Procter & Gamble Health Q3 FY26: Revenue Surges, Profit Wobbles Amidst Strong Dividend Payout

Procter & Gamble Health Limited has unveiled its financial results for the third quarter and nine months ended December 31, 2025, revealing a tale of two halves: strong top-line expansion juxtaposed with a profit dip in the latest quarter, offset by substantial shareholder returns.

📉 The Financial Deep Dive

The Numbers:

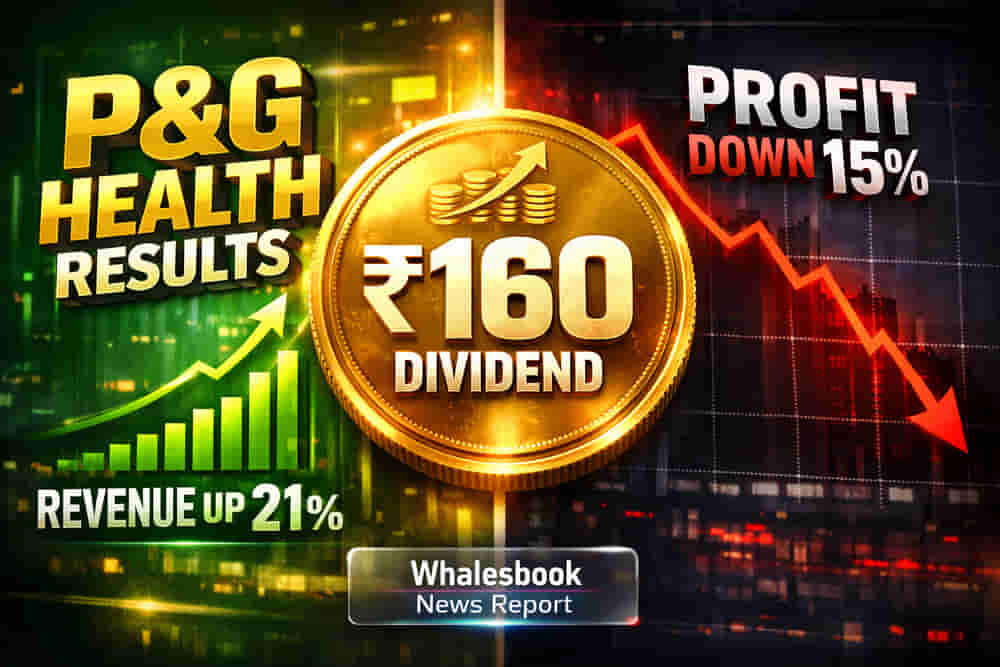

- Q3 FY26 Revenue: ₹373.86 Cr, a significant 20.7% year-on-year (YoY) increase from ₹309.77 Cr in Q3 FY25. Quarter-on-quarter (QoQ), revenue also rose 15.1% from ₹324.92 Cr in Q2 FY26.

- Q3 FY26 Net Profit: ₹77.59 Cr, marking a 14.6% decline YoY from ₹90.90 Cr in Q3 FY25.

- Q3 FY26 EPS: Basic and Diluted EPS stood at ₹46.74, down 14.6% YoY from ₹54.76.

- 9M FY26 Revenue: ₹1037.52 Cr, showing a 14.4% YoY growth from ₹907.06 Cr in 9M FY25.

- 9M FY26 Net Profit: ₹232.31 Cr, a robust 22.3% YoY increase from ₹190.01 Cr in 9M FY25.

- 9M FY26 EPS: Basic and Diluted EPS rose 22.3% YoY to ₹139.95 from ₹114.47.

The Quality:

The significant revenue growth in Q3 FY26 did not translate into a profit increase, indicating potential margin pressures or increased operating expenses. The reported Net Profit decline of 14.6% YoY for the quarter warrants attention, especially when compared to the strong 20.7% revenue jump. For the nine-month period, the reported profit growth of 22.3% was notably boosted by the absence of an exceptional item of ₹20.19 Cr (asset impairment and Goa plant sale consideration) that impacted 9M FY25 results. Excluding this one-off, the underlying profit trajectory requires closer examination.

The Grill:

(No analyst call transcript was provided with the filing.)

Risks & Outlook:

The divergence between strong revenue growth and declining quarterly profits is a key point of concern for investors, suggesting potential headwinds in cost management or competitive pressures affecting margins. However, the board's decision to declare a substantial interim dividend of ₹160 per equity share, including a special dividend of ₹50, is a strong positive signal to shareholders, indicating confidence in the company's cash generation capabilities despite short-term profit fluctuations. Investors will be keen to understand the sustainability of revenue growth and the drivers behind the Q3 profit compression in future communications.