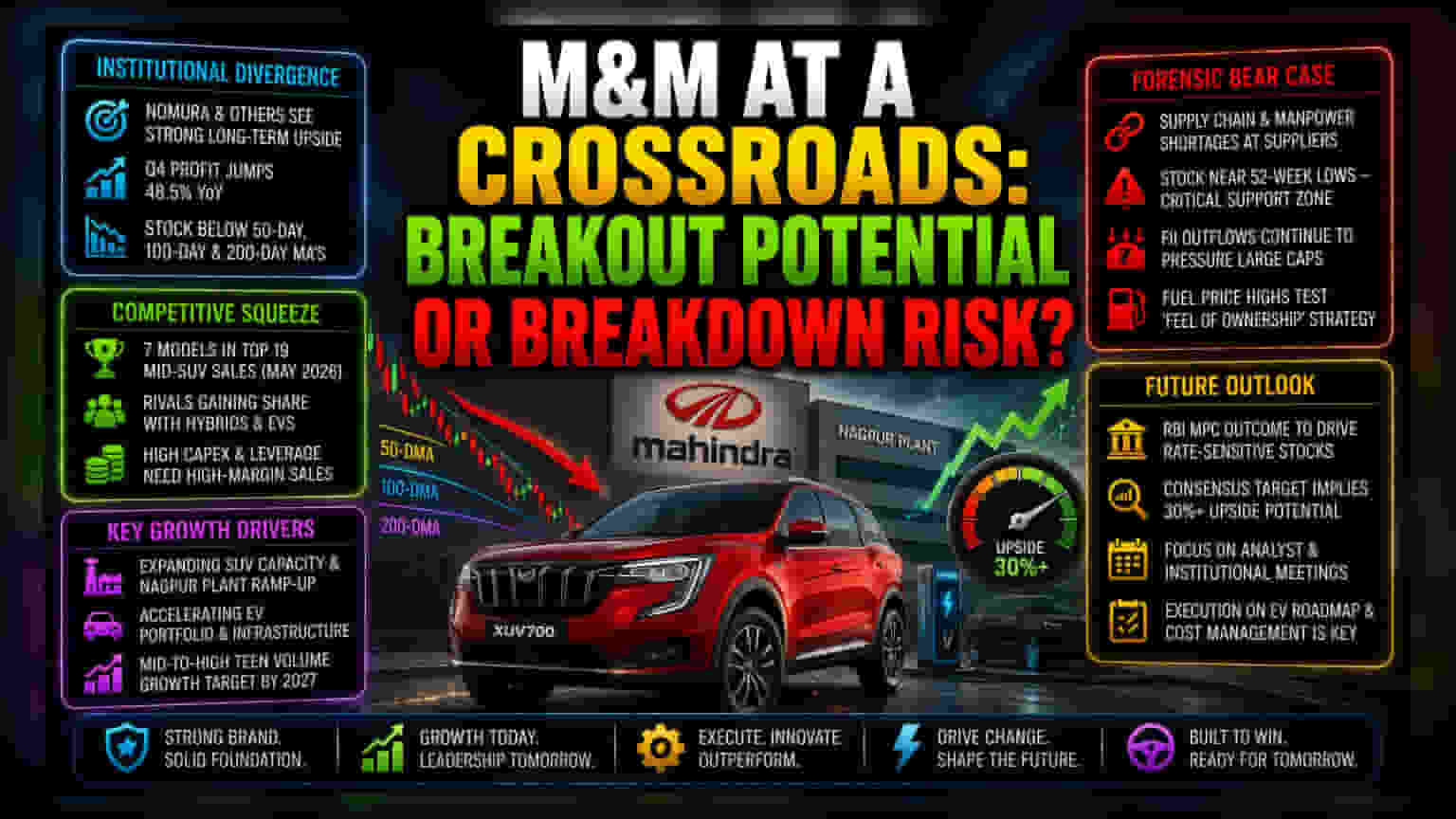

The Institutional Divergence

While Nomura and other major brokerages maintain high price targets for Mahindra & Mahindra (M&M), citing long-term expansion in SUV capacity and EV penetration, the market price reflects a different reality. The stock has faced significant technical pressure, recently trading below its 50-day, 100-day, and 200-day moving averages. This disconnect suggests that while the fundamental story—driven by a 48.5% year-on-year jump in Q4 profit—remains attractive to long-term institutional buyers, near-term traders are increasingly wary of momentum loss and sector-wide headwinds.

The Competitive Squeeze

Mahindra’s dominance in the SUV segment is facing a broader challenge as the Indian passenger vehicle market matures. While the brand successfully placed seven models in the top 19 mid-SUV sales charts for May 2026, it is no longer the sole contender. Rivals like Maruti Suzuki, Hyundai, and Tata Motors are aggressively capturing share through diversified SUV portfolios, hybrids, and competitive EV pricing. Unlike competitors that operate with leaner debt profiles, Mahindra’s aggressive capital expenditure for its Nagpur plant and EV infrastructure necessitates high-margin sales to offset its leverage. This reliance on the domestic market remains a double-edged sword; any cyclical downturn in rural tractor demand or urban SUV appetite leaves the company more vulnerable than diversified global peers.

The Forensic Bear Case

From a risk-averse perspective, the company’s recent performance is shadowed by operational bottlenecks. Management has acknowledged ongoing supply chain constraints, specifically citing manpower shortages at select suppliers that threaten to disrupt the ambitious production ramp-up required for FY27 targets. Furthermore, the stock is currently hovering just a few percentage points above its 52-week lows, a critical support level. A breakdown below this threshold could trigger a wave of technical selling, especially given the sensitivity to Foreign Institutional Investor (FII) outflows, which have been a consistent headwind for large-cap Indian stocks in June 2026. Additionally, M&M’s strategy of relying on “feel of ownership” to insulate itself from fuel price volatility is an untested thesis in an environment of sustained, high-energy costs.

Future Outlook

Looking ahead, the market is awaiting the outcome of the RBI Monetary Policy Committee meeting, which will likely dictate the sentiment for rate-sensitive stocks like M&M. While the consensus price target remains comfortably above current market levels—implying a potential 30%+ upside—the reality of the company's valuation depends on its ability to maintain mid-to-high teen volume growth through 2027 without compromising on margins. Investors are shifting focus toward the company's ability to navigate the upcoming analyst and institutional meetings to provide clarity on the EV roadmap and cost-management efficiency.