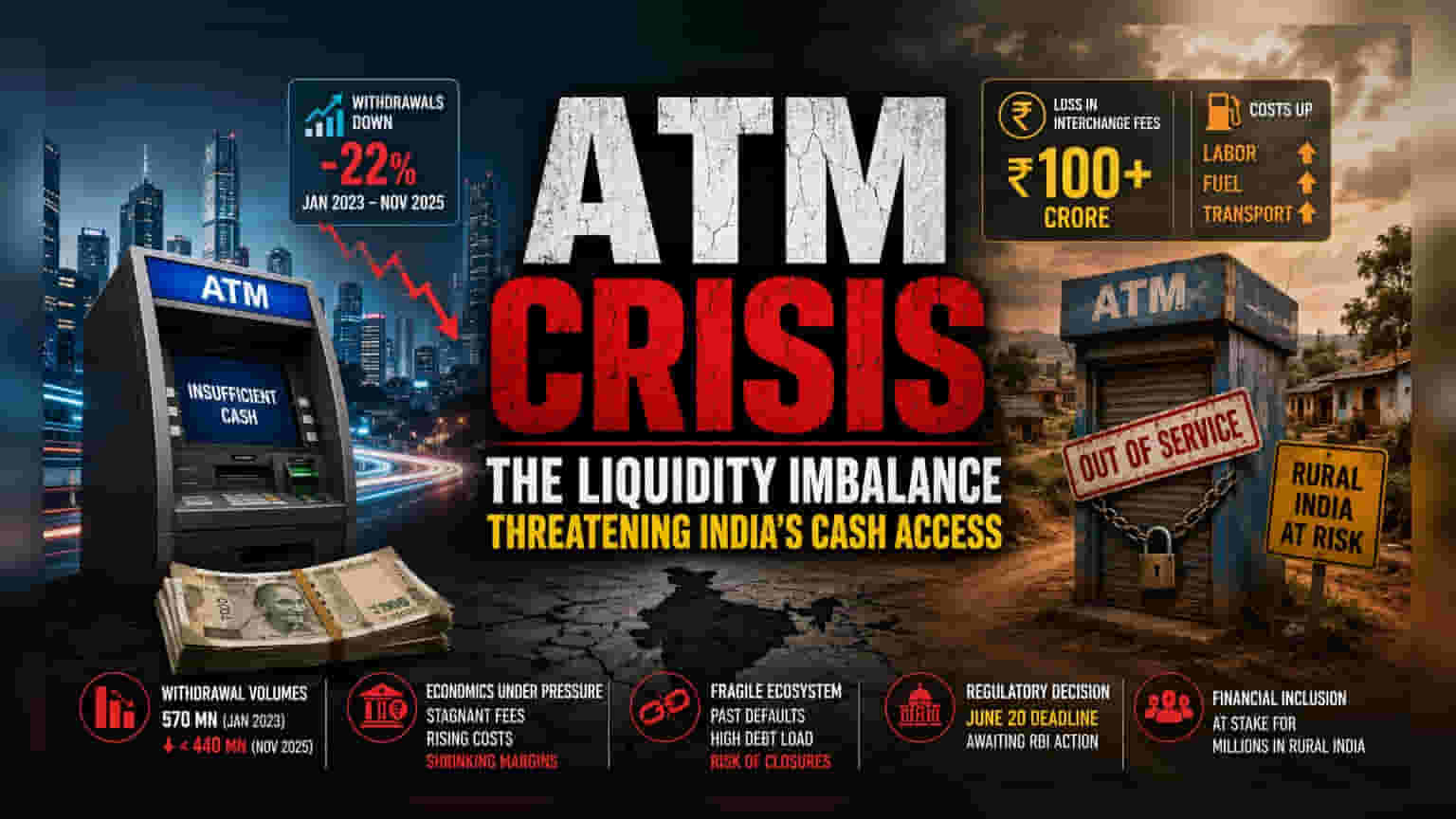

The Structural Liquidity Imbalance

The standoff between the Confederation of ATM Industry and the banking sector is not merely about immediate cash availability but exposes a deeper rot in the financial infrastructure. By prioritizing cash movement to Tier 1 metropolitan zones, institutions like the State Bank of India have created a vacuum in the hinterlands. This strategy minimizes logistical overhead for the banks but effectively hollows out the serviceability of the nation’s ATM network. The financial toll on operators—now exceeding ₹100 crore in lost interchange fees—is only the most visible symptom of a broader breakdown in the revenue-sharing model that currently governs ATM management.

Economic Viability Under Pressure

Beyond the immediate liquidity dispute, the economics of running an ATM in India have soured significantly over the past twenty-four months. The industry is currently contending with a aggressive double-bind: stagnant transaction fees set against surging variable costs. While labor costs have spiked due to significant state-mandated minimum wage revisions and fuel-indexed transport expenses, the underlying consumer behavior is simultaneously shifting toward digital payment rails. Data indicates that monthly ATM withdrawal volumes have sustained a long-term downward trajectory, falling from 570 million in early 2023 to under 440 million by late 2025. This contraction forces operators into a position where every additional kilometer of cash replenishment service erodes the profit margin of the terminal.

The Forensic Bear Case

The fragility of the current ATM ecosystem is underscored by the precedent of previous debt defaults and terminal consolidation. The previous collapse of key industry players, which saw hundreds of crores in bank dues remain unpaid, serves as a sobering indicator of how quickly business models can evaporate when liquidity dries up. Should the Reserve Bank of India fail to mandate a more equitable cash distribution framework, the market risks a cascading wave of off-site ATM closures. This is not merely an operational inconvenience; it is a structural risk to rural financial inclusion. Because these operators run on razor-thin margins and high debt leverage, any prolonged delay in settlement or further reduction in transaction volume renders the entire, independent ATM-deployer model increasingly insolvent.

Forward Trajectory

With the June 20 deadline approaching, the focus now shifts toward the regulatory response. Market analysts suggest that without a formal upward revision of the interchange fee or a direct subsidy for rural cash replenishment, the reduction in machine count—which has already dipped below 251,000 units—is likely to accelerate. While large public sector banks maintain their current distribution priorities to optimize their own internal cost-to-income ratios, the independent operators are nearing a threshold where complete service withdrawal becomes the only rational financial decision.