Birlasoft's FY26 revenue dipped 1.2% to ₹5,310 crore. However, EBITDA jumped 24.2% to ₹866 crore, with margins expanding to 16.3%. PAT remained stable at ₹518.4 crore. The company secured $658 million in new deals.

Birlasoft Reports FY26 Revenue Dip Amidst Strategic Pivot

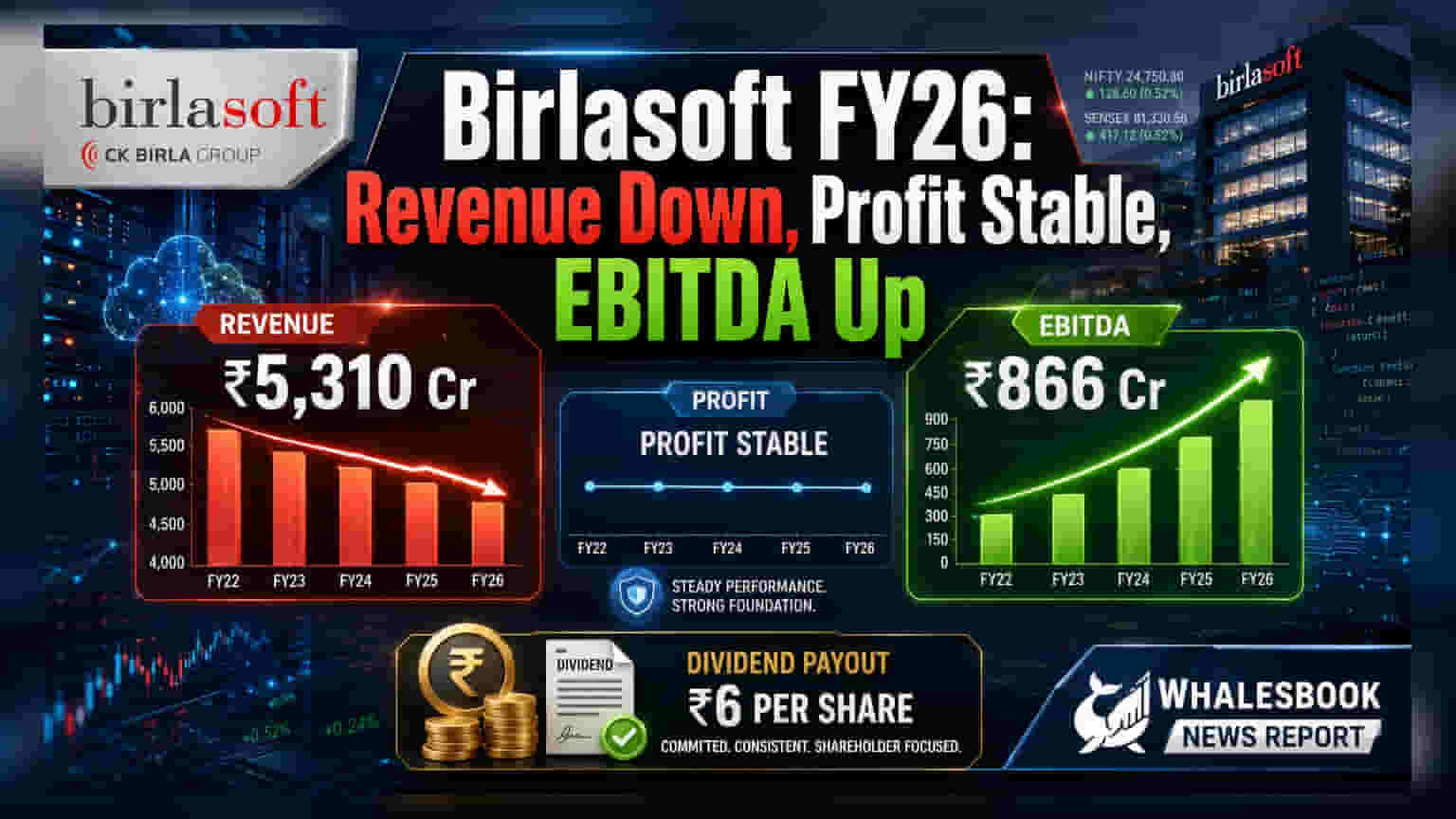

Consolidated Revenue: ₹5,310 crore

Consolidated EBITDA: ₹866 crore

Reader Takeaway: Margin expansion a positive; client concentration and US policies are key watch points.

What just happened

Birlasoft reported its financial results for FY 2026, with consolidated revenue declining by 1.2% to ₹5,310 crore compared to ₹5,375.2 crore in FY 2025. This was attributed to soft demand and exiting unprofitable business. Despite the revenue dip, consolidated EBITDA saw a significant increase of 24.2% to ₹866 crore from ₹697.4 crore, driven by operational efficiencies. Profit After Tax (PAT) remained largely stable at ₹518.4 crore.

Why this matters

The company's focus on profitability over volume is evident in its margin expansion. EBITDA margins improved by 333 basis points to 16.3% from 13.0% in the previous year. This indicates better operational efficiency and cost management. Strong deal wins, particularly in the second half of the fiscal year, totaling $658 million in TCV, suggest potential for future revenue growth. The company is also strategically moving towards a 'Physical AI' approach.

The Board has recommended a final dividend of ₹4 per share, bringing the total for FY 2025-26 to ₹6.5 per share, including the interim dividend.

The backstory

In FY 2025, Birlasoft reported consolidated revenue of ₹5,375.2 crore and EBITDA of ₹697.4 crore. The PAT stood at ₹516.8 crore. The company has been navigating a challenging demand environment and has made strategic choices to exit certain business segments to improve overall profitability.

What changes now

Birlasoft is repositioning itself with a 'Physical AI' strategy, aiming to leverage its strengths in industrial and healthcare sectors. The improved margins and recent deal momentum are expected to support future performance. Investors will be looking for the company to translate these wins into sustained revenue growth and continued margin improvement.

Risks to watch

- Client Concentration: The top 5, 10, and 20 customers account for a significant portion of revenue (42.2%, 55.2%, and 67.0% respectively), posing a concentration risk.

- US Regulatory Policies: Changes in US immigration and visa policies, such as H-1B/L-1, could affect the company's operational flexibility.

- Macroeconomic Headwinds: Geopolitical tensions and economic slowdowns may impact IT spending globally.

Peer comparison

(No peer comparison data was provided in the filing.)

Context metrics (time-bound)

- FY 2026 Consolidated Revenue: ₹5,310 crore (down 1.2% YoY)

- FY 2026 Consolidated EBITDA: ₹866 crore (up 24.2% YoY)

- FY 2026 EBITDA Margin: 16.3% (up from 13.0% in FY 2025)

- FY 2026 Total Contract Value (TCV): $658 million

- Final Dividend Recommended: ₹4 per share

What to track next

Investors will be closely watching Birlasoft's ability to convert its strong TCV wins into revenue growth, sustain its improved margins, and manage its client concentration risks. The progress of its 'Physical AI' strategy will also be key.