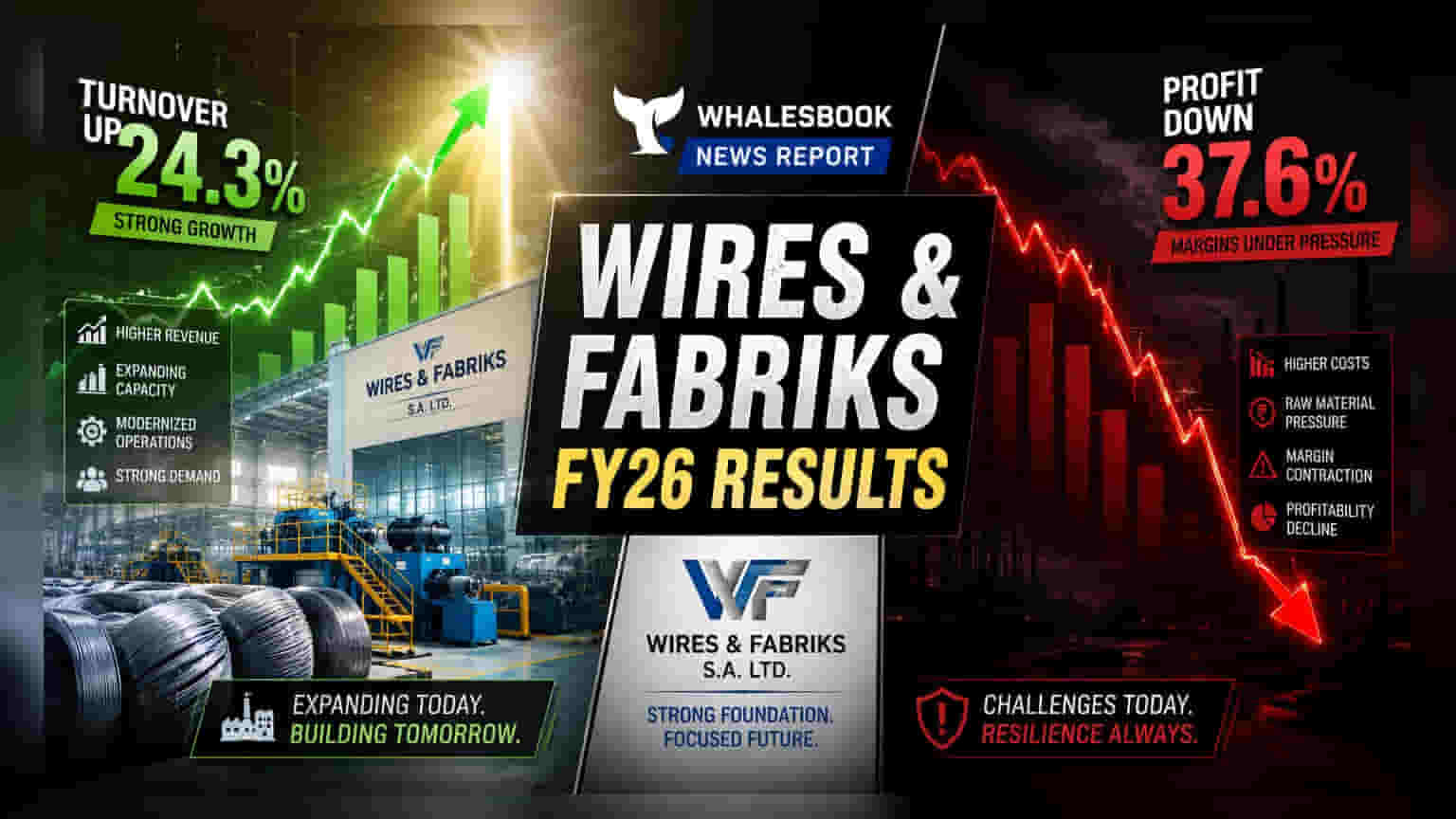

Wires & Fabriks SA Ltd reported increased turnover for FY 2025-26, but net profit declined to ₹0.26 crore due to higher interest and depreciation from modernization. Management expects profit to improve. A ₹0.10 dividend was recommended.

Wires & Fabriks SA Ltd FY2025-26 Results Show Turnover Growth Amid Profit Pressure

Revenue for FY 2025-26: ₹115.45 crore (₹11544.97 lakh)

Profit After Tax for FY 2025-26: ₹0.26 crore (₹26.43 lakh)

Reader Takeaway: Turnover increased, but higher expansion costs pressured net profit; future margin recovery is key.

What just happened

Wires & Fabriks SA Ltd has reported its financial results for the fiscal year 2025-26. The company's turnover saw an increase to ₹115.45 crore from ₹109.02 crore in the previous year. However, Profit After Tax (PAT) saw a significant decline, falling to ₹0.26 crore from ₹1.50 crore in FY 2024-25. This was attributed by management to increased interest and depreciation expenses linked to a recently completed expansion and modernization project.

Why this matters

The decline in net profit, despite revenue growth, highlights the immediate impact of capital expenditure on the company's bottom line. Shareholders will be watching how the company manages these increased costs and leverages its expanded capacity to drive future profitability. The recommended dividend of ₹0.10 per share indicates a payout despite the profit squeeze.

The backstory

The company has recently undertaken an expansion and modernization project, which has led to higher operational costs in the short term. This is a common scenario for companies investing in upgrading facilities for future competitiveness.

What changes now

Investors will monitor the company's ability to absorb the new costs and improve operational efficiency. The management expects profit levels to recover as the benefits of the modernization project are realized. Key management positions have been reaffirmed for five-year tenures, ensuring leadership continuity.

Risks to watch

The primary risk is the company's ability to achieve sufficient capacity utilization and revenue growth to cover the increased interest and depreciation costs. The current debt-to-equity ratio stands at 2.08, indicating significant leverage that needs careful management.

Peer comparison

(No direct peer comparison data available in the filing).

Context metrics (time-bound)

- Turnover (FY 2025-26): ₹115.45 crore

- PAT (FY 2025-26): ₹0.26 crore

- Dividend (FY 2025-26): ₹0.10 per share

- Debt-to-equity ratio: 2.08

What to track next

Investors should track the company's quarterly results to observe the trend in profitability and capacity utilization. The management's ability to translate increased turnover into improved net profit margins will be crucial. The upcoming 69th Annual General Meeting on July 29, 2026, will also be an event to note.