Seshasayee Paper and Boards Ltd Financial Update

The Latest Financial Results

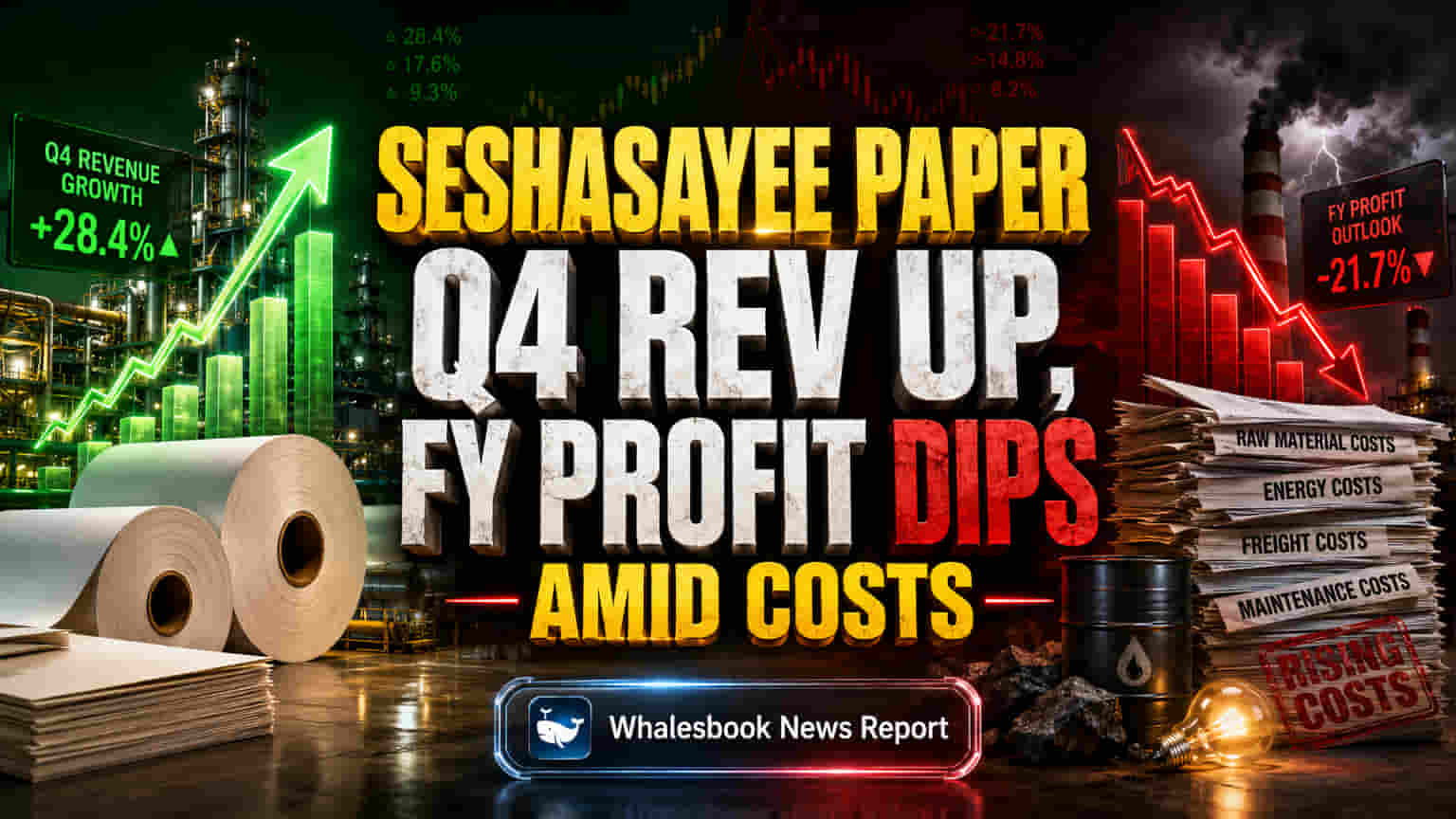

Seshasayee Paper and Boards Ltd (SPB) announced its financial results for the quarter and year ended March 31, 2026, presenting a mixed financial picture. The company achieved a strong 15.93% year-on-year revenue growth in the final quarter (Q4 FY26), reaching ₹603.47 crore. This rebound in sales was partially impacted by rising expenses, which increased by 17.75% YoY during the quarter, outpacing revenue growth and contributing to a slight dip in quarterly net profit.

For the full fiscal year FY26, consolidated revenue declined 3.50% to ₹1,759.20 crore. Net profit saw a more significant drop of 24.40%, closing at ₹82.53 crore compared to ₹109.17 crore in FY25. A notable positive from the filing is the company's successful elimination of current borrowings, reducing them to ₹0.00 as of March 31, 2026. Management has recommended a dividend of ₹2.00 per share.

Strategic Importance of Recent Moves

The company's performance signals a period of transition. While the robust Q4 revenue offers a glimpse of renewed sales momentum, the annual profit decline highlights persistent margin pressures and the ongoing need for stringent cost management. The strategic acquisition of Servalakshmi Paper Limited's assets through an NCLT auction is a significant development. This move is aimed at expanding production capacity and enhancing the company's operational footprint.

Company Background and Acquisition

Seshasayee Paper and Boards Ltd is an Indian paper manufacturer specializing in printing and writing paper, and packaging boards, with mills located in Erode, Tamil Nadu. The company has focused on strengthening its balance sheet, notably by eliminating current borrowings. The recent acquisition of assets from Servalakshmi Paper Limited via an NCLT e-auction is a key strategy. This initiative is designed to boost production capacity and integrate operations, aiming to revive a previously distressed asset and broaden SPB's market reach.

What's Next for the Company

- Integration of the Servalakshmi Paper assets is expected to increase production capacity and potentially market share.

- A strengthened balance sheet is a result of eliminating all current borrowings.

- The company will likely focus on operationalizing the acquired assets and driving cost efficiencies.

- Shareholders are slated to receive a recommended dividend payout of ₹2.00 per share.

Key Risks and Challenges

- The primary risk involves the successful integration and revival of the acquired Servalakshmi Paper operations.

- Sustaining the positive Q4 revenue momentum throughout FY27 amid potential global economic uncertainties.

- Effectively managing rising input costs and operational expenses to prevent further margin erosion.

Industry Peers

- JK Paper Ltd.: A major player with a diversified product portfolio and recent capacity expansions.

- West Coast Paper Mills Ltd.: A strong competitor in the printing and writing paper segment, focused on operational efficiency.

- Andhra Paper Ltd.: Another significant manufacturer in the Indian paper sector, navigating similar industry dynamics.

Key Financial Metrics

- Consolidated Revenue declined by 3.50% from FY25 to FY26, moving from ₹1,822.98 crore to ₹1,759.20 crore.

- Consolidated Net Profit decreased by 24.40% from FY25 to FY26, from ₹109.17 crore to ₹82.53 crore.

- Current borrowings were reduced to ₹0.00 as of March 31, 2026, down from ₹81.86 crore in the previous year (Standalone basis).

Investor Watchlist

- Updates on the operational commencement and performance of the newly acquired Servalakshmi Paper assets.

- Management's commentary on cost control measures and margin improvement strategies during the next earnings call.

- Early indicators from Q1 FY27 results to assess the sustainability of the Q4 revenue growth.

- The formal announcement and payout timeline for the recommended ₹2.00 per share dividend.

- Company plans for leveraging the newly acquired capacity for future revenue streams.