Poonawalla Fincorp's Financial Performance in Q4 FY26

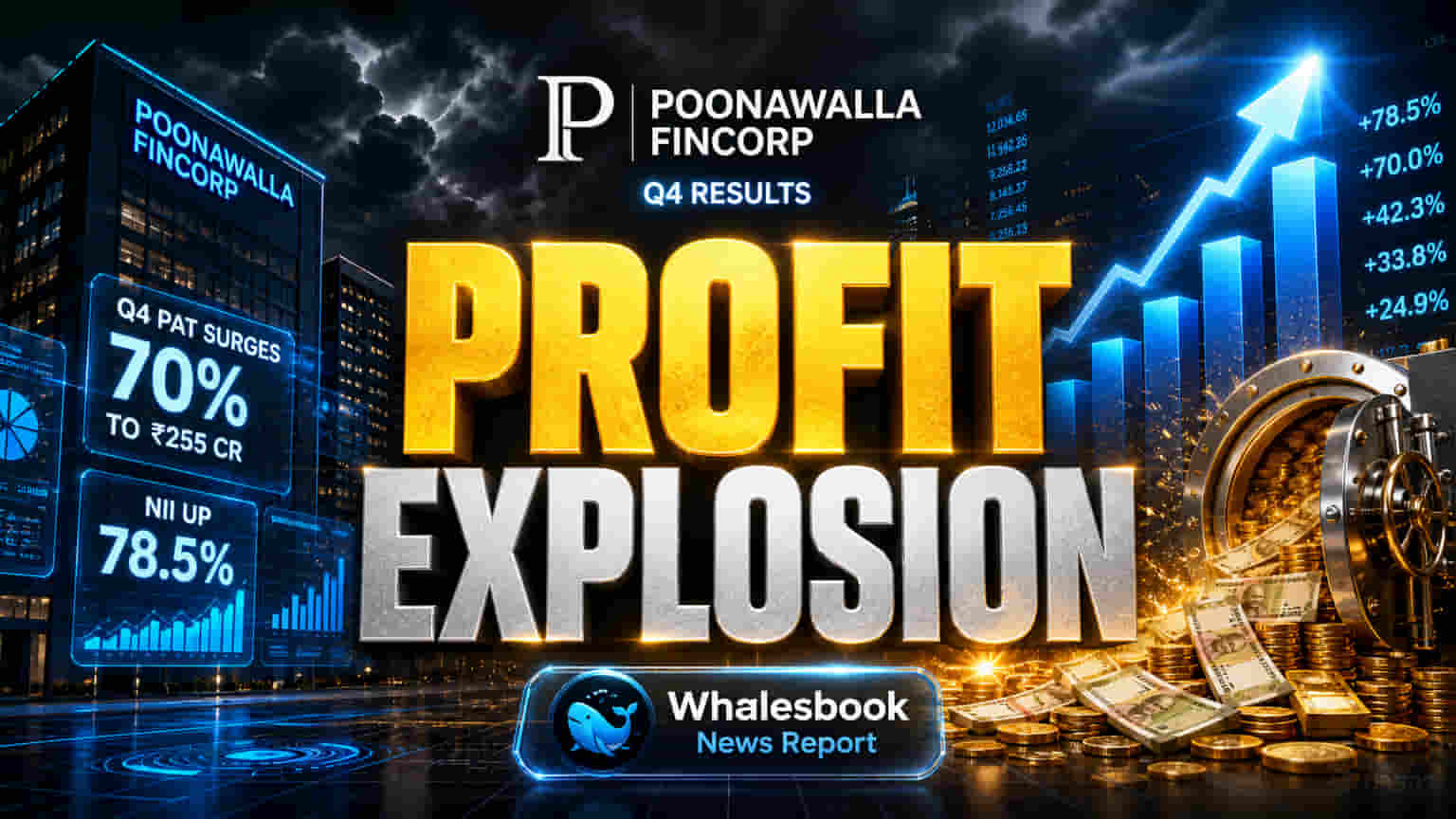

Poonawalla Fincorp announced robust financial results for the quarter ended March 31, 2026. The company reported a Profit After Tax (PAT) of ₹255 crore, a significant 70% increase quarter-on-quarter. Net Interest Income (NII) for the same period surged 78.5% year-on-year to ₹1,276 crore.

