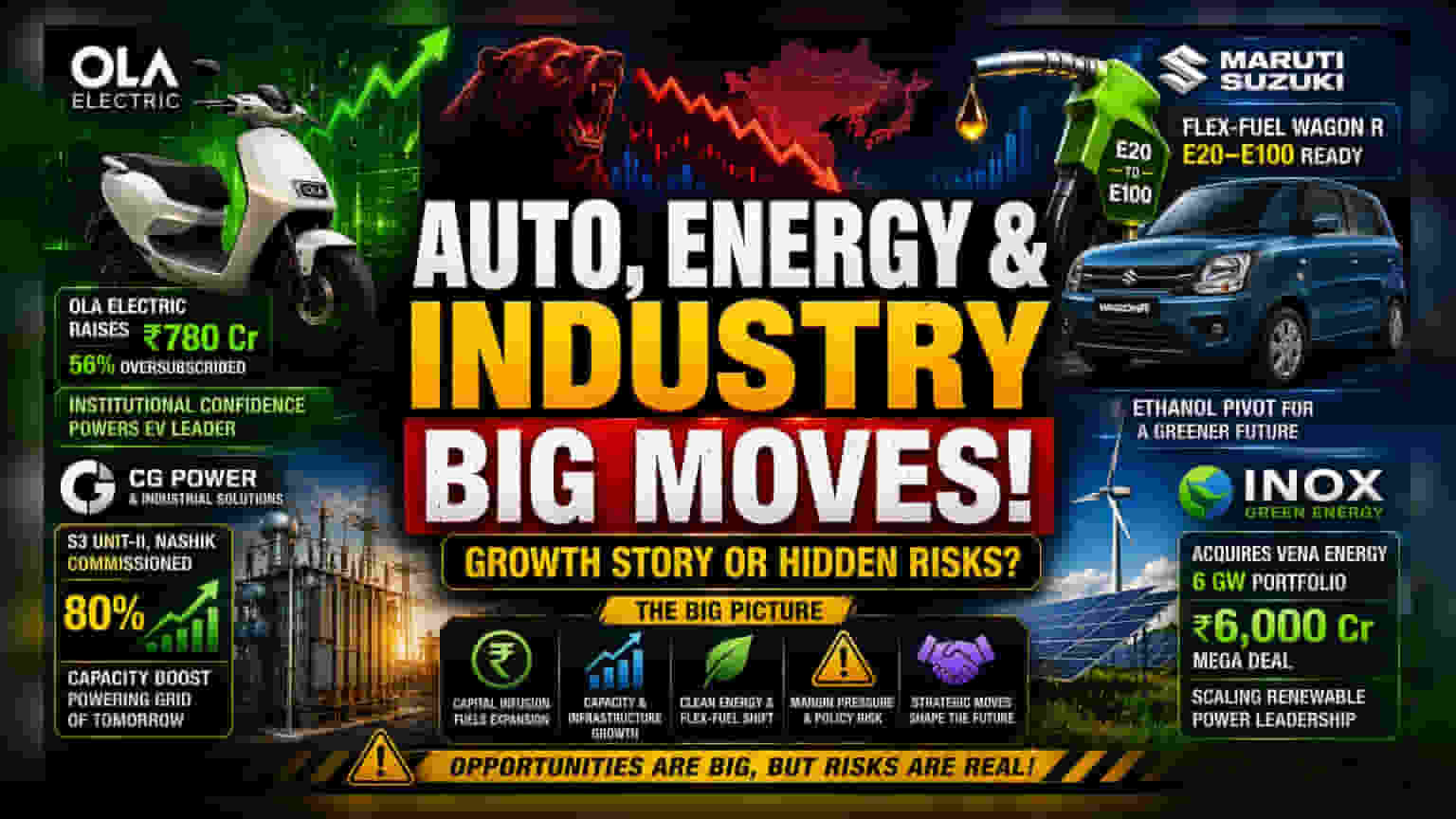

Institutional Confidence Meets EV Reality

Ola Electric’s successful capital raise of Rs 780 crore through a qualified institutional placement highlights a distinct divergence between retail sentiment and institutional backing. While the 56% oversubscription suggests strong institutional interest, it effectively introduces further equity dilution for existing shareholders. Investors are pricing this movement based on the company’s aggressive service network expansion rather than immediate profitability, which remains under pressure. This liquidity injection is critical for the firm to maintain its lead in the electric two-wheeler market as competition intensifies from traditional OEMs transitioning to battery-powered portfolios.

Maruti Suzuki’s Ethanol Pivot

The introduction of the flex-fuel Wagon R represents a strategic hedge for Maruti Suzuki rather than a wholesale abandonment of internal combustion engines. By enabling operation on E20 to E100 blends, the company is positioning itself to benefit from government-led biofuel mandates. However, the path to mass adoption faces significant hurdles, specifically the current lack of a nationwide ethanol-dispensing infrastructure. While this move aligns the firm with long-term carbon reduction targets, near-term margins remain tethered to the traditional petrol-engine cost structure, offering little reprieve from competitive discounting in the entry-level segment.

Industrial Expansion and Infrastructure Consolidation

Beyond consumer vehicles, the industrial landscape is shifting toward capacity enhancement. CG Power’s commissioning of its S3 Unit-II facility in Nashik is a calculated play on the surging demand for high-voltage power transmission, essential for integrating renewable energy into the national grid. This 80% capacity boost places the firm in a prime position to capitalize on government-backed transmission projects. Concurrently, Inox Green Energy’s Rs 6,000 crore acquisition of Vena Energy’s 6 GW portfolio signifies a major consolidation effort. This transaction is likely to weigh on near-term balance sheets due to the sheer size of the debt-funded acquisition, yet it fundamentally scales the company’s operational capacity to compete with larger independent power producers.

The Bear Case: Structural and Macro Headwinds

Despite these developments, systemic risks persist. The automotive sector faces continued margin compression as raw material costs remain volatile and entry-level demand remains sluggish. Regarding the aerospace JV, TVS Supply Chain Solutions is entering a highly capital-intensive, high-barrier sector where global incumbents command pricing power; a mere €2 million initial investment is arguably insufficient to move the needle on a consolidated basis. Furthermore, regulatory reliance remains a common thread—whether through ethanol mandates or renewable energy incentives—which introduces policy risk that could derail these capital expenditures should the government shift its fiscal priorities or subsidy structures in the coming quarters.