Tata Motors shares dropped over 8% on Wednesday after Jaguar Land Rover's (JLR) investor day. While JLR set a revenue target of £26 billion by FY27, investors were disappointed by the 4% EBIT margin guidance, which fell below analyst expectations. This article explores the strategic outlook, the massive £18 billion investment plan, and the financial pressures weighing on the stock.

What Happened

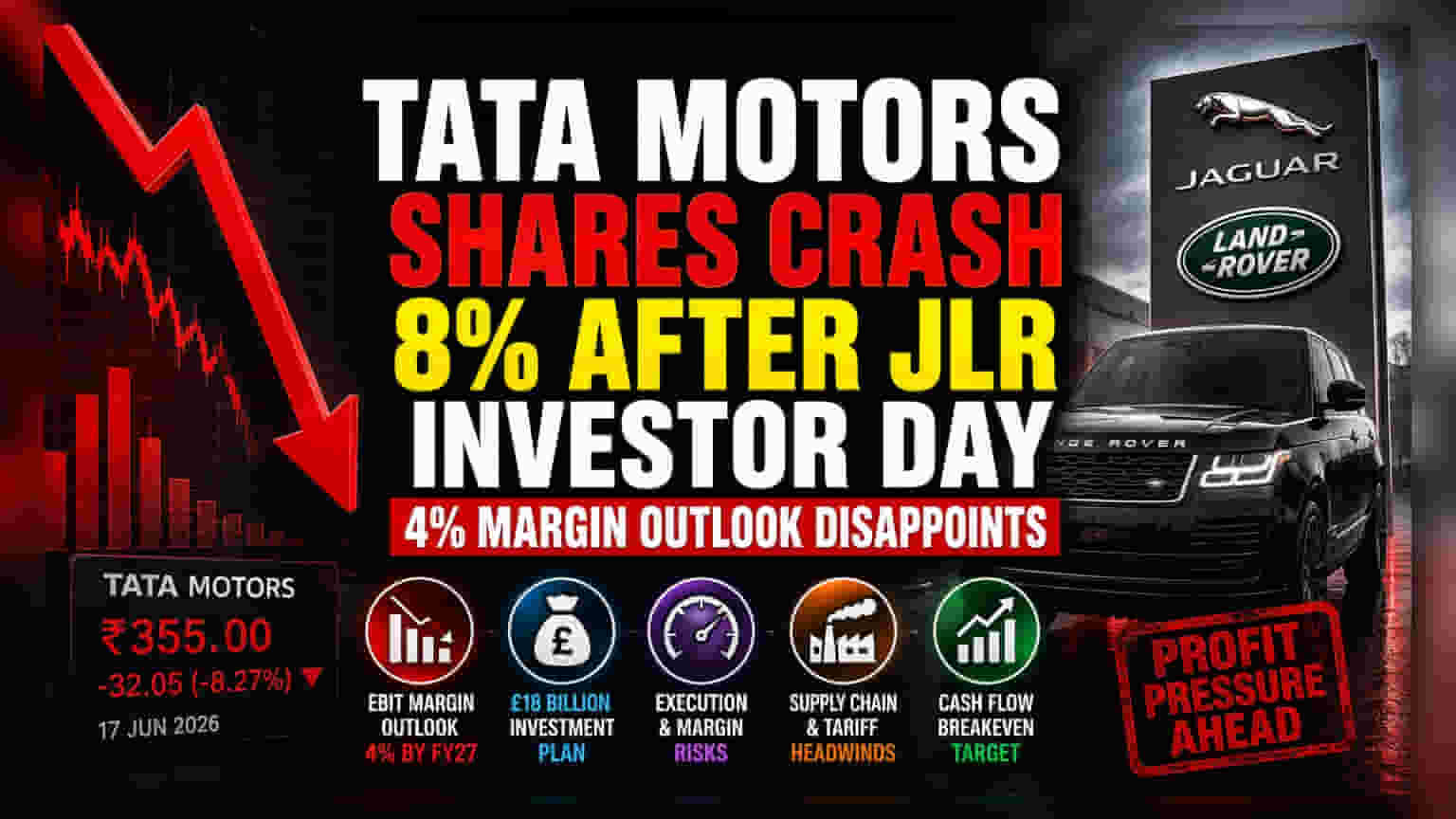

Tata Motors shares saw a sharp decline on Wednesday, June 17, 2026, closing 8.27% lower for the day after hitting an intraday low of Rs 355. The sell-off followed the investor day event held by Jaguar Land Rover (JLR), a critical subsidiary of the Tata group. While the company presented a roadmap for growth, the market reacted negatively to the profitability outlook provided by JLR management.

The Profitability Disappointment

At the heart of the investor concern is the EBIT margin guidance. JLR projected its EBIT margin—a key measure of operating profitability—to reach 4% by fiscal year 2027. While this represents a recovery from near-zero levels in the previous year, market analysts had anticipated a higher figure. In the stock market, when a company provides guidance that misses the street's expectations, investors often reduce their holdings, leading to downward price pressure. This reaction highlights that investors are currently more focused on the company's ability to turn revenue growth into higher profit margins rather than just topline expansion.

Strategic Investment vs. Execution Risk

JLR laid out an ambitious strategy, including a plan to invest £18 billion over the next five years to develop future technologies and new vehicle platforms. The company is pushing a 'House of Brands' strategy to target diverse luxury segments, particularly in the North American market, with models like the Range Rover and Defender. While this investment demonstrates a long-term commitment to growth, it also carries significant execution risk. Large capital spending projects require consistent demand and stable supply chains to ensure they pay off. Any delay in these projects or a failure to meet demand could put further pressure on the company's balance sheet and cash flow.

Financial Context

Recent financial data for Tata Motors Passenger Vehicles (TMPV) reflects the challenges the company is navigating. In the fourth quarter of FY26, the company reported a 32% year-on-year decline in consolidated net profit to Rs 5,783 crore, despite a 7% rise in revenue to Rs 1.05 lakh crore. This trend of rising revenue coupled with falling profit indicates that the company is facing margin pressure, likely due to rising costs or competitive pricing. On a standalone basis, while revenues grew significantly by 43% to Rs 18,598 crore, profits after tax fell by more than half, showing the difficulty in maintaining healthy margins in the current environment.

Market Headwinds

Beyond the margin guidance, JLR acknowledged several external pressures that are impacting its operations. These include potential tariffs, ongoing supply chain disruptions—exacerbated by a recent supplier fire—and general uncertainty in the global automotive sector. Furthermore, the company noted that it does not currently manufacture its core luxury models like the Range Rover and Defender within the United States. This structural limitation may hamper its ability to fully capture the demand in the North American market, particularly under certain trade policies.

What Investors Should Track

Going forward, the key monitorable for investors will be how effectively the company manages its costs and improves margins toward the 4% target and beyond. Shareholders will likely look for updates on cash flow, especially after the company indicated a goal to reach operating cash flow breakeven in the current financial year. Additionally, management’s ability to stabilize the supply chain and navigate trade barriers will be crucial to determining whether the current strategic investments can deliver the expected returns.