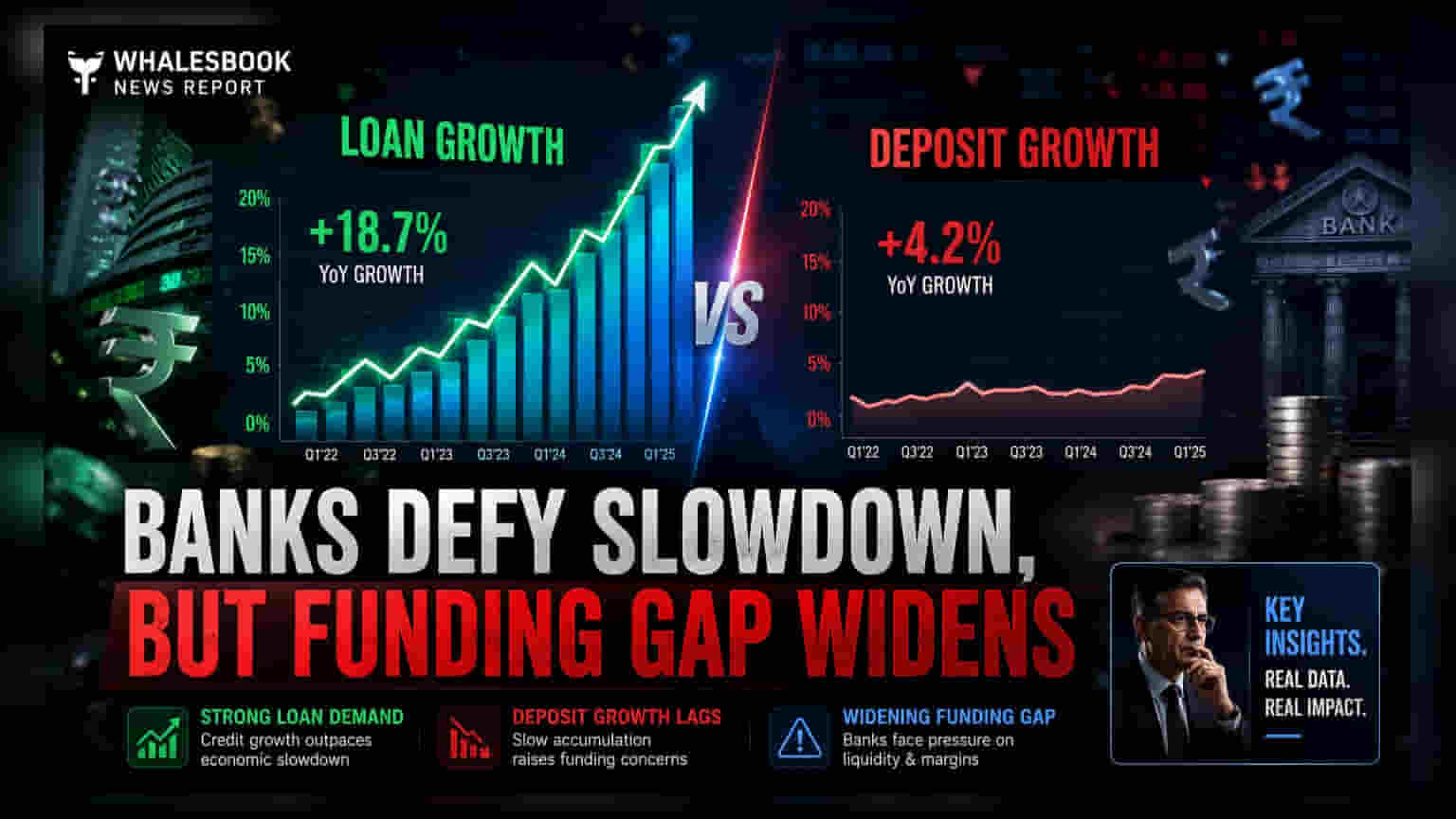

Indian banks reported robust loan growth in Q1 FY27, led by retail, agriculture, and MSME sectors. However, deposit growth continues to trail advances, causing a shift in loan-to-deposit ratios. This imbalance forces lenders to rely on costlier funding, which investors may watch closely as it impacts profit margins.

What Happened

Several public and private sector banks have released their provisional business updates for the first quarter of the fiscal year 2027 (Q1 FY27). The data shows a persistent trend of strong credit demand. Banks continue to see significant interest in loans, particularly from the retail, agriculture, and Micro, Small, and Medium Enterprises (MSME) segments. Despite this robust loan activity, a common challenge has emerged across the sector: deposit growth is not keeping pace with the money being lent out. This gap has led to a sequential decline in loan-to-deposit ratios, meaning banks are lending out a larger portion of their available deposits than before.

The Loan-Deposit Mismatch

For investors, the gap between loan growth and deposit growth is a critical metric to watch. Banks primarily fund their lending activities through deposits collected from customers. When loan growth significantly outpaces deposit growth, banks face a liquidity squeeze. To keep lending, they often need to raise funds through more expensive sources, such as certificates of deposit or inter-bank borrowing. This higher cost of borrowing can put pressure on net interest margins—the difference between the interest income a bank earns on loans and the interest it pays out on deposits. If deposit mobilization does not catch up, maintaining stable profit margins becomes more challenging.

How Different Banks Fared

Performance varied across the sector during the June quarter. Canara Bank started the fiscal year with healthy advance growth, largely supported by its retail and MSME portfolio, though it faced the common issue of slower deposit accumulation. Indian Bank reported more moderate growth in both advances and deposits; however, it maintained a strong competitive advantage through its low-cost deposit franchise, with a stable Current Account Savings Account (CASA) ratio of 39.6%. A higher CASA ratio helps banks keep their overall cost of funds lower.

Jammu & Kashmir Bank stood out as a strong performer, successfully balancing both loan and deposit growth. Other lenders like South Indian Bank, Tamilnad Mercantile Bank, and Karnataka Bank saw healthy credit growth but continued to struggle with deposit mobilization. Tamilnad Mercantile Bank specifically outperformed its own loan growth guidance. Dhanlaxmi Bank presented a more balanced picture, with growth in both deposits and advances remaining steady, helped by gold loans and its existing deposit base. Conversely, Punjab & Sind Bank lagged behind industry trends, reporting slower expansion in both credit and deposit portfolios.

Why Profit Margins Are The Focus

Investors are paying close attention to these updates because they serve as an early indicator of profitability. While strong loan growth is generally positive for revenue, the sustainability of this growth depends on the bank's ability to fund it cheaply. Banks with a strong base of savings and current accounts are better positioned to protect their margins against rising funding costs. If deposit growth remains sluggish, the sector might see continued competition for customer funds, which could push up deposit interest rates and further squeeze profitability in the coming quarters.

What Investors Should Track Next

Moving forward, the primary monitorable will be the management commentary on deposit mobilization strategies in the upcoming quarterly results. Investors may look for details on how banks plan to bridge the gap between loan and deposit growth. Specifically, keeping an eye on the stability of CASA ratios and any changes in the cost of funds will be essential. Additionally, it will be important to observe whether banks prioritize deposit growth over loan growth to restore a more comfortable loan-to-deposit balance, as this will influence both their lending capacity and bottom-line earnings.