Leela Palaces Reports Stellar FY26 with 8.5x Profit Surge

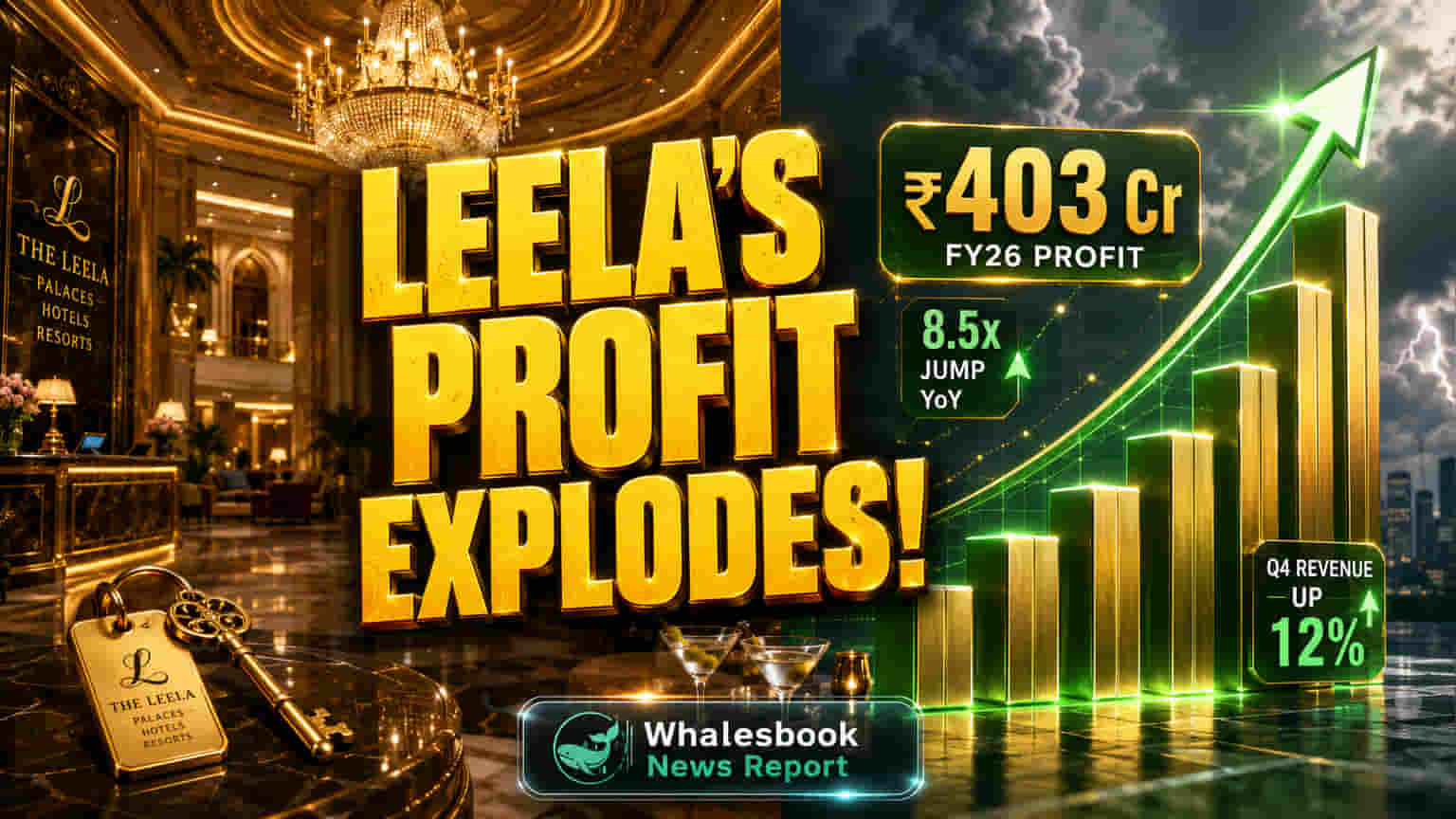

Leela Palaces Hotels & Resorts announced a strong financial performance for fiscal year 2026 (FY26), with profit after tax (PAT) reaching ₹403 crore, an increase of 8.5 times compared to FY25. The company's full-year revenue climbed to ₹1,527 crore.

Key Financials and Expansion

The hospitality group reported a Profit After Tax (PAT) of ₹403 crore for FY26, a substantial rise from ₹48 crore in the previous fiscal year. Full-year revenue reached ₹1,527 crore. Operating EBITDA grew by 19% year-on-year to ₹743 crore in FY26.

In the fourth quarter (Q4 FY26), revenue stood at ₹484 crore, marking a 12% increase year-on-year. PAT for Q4 FY26 was ₹172 crore.

FY26 also saw Leela Palaces achieve its fastest expansion pace, adding 966 rooms, representing a 23% growth in its property portfolio.

The company noted that geopolitical events affected international travel and occupancy in March. Despite this, domestic demand remained strong.

Strategic Growth and Market Position

The robust financial results and rapid expansion signal a successful growth phase for Leela Palaces. The company's strategic push for expansion aims to capture greater market share and diversify its offerings within the luxury hospitality segment.

Company History and Future Plans

Leela Palaces Hotels & Resorts, acquired by Brookfield Asset Management in 2019, has been actively expanding its presence. Recent developments include the March 2026 acquisition of an ultra-luxury resort in Coorg for ₹560 crore, its first venture into wellness-focused hospitality.

In October 2025, Leela announced its first international project, a resort in Dubai, with an expected closing in Q3 2026. The company has outlined ambitious plans to grow its portfolio to over 5,000 rooms across more than 23 properties within the next three years, targeting new Indian destinations.

Growth Initiatives and Strategic Focus

The company's expanded portfolio across various regions is intended to diversify revenue streams. Strategic acquisitions and new developments are positioning Leela for continued long-term growth. A focus on wellness and nature-led hospitality is designed to attract new customer segments.

Potential Challenges

Geopolitical events and broader external volatility continue to present challenges, as indicated by the dip in March occupancy. The Dubai asset is currently under evaluation, though write-offs are considered unlikely due to conservative underwriting. The company's ownership transition following the 2019 acquisition faced legal challenges related to related-party transactions, which have since been resolved.

Competitive Landscape

Leela Palaces operates in the competitive luxury hospitality market, facing competition from established players such as Indian Hotels Company, ITC Hotels, EIH Ltd, and Lemon Tree Hotels.