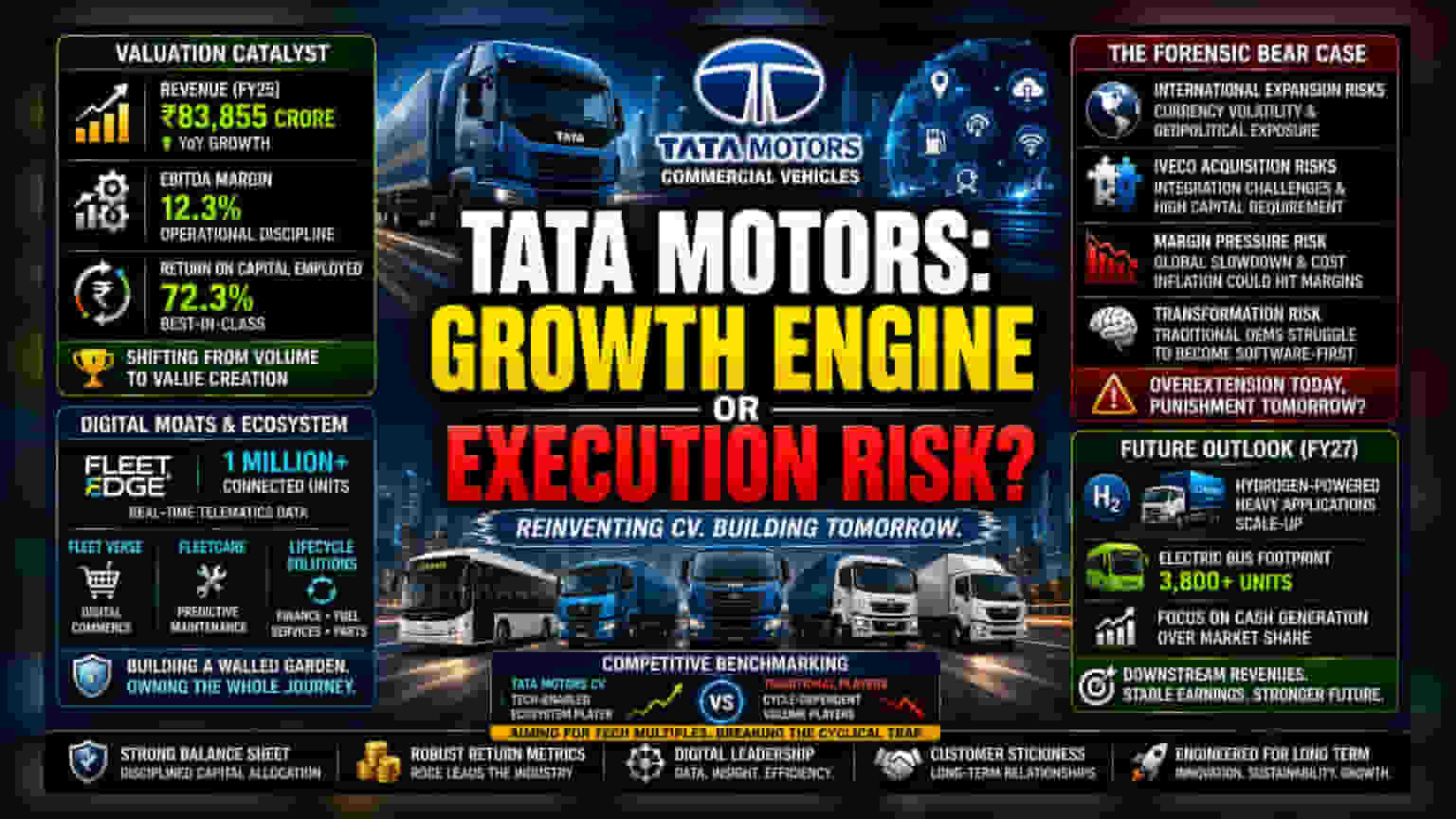

The Valuation Catalyst

Recent financial disclosures confirm a fundamental shift in the operational architecture of Tata Motors' commercial vehicle division. Moving away from the traditional volume-at-all-costs manufacturing model, leadership is aggressively reallocating capital toward service-oriented verticals. This restructuring occurs as the company posts revenue of ₹83,855 crore, a notable expansion from the previous fiscal year. While the 12.3% EBITDA margin reflects operational discipline, the primary market focus is the 72.3% Return on Capital Employed, a metric that positions the division against high-performing software-as-a-service peers rather than stagnant heavy equipment manufacturers.

Competitive Benchmarking and Digital Moats

Unlike traditional domestic competitors that remain tethered to infrastructure spending cycles, Tata Motors is building a digital ecosystem through its Fleet Edge platform. With over one million units now feeding real-time telematics data back to the central hub, the firm is effectively creating a walled garden. This integration of Fleet Verse for digital commerce and specialized downstream services like FleetCare serves to lock in enterprise clients. By capturing the entire vehicle lifecycle—from financing and fuel management to predictive maintenance—the company is attempting to achieve the valuation multiples of a tech-enabled logistics firm, bypassing the standard cyclical discounts applied to the broader automotive sector.

The Forensic Bear Case

Despite these strategic aspirations, institutional skepticism remains centered on the execution risks inherent in such a massive operational metamorphosis. Expanding into international markets across Southeast Asia and Africa introduces significant currency volatility and geopolitical exposure that could offset gains in domestic efficiency. Furthermore, the proposed acquisition of Iveco Group, while theoretically expanding the technological footprint, introduces substantial integration hazards and capital expenditure demands. If the firm cannot maintain its current margin trajectory, the market may punish the stock for overextending its balance sheet during a period of global economic softening. Critics also point to the historical difficulty of traditional OEMs successfully transitioning into software-first businesses, noting that entrenched legacy culture often stifles the agility required to compete with native digital challengers.

Future Outlook and Strategic Guidance

Management has signaled a clear intent to prioritize cash generation over aggressive market share expansion. The roadmap for FY27 focuses on scaling hydrogen-powered heavy applications and broadening the electric bus footprint, which currently stands at over 3,800 units. Analysts remain focused on whether these downstream revenue streams can eventually account for a meaningful percentage of total earnings, thereby insulating the stock from the inevitable troughs in the heavy commercial vehicle replacement cycle.