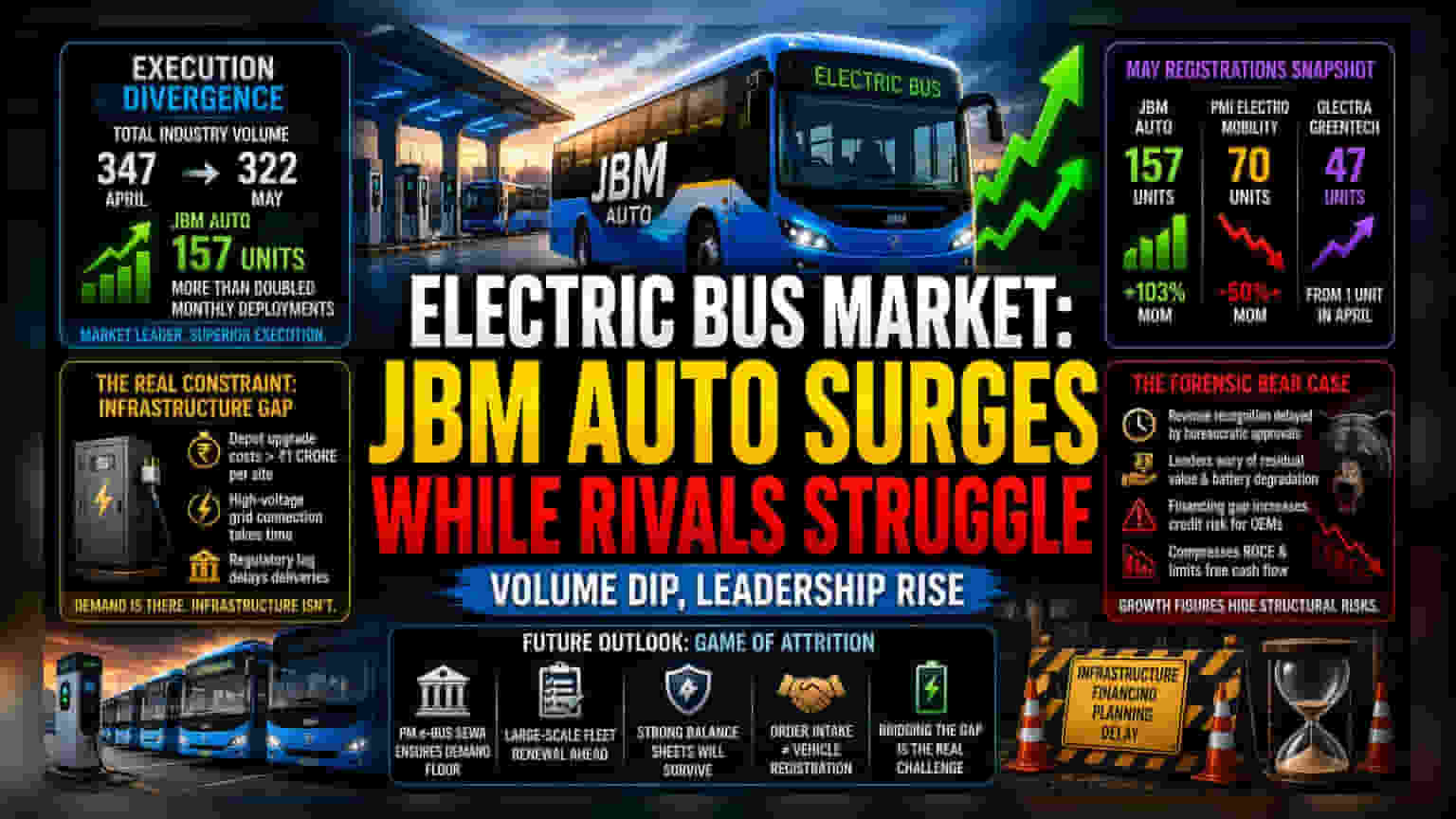

The Execution Divergence

The recent registration data reveals a stark bifurcation in India's electric bus market. While total industry volume contracted to 322 units in May from 347 in April, JBM Auto decoupled from this trend by more than doubling its monthly deployments to 157 units. This performance is not merely a sign of market leadership but a manifestation of superior operational logistics. Companies failing to secure the high-voltage grid connections and depot space required for these heavy vehicles are effectively being priced out of the delivery cycle, regardless of their order books.

Analytical Comparison of Market Performance

Market volatility is currently punishing firms lacking the balance sheet strength to weather long-dated Gross Cost Contract (GCC) cycles. PMI Electro Mobility, which previously held the industry lead, saw its output contract by over 50% month-over-month. Meanwhile, Olectra Greentech’s volatile output—swinging from a single unit in April to 47 in May—underscores the erratic nature of supply chain and site readiness. Unlike the passenger car segment, where inventory can be pushed to dealers, electric bus manufacturers are tethered to the physical readiness of state transport depots. This dependence creates an environment where historical performance is a poor predictor of future delivery capability.

The Forensic Bear Case

Behind the headline growth figures lie systemic risks that investors frequently overlook. The primary constraint is not demand, but the 'last mile' of infrastructure. Upgrading a depot to support high-voltage charging requires a capital outlay exceeding ₹1 crore before a single charger is even commissioned. Furthermore, the regulatory lag in securing electricity board approvals acts as a hidden ceiling on growth. For manufacturers, this implies that revenue recognition is consistently delayed by external bureaucratic factors. Additionally, lenders remain deeply skeptical regarding the residual value of EV bus assets and long-term battery degradation profiles. This financing gap forces manufacturers to shoulder significant credit risk or negotiate stringent collateral terms, which directly compresses return on capital employed (ROCE) and limits free cash flow generation.

Future Outlook and Sector Resilience

The reliance on government-mandated procurement, specifically the PM e-Bus Sewa initiative, provides a floor for demand but restricts pricing power. As the industry shifts from initial pilot projects to large-scale fleet renewals, the ability to manage debt and maintain liquid operational capital will distinguish the long-term survivors. Market expectations suggest that until the government addresses the financing hurdles for private operators, the sector will remain a game of attrition where only those with strong balance sheets can bridge the gap between order intake and vehicle registration.