PNB Housing Finance Hits GNPA Milestone Below 1%, Retail Book Jumps 16%

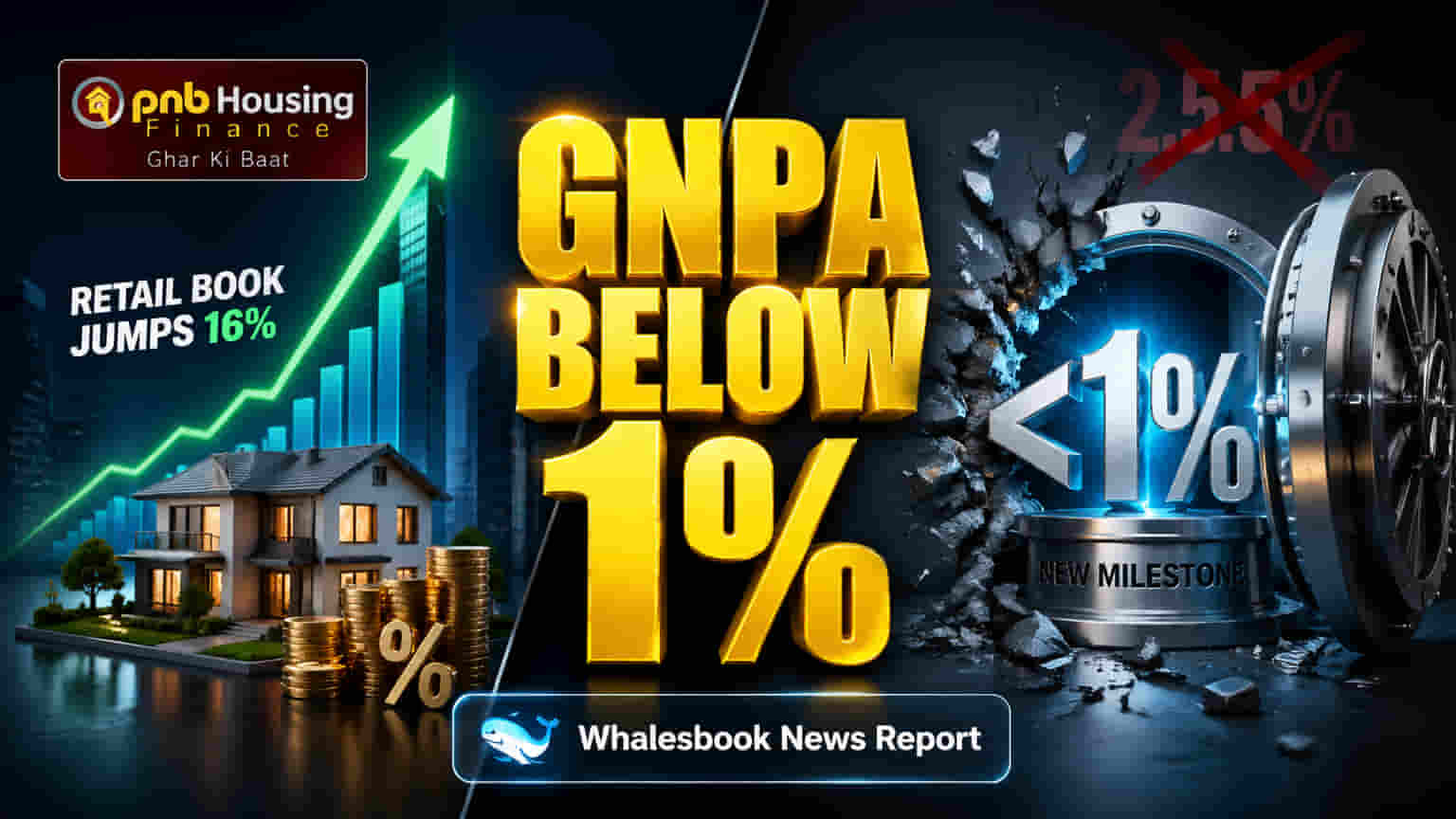

The company achieved a Gross NPA of 0.93% in Q4 FY26, falling below the 1% mark for the first time. Its retail loan book grew 16% year-on-year to INR 86,946 crore, with Q4 disbursements surging 36% year-on-year.

Key Financials and Growth

PNB Housing Finance reported a key milestone in its asset quality, achieving a Gross Non-Performing Asset (GNPA) ratio of 0.93% for Q4 FY26. This marks the first time the ratio has fallen below the 1% threshold. This achievement was supported by a strong 16% year-on-year growth in its retail loan book, which reached INR 86,946 crore.

