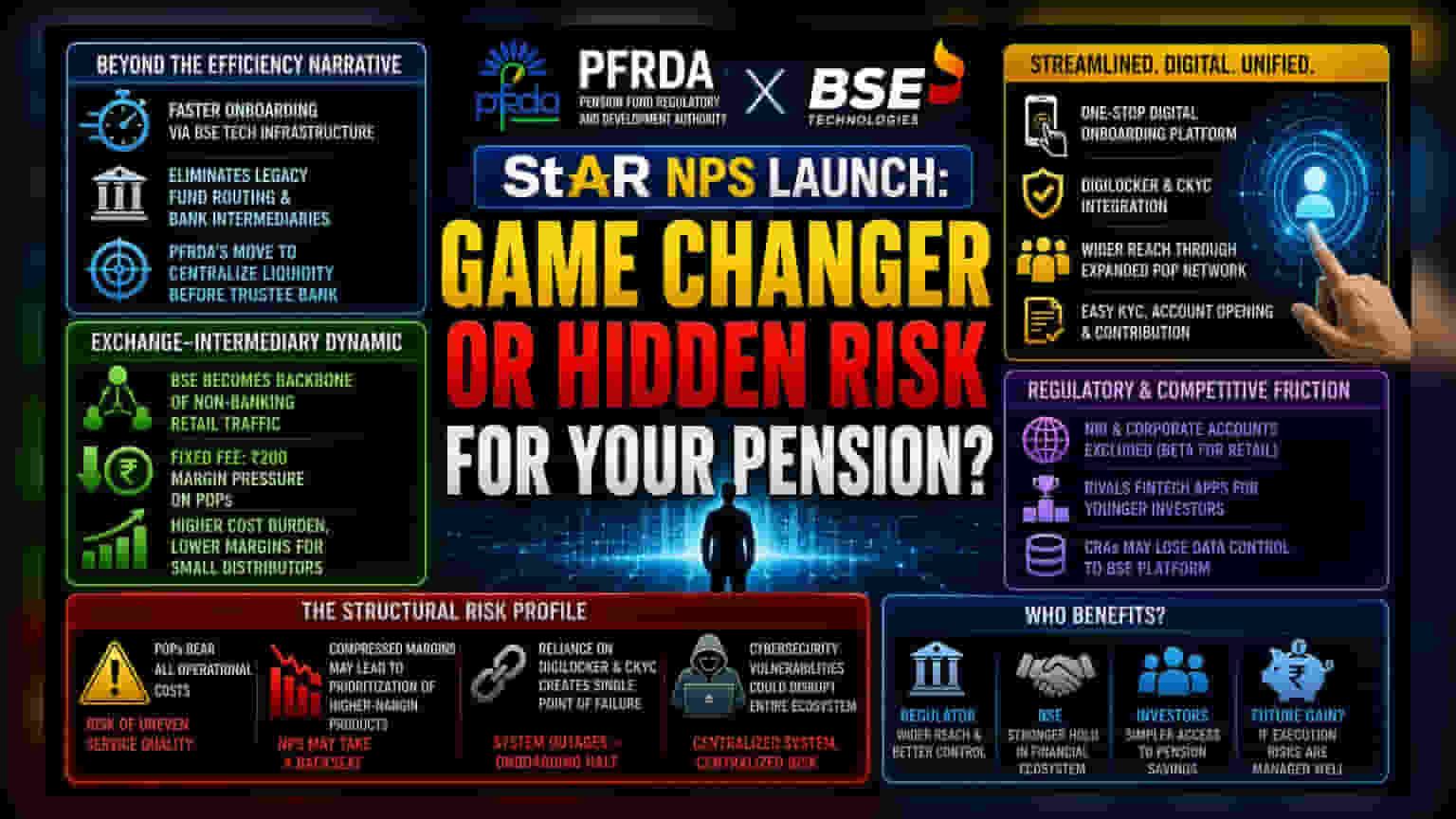

Beyond the Efficiency Narrative

While the industry touts the speed of the newly launched StAR NPS, the move represents a defensive consolidation for the Pension Fund Regulatory and Development Authority (PFRDA) rather than a mere technological upgrade. By utilizing BSE Technologies' existing exchange-traded infrastructure, the regulator is essentially force-multiplying the distribution capacity of Points of Presence (PoPs) to counter stagnant voluntary enrollment rates. The shift away from legacy fund routing, which historically required a labyrinthine path through various banking intermediaries, suggests a move toward centralizing liquidity before the funds even reach the Trustee Bank.

The Exchange-Intermediary Dynamic

This integration underscores the growing influence of exchange-owned technology platforms in the broader financial services ecosystem. By embedding the onboarding process directly into a platform that already facilitates high-frequency transaction flow, BSE effectively cements its role as the backbone of non-banking financial retail traffic. However, this creates a distinct margin pressure for PoPs. Since these entities are now responsible for absorbing the underlying operational costs while still being held accountable for KYC and grievance resolution, the fee structure remains fixed at ₹200. This effectively squeezes the profit margins of smaller distributors who lack the scale to offset these maintenance costs with high-volume registrations.

Regulatory and Competitive Friction

The exclusion of Non-Resident Indians and corporate accounts signals that this rollout is a beta-test for retail mass-market adoption rather than a total system overhaul. From a competitive standpoint, the PFRDA is attempting to create a unified experience that rivals the simplicity of modern fintech apps, which have historically siphoned younger demographics toward private investment vehicles rather than government-backed retirement products. Market participants should monitor whether the Central Recordkeeping Agencies (CRAs) will lose their historical grip on data ownership as the platform begins to aggregate behavioral data directly through the BSE stack.

The Structural Risk Profile

Investors in firms acting as significant PoPs should view the mandate for them to bear all operational costs with caution. This creates a potential for uneven service quality; as margins compress, larger financial institutions may prioritize proprietary wealth products over low-margin NPS onboarding. Furthermore, the reliance on DigiLocker and CKYC, while convenient, introduces a single point of failure in the digital verification chain. Should the underlying database services face outages or cybersecurity vulnerabilities, the entire onboarding flow could be halted, exposing the fragility of a system that is now tethered to a centralized technical backbone.