Sector Resilience Amid Market Downturn

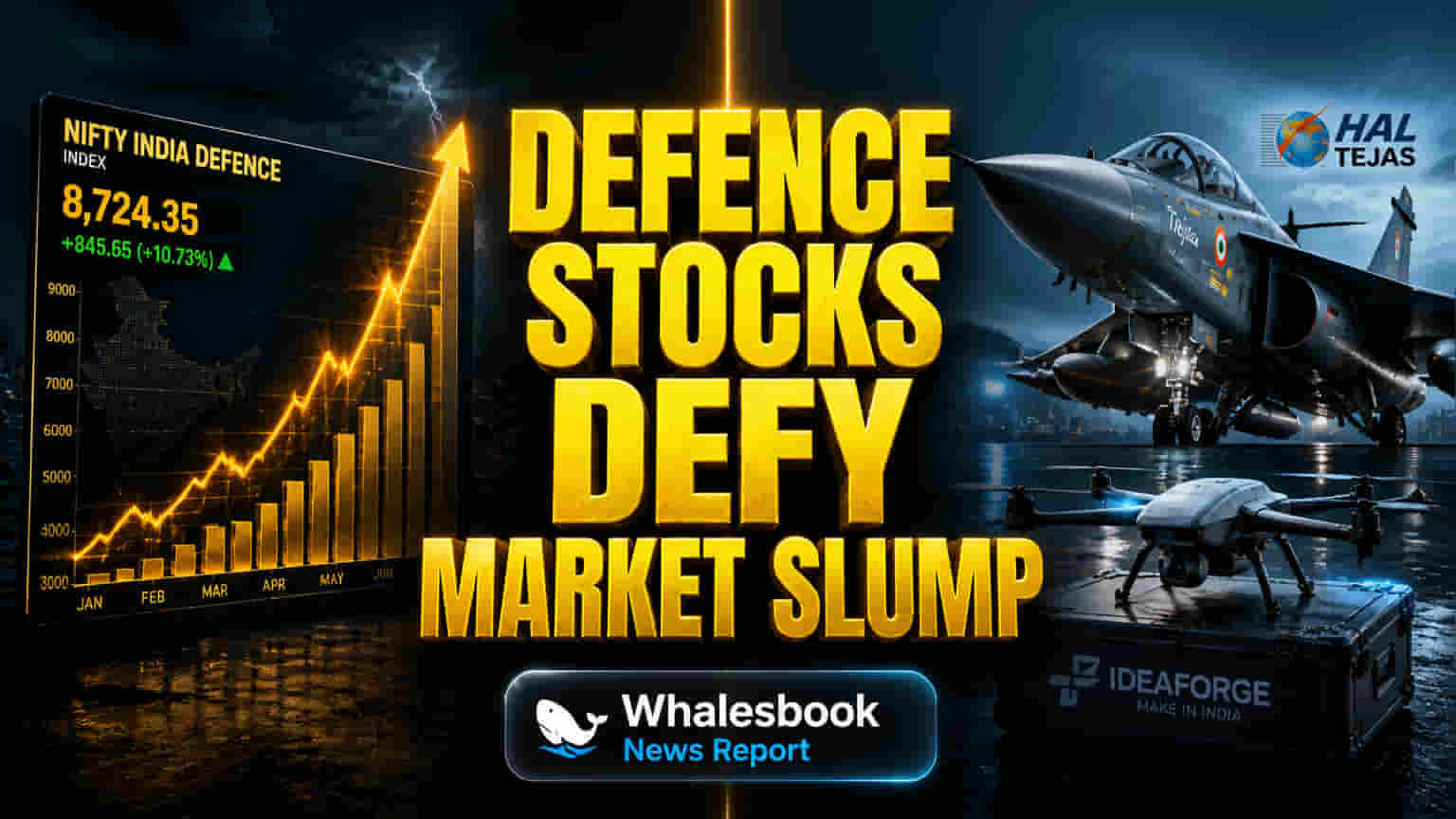

India's defense sector showed resilience, with the Nifty India Defence index nearing its 52-week high, standing out against a weaker broader market. This strength isn't uniform, however, as different growth stories are emerging among key players. While established companies like Hindustan Aeronautics Limited (HAL) are supported by major government contracts, newer technology firms are attracting investor interest with advanced applications, though with high market valuations.

