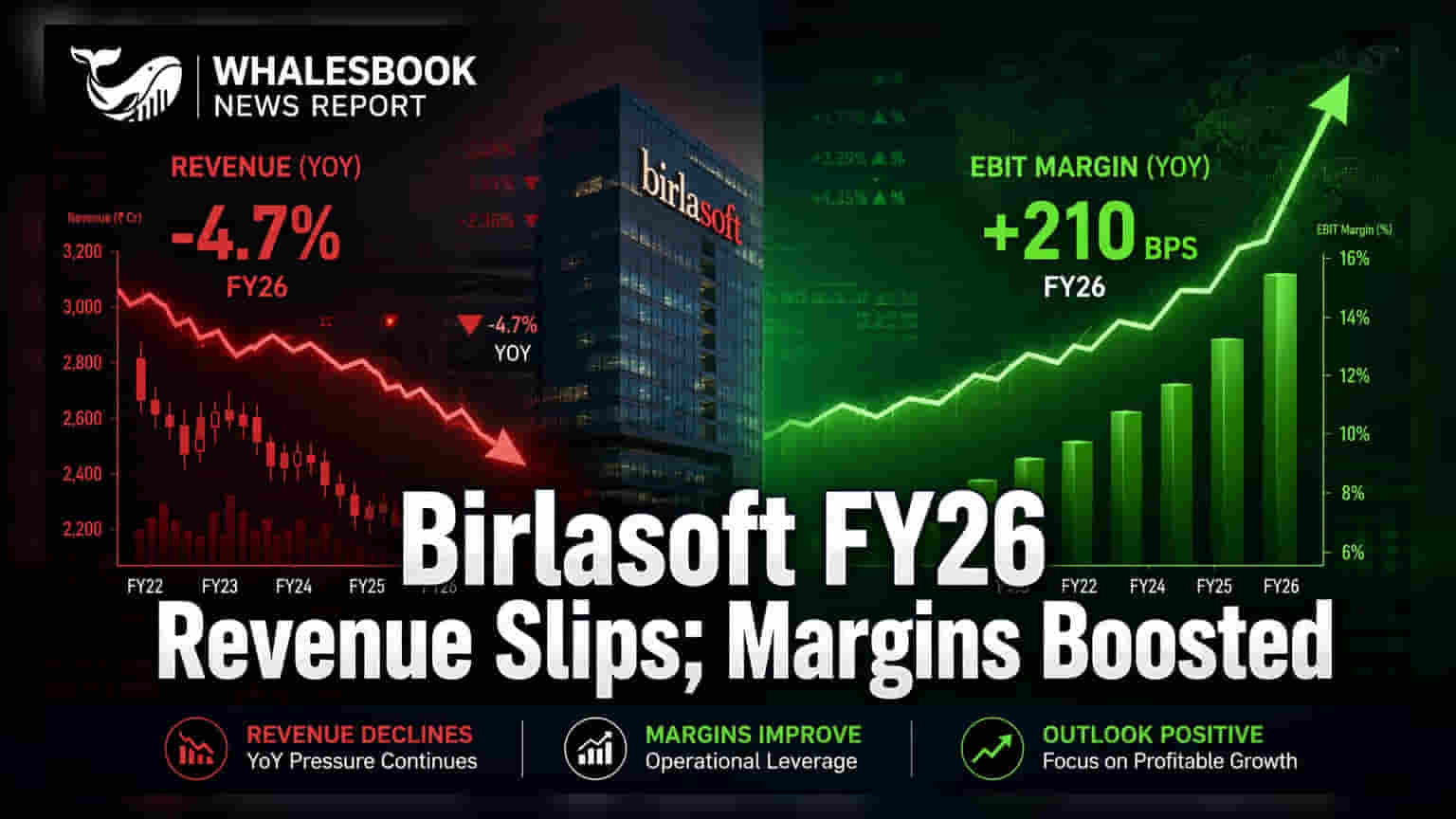

Birlasoft reported a 1.2% dip in FY26 revenue to ₹5,310 crore, impacted by strategic exits and soft demand. However, EBITDA jumped 24.2%, and margins expanded significantly, showing operational improvements. Profit remained stable. The company is focusing on an AI-first strategy.

Birlasoft FY26 Results: Revenue Dip, Margin Expansion Amid AI Focus

Birlasoft reported FY26 Revenue from Operations at ₹5,310 crore and EBITDA at ₹866 crore.

Reader Takeaway: Revenue decline masked by strong margin growth and AI investments.

What just happened

Birlasoft's revenue from operations for FY 2025-26 stood at ₹5,310 crore, a marginal decrease of 1.2% compared to ₹5,375.2 crore in the previous fiscal year. The company's EBITDA saw a significant increase of 24.2%, reaching ₹866 crore from ₹697.4 crore. Profit After Tax (PAT) was broadly stable at ₹518.4 crore, a slight increase of 0.3% from ₹516.8 crore in FY 2024-25. This stability in PAT was achieved despite the impact of one-time regulatory changes related to Labour Codes and higher US federal tax provisions.

Why this matters

The results highlight Birlasoft's strategic shift and operational efficiency gains. While the top line faced headwinds from a challenging global demand environment and the company's decision to exit non-profitable revenue streams, the substantial EBITDA growth and margin expansion (333 basis points to 16.3%) indicate effective cost management and a focus on higher-margin business. This operational discipline is crucial for sustaining profitability in a subdued technology spending landscape.

The backstory

Birlasoft has been increasingly focusing on an 'AI-First' operating model. Investments in proprietary platforms like 'Birlasoft Cogito' for Agentic AI and 'Lynx' for Unified Test Automation are central to this strategy. These initiatives aim to drive enterprise AI adoption and enhance delivery capabilities.

What changes now

With a stable PAT and improved margins, the company is better positioned to invest in its AI initiatives. The recommended final dividend of ₹4 per share, bringing the total payout for the year to ₹6.5 per share (including the interim dividend), signals a commitment to shareholder returns. The company's future trajectory will depend on its ability to translate its AI strategy into tangible revenue growth.

Risks to watch

A key concern is the 1.2% revenue degrowth, reflecting soft market demand. Additionally, an increase in Days Sales Outstanding (DSO) to 62 days (from 54 days in FY25) signals a potential slowdown in collections, which warrants close monitoring.

Peer comparison

While the filing does not provide direct peer comparison data, the reported revenue degrowth in a challenging IT spending environment is a trend seen across some parts of the industry. Birlasoft's margin expansion in this context could be a distinguishing factor.

Context metrics (time-bound)

- Revenue from Operations (FY26): ₹5,310 crore

- Revenue from Operations (FY25): ₹5,375.2 crore

- EBITDA (FY26): ₹866 crore

- EBITDA (FY25): ₹697.4 crore

- PAT (FY26): ₹518.4 crore

- PAT (FY25): ₹516.8 crore

- EBITDA Margin (FY26): 16.3%

- EBITDA Margin (FY25): 13.0%

- Cash and Cash Equivalents: ₹2,637.3 crore

- Days Sales Outstanding (FY26): 62 days

- Days Sales Outstanding (FY25): 54 days

- Final Dividend: ₹4 per share

What to track next

Investors will be watching the company's ability to drive revenue growth, particularly through its AI-led offerings. Monitoring the Days Sales Outstanding (DSO) for improvements in collection efficiency and tracking the success of its 'AI-First' strategy in generating new, scaled client engagements will be crucial.