India's Edible Oil Industry Seeks Freight Aid Amid Rising Costs

The Solvent Extractors’ Association of India (SEA) has formally asked the Indian government for help with escalating costs in the edible oil sector. The industry is requesting freight cost subsidies and priority berthing for import vessels. This plea comes as a complex mix of global factors is driving up import expenses while also creating unexpected opportunities for domestic oilseed crushing operations.

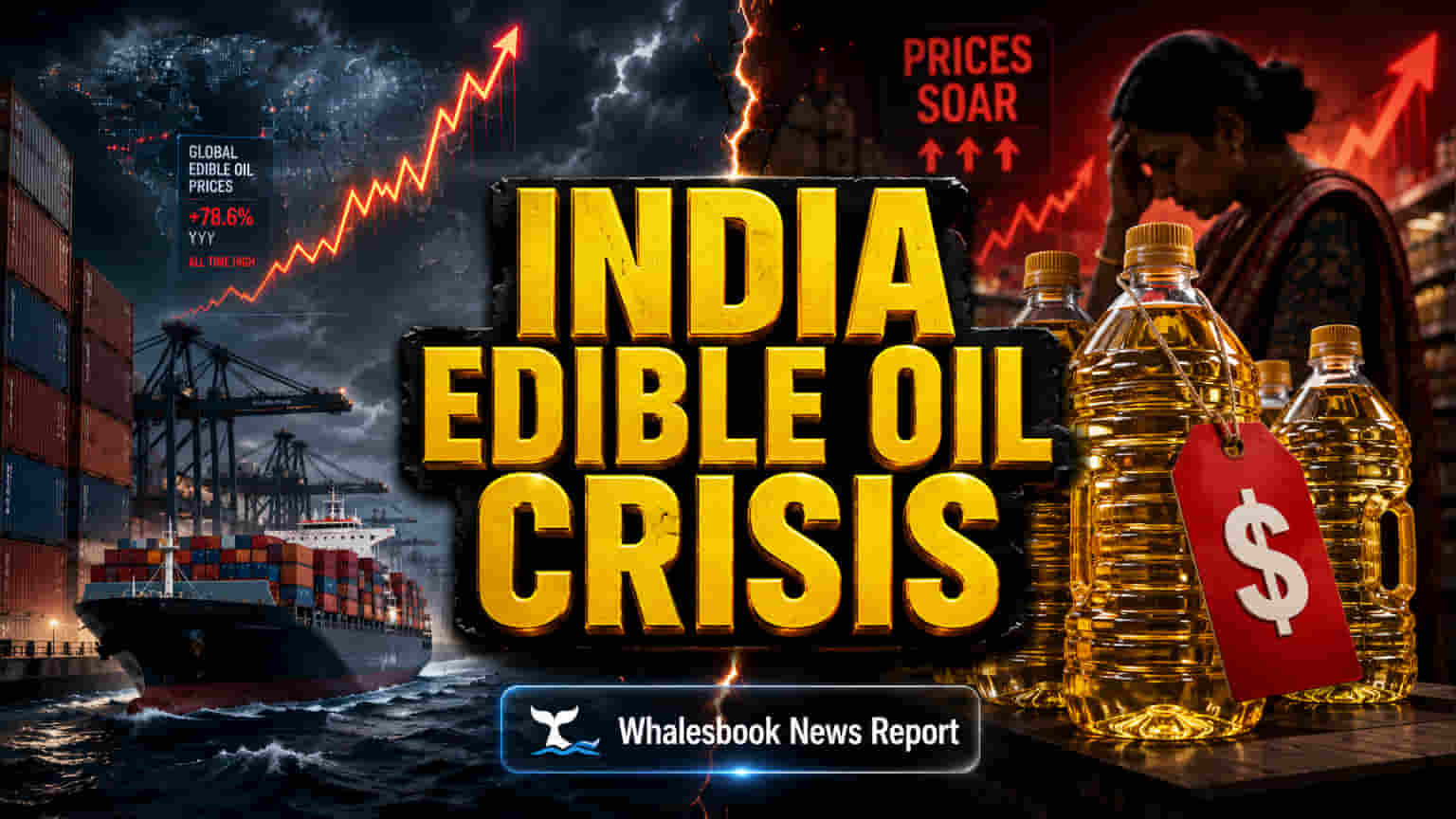

Freight Costs Surge

Global shipping rates have dramatically surged, nearly doubling on key trade routes. For example, shipments from Argentina to Indian ports now cost about $140-145 per tonne, up from $70-75. Freight from Russia has climbed from roughly $55 to $90-95 per tonne, and routes from Malaysia and Indonesia have seen costs rise from $40 to $55 per tonne. These higher freight charges directly increase the cost of imported edible oils. The SEA reports that by May 8, 2026, crude palm oil prices had climbed 20% year-on-year to $1250/tonne, soybean oil rose 17% to $1295/tonne, and sunflower oil increased 16% to $1325/tonne. Crude palm oil at Kandla port recently rose nearly 16% to INR 1,341 per 100 kg since late February 2026. Current packaged retail prices on May 11, 2026, show these pressures: sunflower oil at ₹175.40/kg, soybean oil at ₹148.87/kg, and palm oil at ₹134.72/kg.

Global Drivers and Domestic Paradox

The surge in vegetable oil prices is closely tied to growing demand from the biofuel sector. Indonesia and Malaysia, for instance, are boosting their biodiesel blending mandates. This global trend, along with higher crude oil prices stemming from geopolitical tensions in West Asia, has increased demand for palm and soybean oils for biofuels. The West Asia conflict has disrupted global commodity markets, affecting freight, energy, and currency, which raises import costs for countries like India that rely heavily on overseas supplies. However, these higher global prices and supply issues are also boosting India's domestic crushing industry. Local edible oil prices are rising alongside imported oil prices, keeping mustard prices above the Minimum Support Price (MSP) of Rs. 6200/- per quintal. In April 2026, a record 1.6 million tonnes of rapeseed-mustard was crushed, helping to soften the impact of imported oils on domestic prices.

Consumer Price Pressures Persist

