UNO Minda reported strong financial performance for FY26 with revenue at ₹19,658 crore and PAT up 27% to ₹1,197 crore. The company also announced a dividend and plans to raise up to ₹2,500 crore for growth, including new EV component plants.

UNO Minda Reports Robust FY26 Growth, Plans Capital Infusion

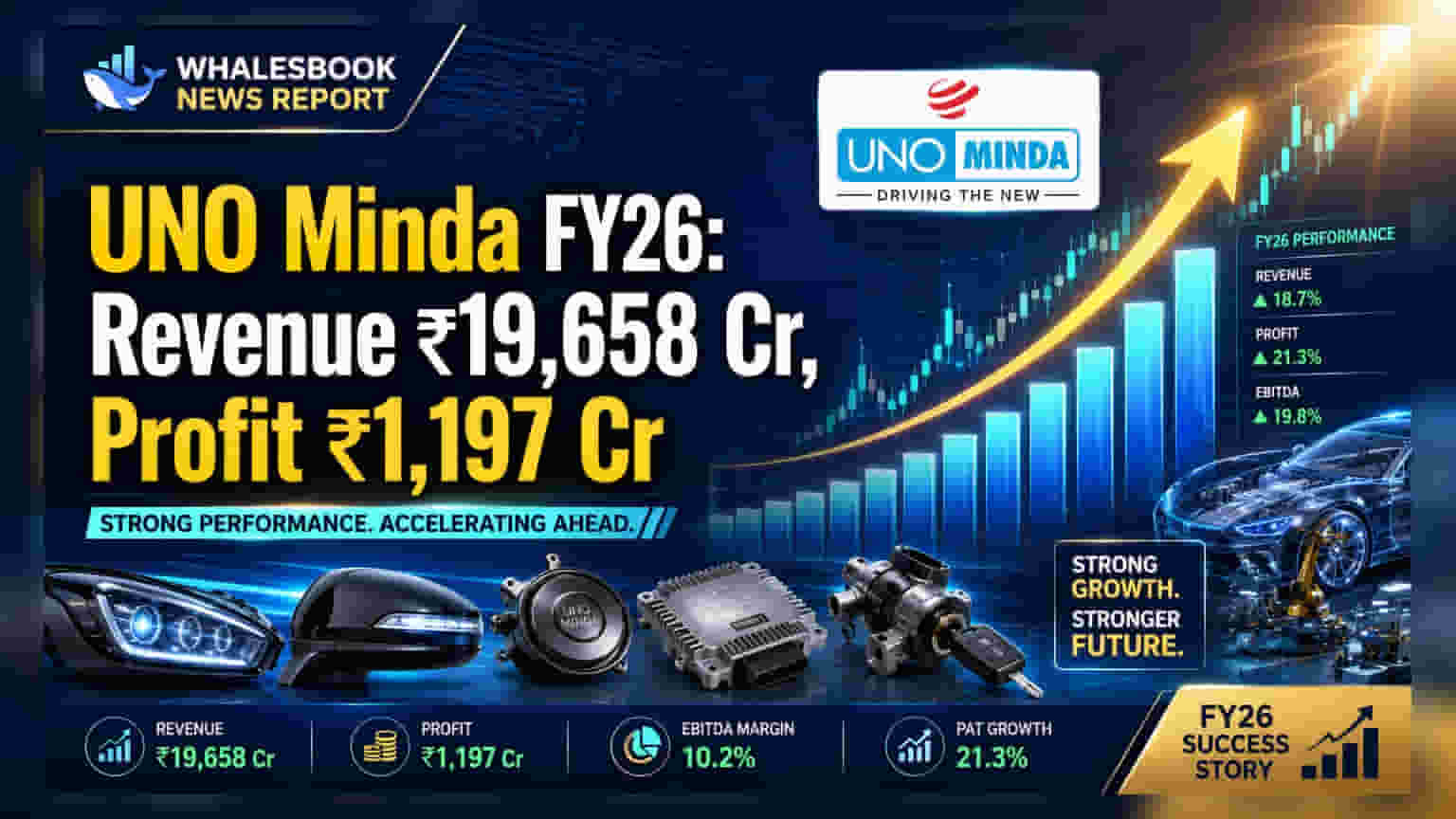

Consolidated Revenue: ₹19,658 crore

PAT (Attributable to shareholders): ₹1,197 crore

Reader Takeaway: Strong revenue and profit growth driven by strategic investments, but commodity price volatility and customer concentration remain watch points.

What just happened

UNO Minda Ltd announced its financial results for FY 2025-26, showcasing significant year-on-year growth. Consolidated revenue reached ₹19,658 crore, a 17% increase from FY 2024-25. Earnings Before Interest, Taxes, Depreciation, and Amortisation (EBITDA) rose by 20% to ₹2,251 crore. Profit After Tax (PAT) attributable to shareholders saw a substantial 27% jump, reaching ₹1,197 crore compared to ₹943 crore in the previous fiscal year. The company's EBITDA margin improved to 11.5% from 11.2%.

Why this matters

These results demonstrate UNO Minda's strong execution capabilities and successful expansion, particularly in the growing automotive sector. The significant PAT growth indicates improved profitability and operational efficiency. The planned capital raise signals ambitious expansion plans, including investments in Electric Vehicle (EV) components, which aligns with industry shifts.

The backstory

UNO Minda has been consistently expanding its product portfolio and manufacturing capabilities. Recent strategic moves include securing new orders for Infotainment (IVI) systems and 2W lamps. The company is also actively investing in EV-related infrastructure, such as a new casting plant and a second passenger vehicle EV powertrain plant.

What changes now

UNO Minda will seek shareholder approval to raise up to ₹2,500 crore. This capital will likely fund its expansion projects, including the new EV-related plants. The company has recommended a final dividend of ₹1.75 per equity share, adding to the interim dividend already paid.

Risks to watch

The company highlighted two key watch points: commodity price volatility, which could impact margins, and customer concentration, as it relies on a limited number of Original Equipment Manufacturers (OEMs). Diversifying its customer base and managing commodity costs will be crucial.

Peer comparison

While specific peer results are not detailed in the filing, UNO Minda's performance in revenue and profit growth appears robust within the auto components sector, which is experiencing overall growth driven by increased vehicle production and a shift towards EVs.

Context metrics (time-bound)

- Consolidated Revenue (FY26): ₹19,658 crore (vs ₹16,775 crore in FY25)

- EBITDA (FY26): ₹2,251 crore (vs ₹1,874 crore in FY25)

- PAT (FY26): ₹1,197 crore (vs ₹943 crore in FY25)

- Final Dividend: ₹1.75 per share

- Capital Raising Plan: Up to ₹2,500 crore

- New EV Casting Plant Investment: ₹210 crore

- New EV Powertrain Plant Investment: ₹550 crore

What to track next

Investors should monitor the progress of the capital raise, the deployment of funds into new projects, particularly the EV-related investments, and management's strategies to mitigate commodity risks and customer concentration.