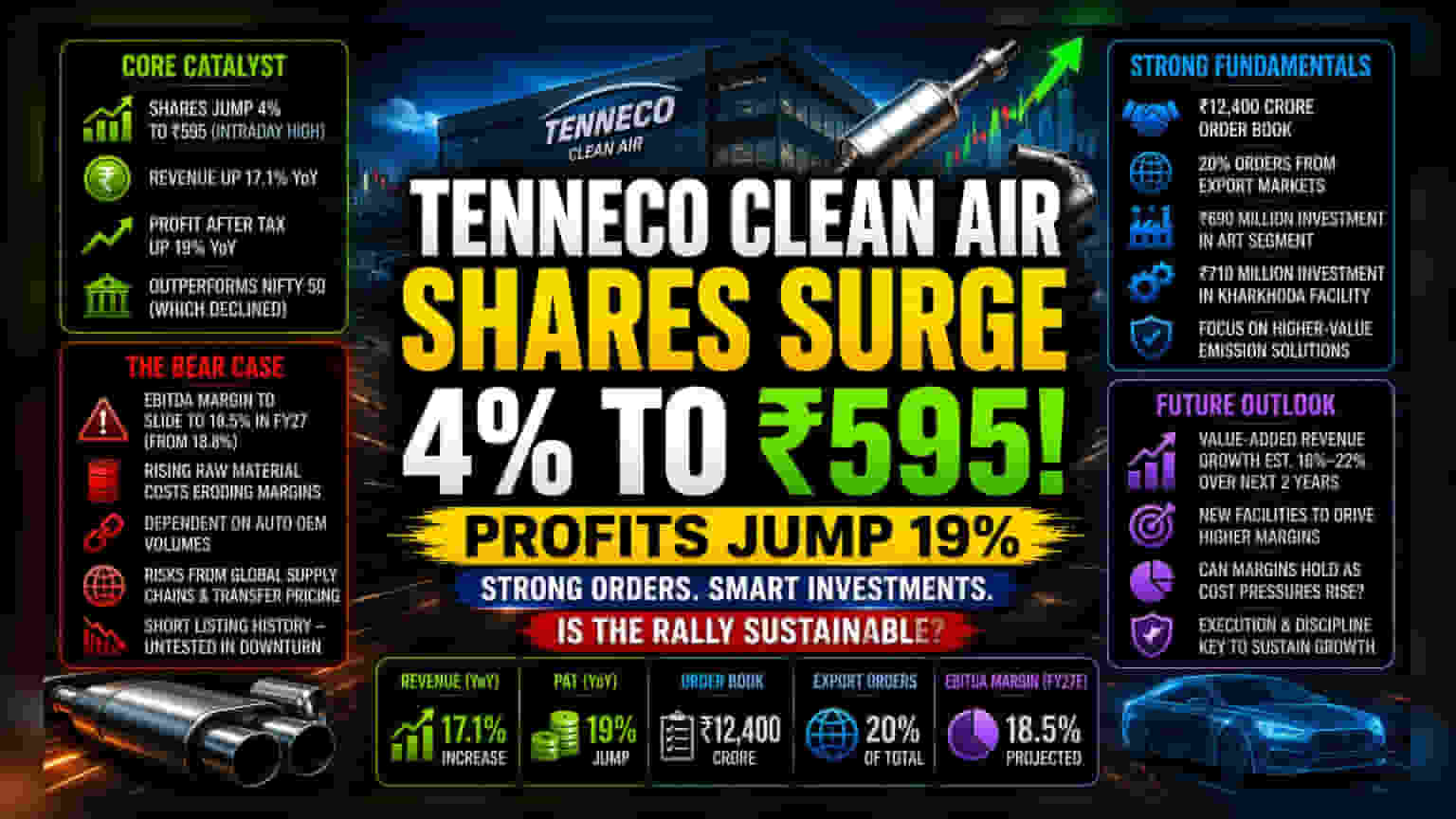

The Core Catalyst

Market participants responded to the latest financial disclosures with immediate buying pressure, lifting the stock by 4% to an intraday high of ₹595. This performance stands in sharp contrast to the broader Nifty 50, which experienced a slight decline during the same session. The primary driver of this positive sentiment is the company’s ability to translate top-line growth into bottom-line profitability, specifically reporting a 17.1% increase in revenue alongside a 19% surge in profit after tax compared to the same period last year. The market appears to be rewarding the company’s ability to maintain high-double-digit growth figures in a period characterized by volatile industrial demand.

The Analytical Deep Dive

When benchmarking against the broader auto-component sector, Tenneco Clean Air’s ability to secure a ₹12,400 crore order book provides a distinct defensive moat. While peers are currently grappling with decelerating demand in the domestic passenger vehicle segment, this company is hedging risk through a diversified export portfolio, which currently accounts for up to 20% of its order volume. Recent capital expenditures, specifically the ₹690 million allocated for the ART segment and a ₹710 million investment in its Kharkhoda facility, suggest management is preparing for a shift toward more stringent emission regulatory requirements. These investments are critical; they signify a transition toward higher-value products that typically command better margins, potentially insulating the company from the commoditization often seen in standard exhaust systems.

The Forensic Bear Case

Despite the positive momentum, significant operational risks remain. The projected EBITDA margin contraction to 18.5% for FY27—down from 18.8%—is not merely a minor variance; it signals that inflationary pressures on raw materials are beginning to erode the company's pricing power. Furthermore, as a subsidiary of a global parent, the company faces inherent risks related to inter-company transfer pricing and potential volatility in global supply chains. Because Tenneco relies heavily on the automotive original equipment manufacturer sector, any softening in vehicle production volumes will hit the order book directly. Investors should note that the company’s relatively short history on the public markets means it has yet to be tested through a prolonged cyclical downturn, leaving its long-term valuation sensitivity largely unproven.

The Future Outlook

Brokerage sentiment remains optimistic, with consensus estimates pointing toward consistent growth in value-added revenue for the next two fiscal years. The forward trajectory is contingent on the company’s ability to operationalize its new facilities without cost overruns. If the anticipated 16% to 22% growth in value-added revenue materializes, the current valuation may be justified, provided that management successfully navigates the narrowing spread between raw material costs and product realisations.