Despite these domestic efforts, average retail prices for major cooking oils across India have risen 7-12% year-on-year. Soybean oil is up 8% to Rs 159 per litre, mustard oil has increased 12% to Rs 189 per litre, and sunflower oil is up 8% to Rs 187 per litre. Some reports show a broader increase of 5-14% year-on-year for key cooking oils. This price jump directly impacts household budgets, as edible oils are a staple in Indian diets. India imports about 57% of its annual edible oil needs, totaling 25-26 million tonnes, mainly from Indonesia, Malaysia, Ukraine, Russia, and Argentina. This reliance on imports leaves the country vulnerable to international price swings and supply chain disruptions.

Structural Vulnerabilities and Consumer Impact

India's significant reliance on edible oil imports, estimated at around 60% of its demand, poses substantial structural risks. The country's import bill for edible oils reached nearly Rs 1.61 lakh crore (USD 18.3 billion) in the 2024-25 marketing year. Although domestic production has improved slightly, self-sufficiency is still only around 44%. Global price volatility, worsened by geopolitical tensions like the West Asia conflict and climate risks such as El Nino, can quickly lead to inflation in India. Unlike some major producers who use biofuel mandates to support domestic demand, India faces a greater financial burden on its budget when global prices increase. Additionally, current logistics issues, including a lack of suitable vessels and rerouting due to uncertain shipping routes, add further costs and delays. The combination of these factors, alongside potential government inaction on subsidy requests, creates an uncertain outlook for price stability and consumer affordability. While domestic crushing shows strength, the overall system remains vulnerable to external shocks.

Future Outlook

Industry groups forecast domestic edible oil production to reach about 9.6 million tonnes in the 2025-26 marketing year. This would cover only around 40% of the country's demand, requiring imports of roughly 16.7 million tonnes. The government's National Mission on Edible Oils (NMEO) aims to increase domestic oilseed production, targeting output of 69.7 million tonnes by 2030-31 and edible oil production of 20.2 million tonnes. However, reaching these goals needs continuous policy support and effective management of global supply chain risks. Prime Minister Modi recently urged reduced edible oil consumption to curb import dependence and save foreign exchange, indicating a long-term strategy for self-reliance amid global uncertainties.