1. THE SEAMLESS LINK

This performance underscores a shift in how the economy's hiring trajectory is perceived, moving from a potentially robust expansion to one characterized by a more subdued, albeit still positive, rate of job creation.

2. THE STRUCTURE

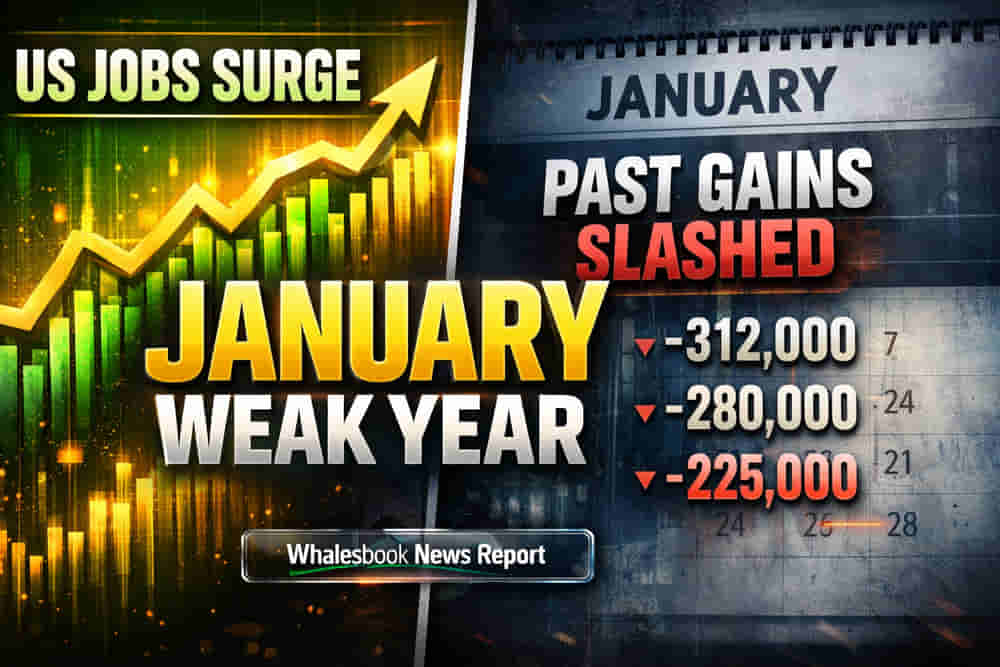

January Momentum vs. Historical Drag

The January jobs report presented a superficially strong picture, with payrolls climbing by 130,000, a figure comfortably exceeding the 55,000 consensus estimate. This gain, coupled with a reduction in the unemployment rate to 4.3%, suggested ongoing resilience in the U.S. labor market. However, the gloss was significantly dulled by the Bureau of Labor Statistics' (BLS) annual benchmarking adjustments. These revisions, derived from comprehensive tax records, revealed that job growth in the year leading up to March 2025 was 862,000 jobs lower than initially recorded. This recalibration indicated that 2025 saw the addition of only 181,000 jobs, a stark contrast to the previously reported 584,000, making it the weakest year for U.S. job creation since 2020. Markets reacted with tempered optimism, with initial gains in futures contracts being capped as investors digested the implications of the revised historical data. Bond yields and the dollar index saw modest increases following the report.

The Analytical Deep Dive

The stark contrast between the January headline and the annual revisions highlights a potential disconnect between monthly survey data and more complete economic accounting. Analysts are now grappling with whether January's figures represent a genuine rebound or an outlier against a backdrop of decelerating job creation. Economists suggest that the downward revisions could imply that earlier optimism about the pace of economic recovery was overstated. This divergence complicates the outlook for Federal Reserve policy. The stronger January jobs data, despite the downward historical revisions, has led traders to increase the probability of the Fed holding interest rates steady in March, potentially pushing back anticipated rate cuts. In contrast to the U.S., Eurozone employment growth in the second quarter of 2025 showed a more stable pattern, with a 0.1% quarter-over-quarter increase and 0.7% year-over-year growth, suggesting less volatility in its labor market compared to the U.S. data recalibrations.

The Forensic Bear Case

The substantial downward revision to annual job growth casts a long shadow over the economy's true vitality. While January's 130,000 jobs may look good on paper, it's crucial to recognize that this occurred against a backdrop where the prior year's hiring momentum was significantly weaker than previously understood. This suggests that the economy might be more fragile than headline figures let on, with underlying demand and hiring capacity potentially waning. The BLS data correction means that businesses were not expanding their workforces as aggressively throughout 2025 as previously believed, potentially signaling weaker consumer spending or corporate investment than anticipated. The risk here is that January's performance could be a temporary blip, a final burst of energy before a more pronounced slowdown, especially if global economic headwinds persist or domestic policy shifts impact corporate confidence and investment decisions. The revised historical data implies that the labor market's capacity to absorb shocks or sustain rapid growth is diminished, increasing vulnerability to any future economic downturn.

The Future Outlook

Forward-looking indicators and analyst sentiment are now attempting to reconcile this data conflict. While some see the January numbers as a positive signal for early 2026, many are tempering expectations due to the historical adjustments. The consensus is shifting towards a narrative of slower, more moderate job growth throughout the year, with a keen eye on whether January's performance can be sustained or if it was a fleeting anomaly. The Federal Reserve's upcoming policy decisions will likely be influenced by this dual narrative, balancing the current strength against revised historical context, potentially leading to a delay in anticipated monetary easing.