📉 The Financial Deep Dive

Medi-Caps Limited has announced its un-audited financial results for the quarter and nine months ended December 31, 2025 (Q3 FY26 & 9M FY26), presenting a mixed picture driven by strong standalone performance and a consolidated turnaround, albeit with a critical reporting discrepancy.

The Numbers:

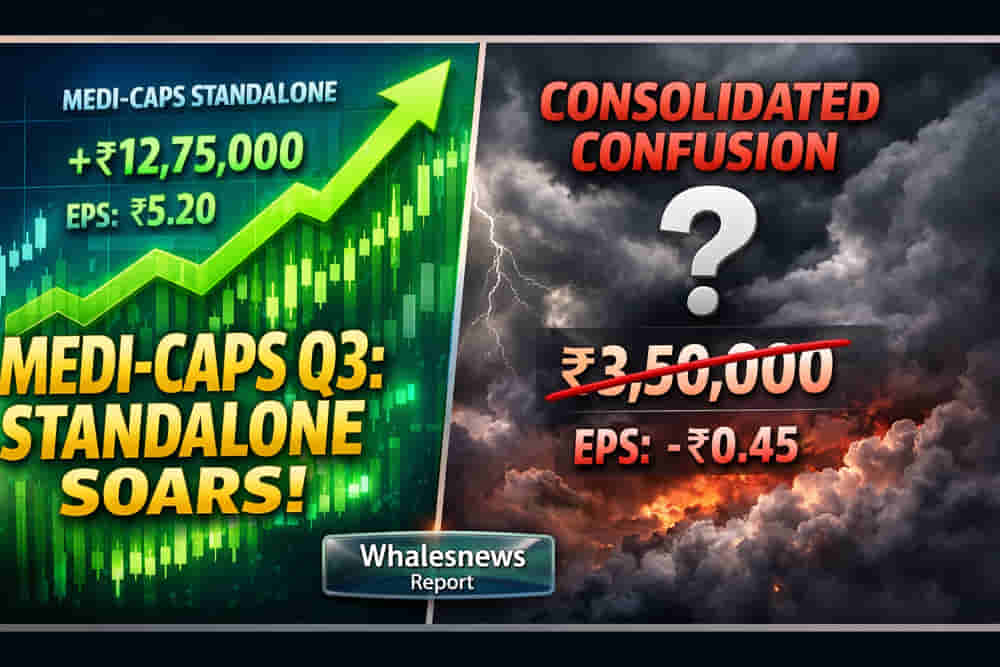

Standalone Performance: The company reported a stellar standalone revenue from operations of ₹77.28 Lakhs for Q3 FY26, marking a substantial 197% year-on-year (YoY) increase from ₹26.04 Lakhs in Q3 FY25. Standalone Net Profit saw a modest 7.6% YoY growth to ₹28.50 Lakhs, with Basic EPS improving to ₹0.23 from ₹0.21. For the nine-month period (9M FY26), standalone revenue grew 16% YoY to ₹177.06 Lakhs. Crucially, standalone Net Profit turned around from a loss of ₹15.10 Lakhs in 9M FY25 to a profit of ₹17.42 Lakhs in 9M FY26, and Basic EPS improved to ₹0.14 from ₹-0.12.

Consolidated Performance: The consolidated operations demonstrated a significant turnaround from net losses to profits. In Q3 FY26, consolidated Net Profit was ₹76.53 Lakhs, a stark improvement from a net loss of ₹204.50 Lakhs in Q3 FY25. This was aided by a 5.8% YoY increase in consolidated revenue to ₹425.31 Lakhs and a substantial surge in 'Other Income' to ₹75.91 Lakhs.

The Quality & The Grill:

The most alarming aspect of the Q3 FY26 results is the contradiction within the consolidated figures. While the company reported a positive consolidated Net Profit of ₹76.53 Lakhs for both Q3 FY26 and 9M FY26, the corresponding consolidated Basic Earnings Per Share (EPS) figures are reported as ₹-0.61 for Q3 FY26 and ₹-4.88 for 9M FY26. This significant discrepancy between positive net profit and negative EPS demands immediate clarification from management and raises serious concerns about the accuracy and transparency of the financial reporting.

Furthermore, the consolidated turnaround for the nine-month period occurred despite a sharp 51.5% YoY decrease in consolidated revenue from operations to ₹897.40 Lakhs. The profit improvement was heavily reliant on a more than threefold increase in 'Other Income', which suggests that the core operating business is under pressure on a consolidated basis.

Risks & Outlook:

The primary risk for investors lies in the unexplained disparity between consolidated net profit and EPS. This could indicate accounting errors, misinterpretations of reporting standards, or potentially a deliberate obfuscation, all of which severely impact investor confidence. The reliance on non-operational income ('Other Income') for the consolidated profit turnaround also poses a sustainability risk.

Given the absence of any forward-looking guidance, balance sheet details, or cash flow information in this announcement, the outlook remains highly uncertain. Investors will be looking for an urgent explanation regarding the EPS anomaly and a clear strategy to address the declining consolidated revenue and bolster operating profitability.