The company also reported a robust 36% year-on-year surge in Q4 disbursements, totaling INR 9,355 crore. This growth was bolstered by a strategic shift, with affordable and emerging market segments now making up 40% of the retail loan asset, an increase from 37% in the previous year. The digital 'Infinity' app has also improved the onboarding process for its sales team, reducing turnaround times.

PNB Housing Finance has re-entered corporate lending, disbursing INR 335 crore in Q4. This brings the corporate book to INR 401 crore. Management has set a target to cross INR 1 lakh crore in total loan book by FY27, projecting an ROA of 2.4% to 2.5% and Net Interest Margins (NIMs) between 3.55% and 3.65%.

Why This Matters

Achieving sub-1% GNPA demonstrates PNB Housing Finance's success in improving asset quality and managing credit risks, following a period of strategic adjustment. The strong retail loan growth, combined with a shift towards higher-yielding affordable and emerging markets, aims to protect and enhance profitability amid rising competition and evolving interest rate environments.

The resumption of corporate lending, managed cautiously, suggests a diversified growth strategy. The guidance for FY27 outlines a clear growth path, focusing on scaling the loan book while maintaining profitability targets through prudent management of credit costs and funding.

The Backstory

PNB Housing Finance has been undergoing a strategic transformation to strengthen its profitability and market position. In recent years, the company has focused on high-yielding segments like affordable and emerging markets to counter margin pressures often seen in the prime lending segment. This adjustment has involved expanding its retail loan book and opening new branches to serve these customer bases better. The re-entry into corporate lending, after previously stepping away from wholesale lending, signifies a measured approach to diversify revenue streams while managing associated risks.

What Changes Now

- Improved Asset Quality Signal: The sub-1% GNPA milestone suggests a healthier balance sheet, potentially reducing the need for aggressive provisioning and improving investor confidence.

- Strategic Segment Focus: The increasing share of affordable and emerging segments in the retail portfolio indicates a strategic move towards higher-margin products.

- Corporate Lending Re-entry: The resumption of corporate lending, though small, diversifies income sources and could offer avenues for scale if managed effectively.

- Digital Enhancements: The 'Infinity' app adoption is expected to improve operational efficiency and customer service.

- Growth Outlook: The target of crossing INR 1 lakh crore in the loan book by FY27 sets a clear growth trajectory for the company.

- Profitability Drivers: Management's guidance on ROA and NIMs suggests a continued focus on improving earnings efficiency.

Risks to Watch

- External Economic Factors: Volatility in crude oil prices and geopolitical conflicts remain potential risks that could impact economic growth and asset quality.

- Yield Pressures: The prime business segment continues to face yield compression due to competitive banking offers and prevailing interest rate dynamics.

- Operational Cost Increase: Operating expenses grew 13% year-on-year due to branch expansion and implementation of the new Labor Code. Management expects scale benefits to offset this.

Peer Comparison

PNB Housing Finance competes in a dynamic market alongside established players. LIC Housing Finance, the largest HFC, focuses on a broad range of home loans, while Aavas Financiers targets the lower-income and rural segments. Bajaj Housing Finance concentrates on prime home loans and loans against property. PNB Housing's strategic pivot towards affordable and emerging segments aims to carve out a strong niche, while its cautious re-entry into corporate lending competes for a share of a market also served by entities like HDFC Ltd. (now part of HDFC Bank) and others.

As of December 2025, Aavas Financiers reported an AUM of INR 222.04 billion with a GNPA of 1.19%. In contrast, PNB Housing's GNPA of 0.93% signifies a cleaner asset base in the current reported period.

Context Metrics

- The company's ROA is guided to be between 2.4% and 2.5% for FY27.

- NIMs are projected to be in the range of 3.55% to 3.65% for FY27.

- Credit costs are expected to remain negative, between -15 to -20 basis points, driven by recoveries.

What to Track Next

- Sustained GNPA Levels: Monitor if the GNPA ratio remains below 1% in subsequent quarters.

- Corporate Book Growth: Track the expansion and performance of the recently re-initiated corporate loan portfolio.

- New Product Launches: Observe the uptake and yield performance of Micro Housing and Micro LAP products launching in Q1 FY27.

- Opex Management: Evaluate if scale benefits effectively offset the increase in operating expenses due to expansion and labor code impacts.

- Retail Loan Book Growth: Continue to track the momentum in the retail loan book growth, particularly in the affordable and emerging segments.

- Yield Sustainability: Assess if yields in prime segments stabilize or improve amidst competition, and if higher-yield segments drive overall profitability.