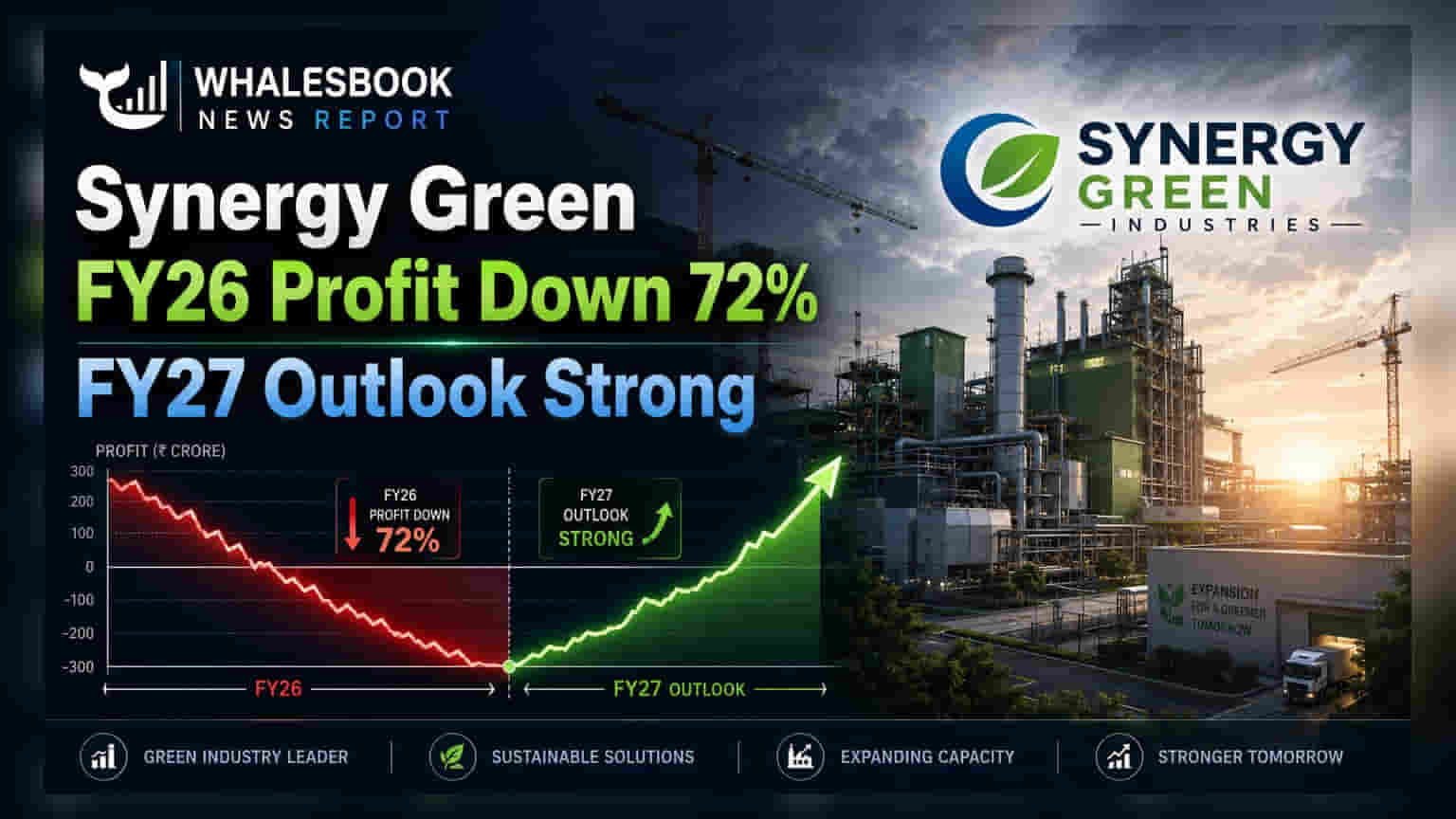

Synergy Green Industries reported a 72% drop in FY26 net profit to ₹4.66 crore, impacted by expansion costs. Revenue grew 3.49%. The company expects strong growth and margin improvement in FY27.

Synergy Green Industries FY26 Results: Profit Hit by Expansion, FY27 Outlook Positive

Synergy Green Industries reported standalone Profit After Tax (PAT) of ₹4.66 crore for FY 2025-26, a significant 72% decrease from ₹16.89 crore in the previous fiscal year. Total income saw a modest increase of 3.49% to ₹376.37 crore.

Reader Takeaway: Capacity expansion successful but margins pressured; FY27 outlook strong.

What just happened

Synergy Green Industries posted a substantial drop in net profit for the fiscal year ending March 2026, primarily due to higher operating costs and expansion-related overheads. Total income grew marginally by 3.49% to ₹376.37 crore.

Why this matters

The significant profit decline, coupled with a muted revenue increase, highlights the short-term financial impact of the company's aggressive capacity expansion. However, management's positive outlook for FY27 suggests these investments are expected to yield future benefits.

The backstory

The fiscal year 2025-26 was focused on a ₹217 crore capital expenditure program. This included expanding foundry capacity to 45,000 TPA, commissioning a new 20,000 TPA machining and coating facility, and increasing captive solar power to 10 MW. This expansion also led to increased outsourcing, manpower, and overhead costs.

What changes now

With the capex cycle complete, the company anticipates improved operational leverage and margin expansion in FY 2026-27. Management projects healthy double-digit revenue growth and an order book exceeding ₹500 crore, with EBITDA margins expected to improve by over 300 basis points.

Risks to watch

A key concern is the high concentration of over 80% of revenue from the wind sector. Margin pressure from increased operational costs needs careful monitoring as new capacities are utilized.

Peer comparison

(No peer comparison data available in the filing).

Context metrics (time-bound)

- Total Income FY25-26: ₹376.37 crore (up 3.49% from ₹363.68 crore in FY24-25).

- PAT FY25-26: ₹4.66 crore (down from ₹16.89 crore in FY24-25).

- Foundry Capacity: Increased to 45,000 TPA from 30,000 TPA.

- New Machining & Coating Capacity: Commissioned 20,000 TPA.

- Captive Solar Power: Increased to 10 MW from 2 MW.

- FY26-27 Outlook: Revenue growth expected to be double-digit, order book over ₹500 crore, EBITDA margin expansion over 300 bps.

What to track next

Investors should monitor the ramp-up of new facilities and the realization of projected revenue growth and margin expansion in FY 2026-27. Diversification beyond the wind sector will also be a key factor.