Key Financial Highlights

Poonawalla Fincorp Ltd announced strong audited financial results for the quarter and year ended March 31, 2026. The company’s Assets Under Management (AUM) reached ₹60,348 crore.

Profit After Tax (PAT) for the fourth quarter of FY26 saw a substantial 70% quarter-on-quarter jump to ₹255 crore, up from ₹150 crore in Q3 FY26. Net Interest Income (NII) climbed 78.5% year-on-year to ₹1,276 crore.

The company also highlighted healthy performance in key ratios, with Net Interest Margin (NIM) at 9.05% and Gross Non-Performing Assets (GNPA) improving to 1.44% from 1.51% in the previous quarter.

Management Viewpoint

The company’s strong financial performance signals a key growth phase, according to the Managing Director and CEO. Management attributed the NIM expansion to increased yields and improved operational efficiency.

This growth is supported by a strategy focused on expanding yields while managing operating expenses, which are growing slower than assets under management (AUM). This approach positions the business for sustained profitability, with a commitment to strategic investments for long-term earnings.

Company Transformation

Poonawalla Fincorp, formerly Magma Fincorp, has transformed significantly since the Cyrus Poonawalla Group, via Rising Sun Holdings, acquired a controlling stake in early 2021 and provided substantial capital. The group’s strategic direction has guided the company to become a tech-driven, digitally-enabled NBFC focused on consumer and MSME lending.

This strategic shift has been bolstered by consistent capital infusion. This includes a ₹2,500 crore Qualified Institutions Placement (QIP) completed in April 2026, aimed at strengthening its capital base and supporting growth opportunities. The company plans to use data analytics and a digital origination strategy to enhance sales, distribution, and risk management.

Investor Outlook

- Shareholders can anticipate a continued focus on profitable growth, driven by expanding NIMs and controlled credit costs.

- The company’s strategy involves a mix of secured and unsecured products, targeting prime retail and MSME customers.

- Investments in technology and analytics are expected to boost operational efficiencies and enhance the customer experience.

- Strong AUM growth indicates increasing market penetration and demand for the company's lending products.

Potential Risks

While the results are strong, investors should be aware of past regulatory issues. In September 2021, SEBI barred the company's MD and others for alleged insider trading, impounding ₹13.58 crore in wrongful gains, though some bans were later revoked after settlements. More recently, in August 2024, the RBI fined Poonawalla Fincorp ₹10 lakh for prematurely charging interest on loans. The NBFC sector also faces inherent risks from competition and evolving regulatory frameworks.

Competitive Landscape

Poonawalla Fincorp operates in a dynamic NBFC market. Key competitors include Bajaj Finance Ltd., Shriram Finance Ltd., and Cholamandalam Investment and Finance Company Ltd. These companies also focus on retail and MSME lending and face similar market conditions and regulatory environments.

Key Financial Metrics

- Assets Under Management (AUM) stood at ₹60,348 crore as of March 31, 2026, up from ₹55,017 crore as of December 31, 2025.

- Net Interest Income (NII) for Q4 FY26 was ₹1,276 crore, compared to ₹1,080 crore in Q3 FY26.

- Profit After Tax (PAT) for Q4 FY26 was ₹255 crore, against ₹150 crore in Q3 FY26 and ₹62.33 crore in Q4 FY25.

- Gross Non-Performing Assets (GNPA) improved to 1.44% as of March 31, 2026, from 1.51% as of December 31, 2025.

- Capital Adequacy Ratio (CAR) was 16.83% as of March 31, 2026, above the regulatory minimum of 15%.

Looking Ahead

- Sustained AUM growth and its drivers, particularly in digital consumer and MSME segments.

- Management's outlook on future yield expansion and cost optimization strategies.

- Performance of newly launched business segments and their contribution to profitability.

- Any further regulatory developments impacting the NBFC sector.

- The company's ability to maintain asset quality amidst competitive pressures.

- Execution of long-term strategic investments aimed at durable earnings.