India's Kharif sowing reached 84.6 lakh hectares by June 12, marking a 3.9% decline compared to last year. While rice planting saw a 28% jump due to early monsoon, cotton and pulses saw sharp drops of 27.8% and 43%, respectively. This data is critical for investors tracking food inflation, agri-input demand, and rural consumption trends.

What Happened

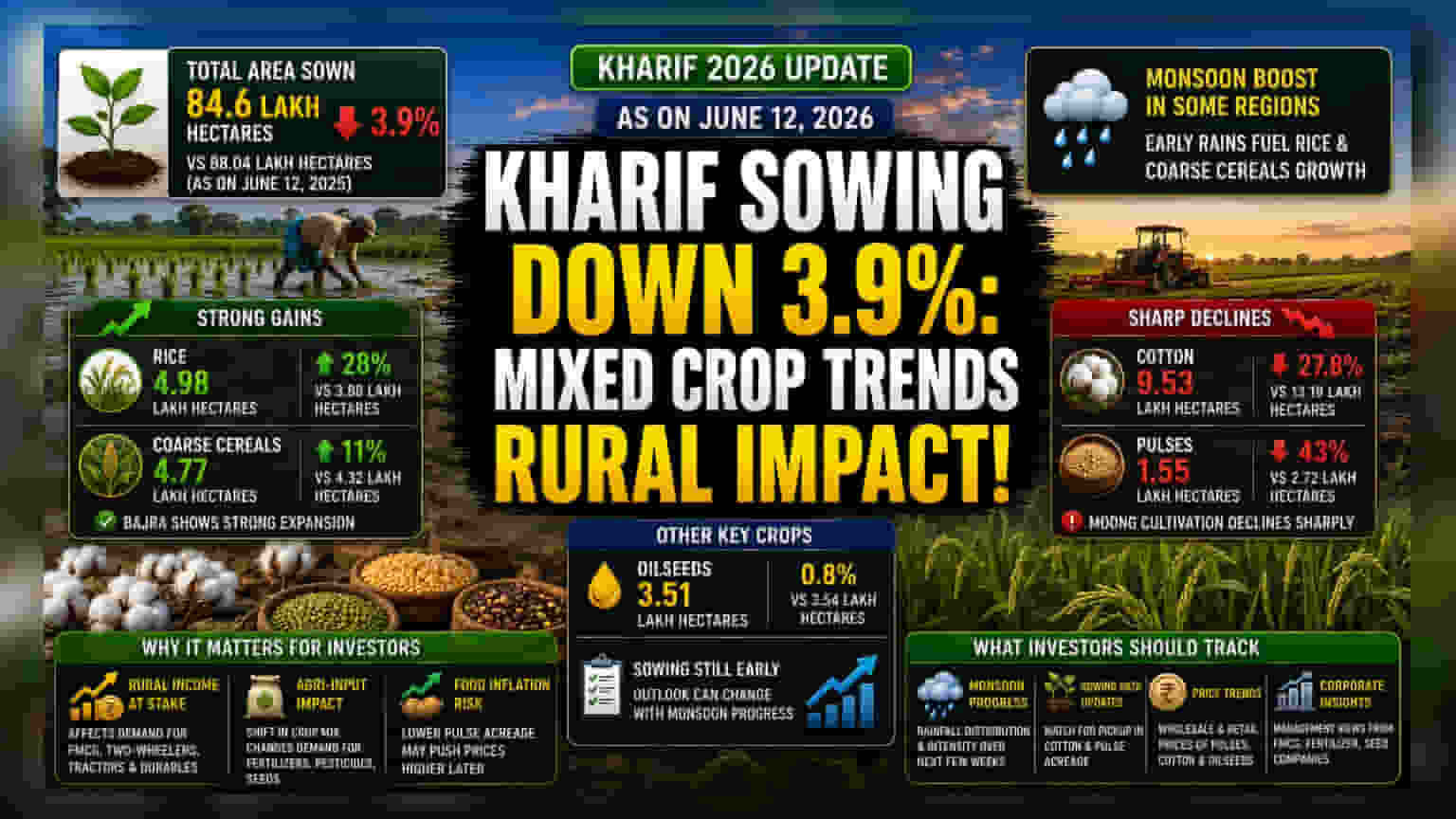

Latest data from the Ministry of Agriculture shows that as of June 12, 2026, the total area covered under Kharif crops stands at 84.6 lakh hectares. This is a decline of 3.9 percent compared to the 88.04 lakh hectares recorded during the same period in 2025. While total sowing is trailing slightly, the composition of crops being planted shows a mixed picture, heavily influenced by the early arrival of the monsoon in specific regions.

Understanding The Crop Mix

The most notable shift in the current planting season is the significant surge in rice acreage. Rice planting increased by 28 percent to 4.98 lakh hectares, compared to 3.88 lakh hectares in the previous year. This growth is largely credited to the favorable onset of the monsoon in key rice-growing areas. Coarse cereals also followed a similar positive trend, with acreage rising to 4.77 lakh hectares from 4.32 lakh hectares, with bajra seeing a strong expansion.

In contrast, key cash crops and pulses have struggled. Cotton sowing has faced a sharp drop of 27.8 percent, with the area falling to 9.53 lakh hectares from 13.19 lakh hectares. Pulses have seen an even steeper decline of approximately 43 percent, with acreage dropping to 1.55 lakh hectares. Among pulses, the decline in moong cultivation has been particularly sharp.

Why This Matters For Investors

Investors tracking the rural economy and agricultural sector often view these trends as early indicators for several industries. The significant drop in pulse acreage, if not recovered in the coming weeks, could lead to supply concerns later in the year, potentially impacting food inflation. For consumer companies, this creates a situation where food price trends will need to be monitored closely.

For companies in the agri-input sector, such as those producing fertilizers, pesticides, or seeds, the crop mix is important. A shift toward rice often requires a different product mix compared to cotton or pulses. If the reduction in cotton and pulse sowing persists, it may impact demand for specific crop-protection chemicals designed for those crops.

Sector Pressures To Watch

The current decline in cotton and pulse acreage highlights the sensitivity of Indian agriculture to weather patterns and regional rainfall distribution. While the monsoon has helped rice, the delay or lower interest in cotton and pulses suggests that farmers might be waiting for better soil moisture conditions or making decisions based on past price realizations and local weather forecasts.

Another point to note is the stability in oilseeds, which covers 3.51 lakh hectares, close to the previous year's 3.54 lakh hectares. Stability in this segment is generally positive for supply chain consistency, but investors will look for whether this trend continues as the monsoon progresses.

What Investors Should Track

The most important monitorable for the coming weeks is the distribution and intensity of monsoon rainfall. Since the sowing season is still in its early stages, the overall picture can change rapidly. Investors should look for updated data on acreage, as a pickup in cotton and pulse sowing could offset the current shortfall. Additionally, tracking wholesale and retail price trends for pulses and cotton will provide insight into how the market is anticipating the upcoming harvest. Management commentary from companies in the FMCG, fertilizer, and seed sectors during upcoming earnings calls will also be valuable to understand how they are adjusting to these planting shifts.