The Core Catalyst: Order Books Versus AI Bets

HAL saw its shares climb about 3% intraday on Tuesday, May 5, 2026. This rise is backed by an order book exceeding ₹2.54 trillion as of March 2026, nearly eight times its projected FY26 revenue. This backlog offers substantial earnings visibility for HAL, with expected growth in Tejas aircraft production boosted by GE engine deliveries. The company's focus on aircraft, helicopters, aero-engines, and avionics positions it for steady, contract-driven growth.

In contrast, Ideaforge Technology, a leader in unmanned aircraft systems (UAS), recently hit a 52-week high of ₹796.30. Its stock has jumped over 97% in the past month. This rally follows its strongest quarterly performance in Q4FY26, with revenues of ₹141 crore and profits after tax of ₹60 crore, alongside record annual order bookings of ₹530 crore for FY26. The company is actively developing combat drones and EW-resilient systems, aligning with evolving defense strategies.

MTAR Technologies has also seen significant gains, rising 160% year-to-date in 2026. Its growth is closely tied to the global AI infrastructure boom, where it supplies critical components for data center power solutions through its partnership with Bloom Energy. Analysts note MTAR's key role in supplying power solutions for AI data centers, supported by a decade-long partnership.

The Analytical Deep Dive

India's defense industry, valued at roughly USD 31.76 billion in 2026, is expected to grow at a CAGR of 4.05% to reach USD 38.73 billion by 2031. This growth is driven by government commitment to domestic procurement and modernization. The Union Budget 2026-27 allocated a record ₹7.85 lakh crore to the Ministry of Defence, with capital outlay increasing by nearly 22%, signaling sustained government support for local manufacturing and technological advancement.

Valuation metrics show a diverging picture. HAL's trailing P/E ratio is around 34.45 to 44.3, reflecting its stable earnings and large order book. MTAR Technologies, however, trades at a much higher P/E, with trailing ratios reported around 249.06 to over 300, indicating high growth expectations priced in by the market. Ideaforge, while not having an explicit P/E in the provided searches, has shown a near 97% stock increase in one month, suggesting an aggressive valuation premium for its high-growth technology segment.

Competitively, HAL faces emerging private players like Tata Advanced Systems Limited (TASL), which is leading significant programs like the C-295 aircraft and is shortlisted for the AMCA prototype, adding a new dynamic to HAL's established dominance. MTAR's core strength lies in specialized component manufacturing for critical sectors, setting it apart from broader defense equipment makers. Ideaforge operates in the fast-growing drone market, competing with both domestic and international firms.

Key Risks and Challenges

Despite the sector's positive momentum, significant risks persist. The high P/E ratios for MTAR Technologies and Ideaforge Technology suggest their stock prices may be valuing future growth and tech adoption too optimistically. A slowdown in AI infrastructure buildout, slower adoption of advanced drones, or competitive pressures could lead to substantial valuation corrections. MTAR's debt-to-equity ratio is higher than the industry median.

For HAL, while the order book provides a safety net, execution risks remain. Production delays, reliance on specific government tenders, and increasing competition from private players like TASL, which is taking on prime contracting roles in advanced projects, could challenge HAL's market share and growth. The defense sector's inherent dependency on government policy and budget allocation means any shifts in fiscal priorities or geopolitical events could impact order flows. Furthermore, long project cycles and milestone-based revenue recognition mean earnings can fluctuate.

The Future Outlook

Analysts remain largely positive on the sector, particularly on companies like MTAR Technologies, with Motilal Oswal reiterating a 'Buy' rating and a target price of ₹6,000, citing its strong positioning in AI infrastructure. ICICI Securities has set a target price of ₹4,960 for HAL, indicating expected upside from its current levels. The Nifty India Defence index has shown a 1-year return of approximately 25.33%, and earnings are forecast to grow by 19% annually within the Aerospace & Defense industry. The government's continued focus on indigenization and modernization through substantial budget allocations is expected to fuel demand for both established and emerging defense players, though stock performance will likely vary based on technological specialization and valuation multiples.