1. THE SEAMLESS LINK

The reported third-quarter fiscal year 2026 profit after tax (PAT) of INR15.9 billion for Tata Motors fell below analyst expectations, underscoring margin pressures and operational challenges. This performance highlights a key concern: the gradual loss of market share across critical vehicle segments, a trend that predates the recent acquisition of Iveco. The integration of Iveco now exposes Tata Motors to amplified global macroeconomic uncertainties, a factor that could necessitate a stock de-rating if demand does not improve concurrently.

Margin Pressure and Market Share Erosion

Tata Motors' Q3 FY26 results revealed a profit after tax (PAT) of INR15.9 billion, a figure that trailed the estimated INR18.4 billion. This miss was largely attributed to a compressed margin of 12.8%, underperforming the projected 13.2%. The decline in profitability stems directly from elevated input costs, a persistent challenge impacting operational efficiency. Alongside margin compression, the company has been grappling with a steady erosion of its market share in key automotive segments. This dual pressure of cost increases and market share loss presents a significant hurdle for sustained financial performance.

Iveco Acquisition: A Strategic Gamble?

The recent acquisition of Iveco introduces a new layer of risk. While intended to bolster its commercial vehicle (CV) portfolio and global presence, the move integrates Tata Motors into the complexities of international markets and potential global economic downturns. Analysts suggest this acquisition could lead to a potential de-rating of the stock if the projected demand recovery does not materialize promptly, offsetting the integration risks. The €3.8 billion acquisition is Tata's largest to date, aiming to significantly expand its CV business revenue and EBITDA, positioning it more competitively against global peers like PACCAR and Traton SE, although Iveco itself is not a market leader in all its key markets.

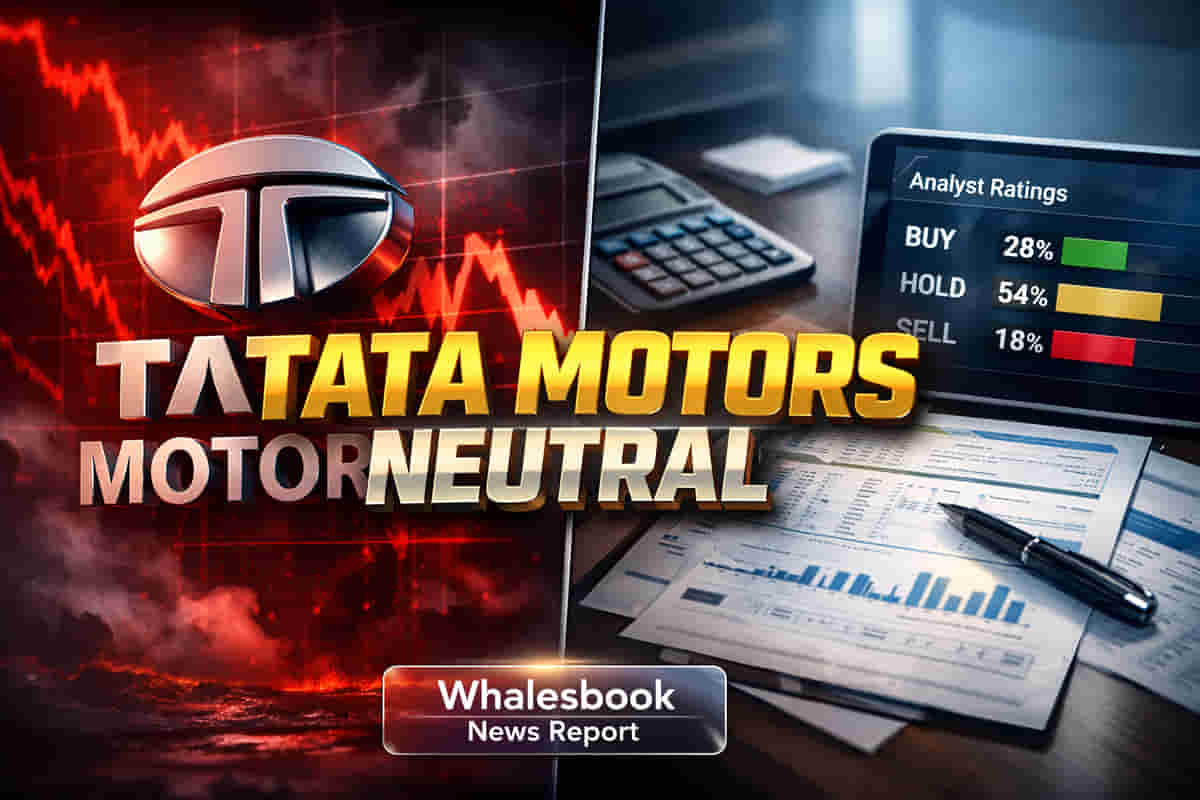

Valuation and Analyst Stance

Despite these headwinds, Motilal Oswal's financial models factor in a projected 9% volume compound annual growth rate (CAGR) for domestic commercial vehicle demand between fiscal years 2025 and 2028. Margins are also expected to remain stable at around 13% over the same period. However, following a recent rally, Tata Motors' stock is trading at approximately 24.1x FY27E and 21.8x FY28E earnings per share (EPS). Motilal Oswal considers this valuation to be fair, leading them to maintain a 'Neutral' rating on the stock. The firm has set a target price of INR431 per share. This valuation is derived by applying a 13x Dec '27E EV/EBITDA multiple to the core business, consistent with peer valuations, with an additional INR13 per share added for its stake in Tata Capital. As of February 1, 2026, Tata Motors' market capitalization stood at approximately ₹1,63,145 crore. Recent trading activity on February 2, 2026, saw the stock fluctuating between ₹435 and ₹443.55.

Sector Outlook and Competitor Landscape

The Indian commercial vehicle market is poised for strong performance, with projections for FY26 and FY27 to surpass the pre-pandemic FY19 record. This optimism is fueled by infrastructure development, GST rationalization, and fleet renewal needs. Tata Motors is a dominant player in this sector, with market capitalization around ₹1.65 lakh crore and a TTM P/E ratio of 20.6 as of January 2026. Competitors like Ashok Leyland have a market capitalization of approximately ₹1,13,365 crore and a TTM P/E of 42.0. In the passenger vehicle segment, Tata Motors secured its position as India's second-largest carmaker in January 2026, with domestic sales of 70,222 units, outpacing Mahindra & Mahindra and Hyundai Motor India. The company also continues to lead the Indian electric vehicle market, holding over 70% share. Despite this strong domestic performance, the stock faces headwinds from potential tariff reductions on EU-imported vehicles.