L&T Posts Record ₹7.4 Lakh Crore Order Book, FY26 Revenue Up 12.2%

Consolidated Annual Total Income reached ₹2,91,635.04 crore. Net Profit Attributable to Owners rose to ₹18,963.88 crore.

What happened in the latest results

Larsen & Toubro (L&T) announced its Q4 and full-year FY26 financial results, detailing strong operational performance alongside significant one-off charges impacting its standalone results.

For the quarter ended March 31, 2026, consolidated total income stood at ₹84,340.75 crore, an 11.67% increase year-on-year. Quarterly consolidated profit attributable to owners was ₹5,325.60 crore.

On an annual basis, consolidated total income grew 12.23% to ₹2,91,635.04 crore. Consolidated net profit for owners rose 7.30% to ₹18,963.88 crore, with basic EPS at ₹116.93.

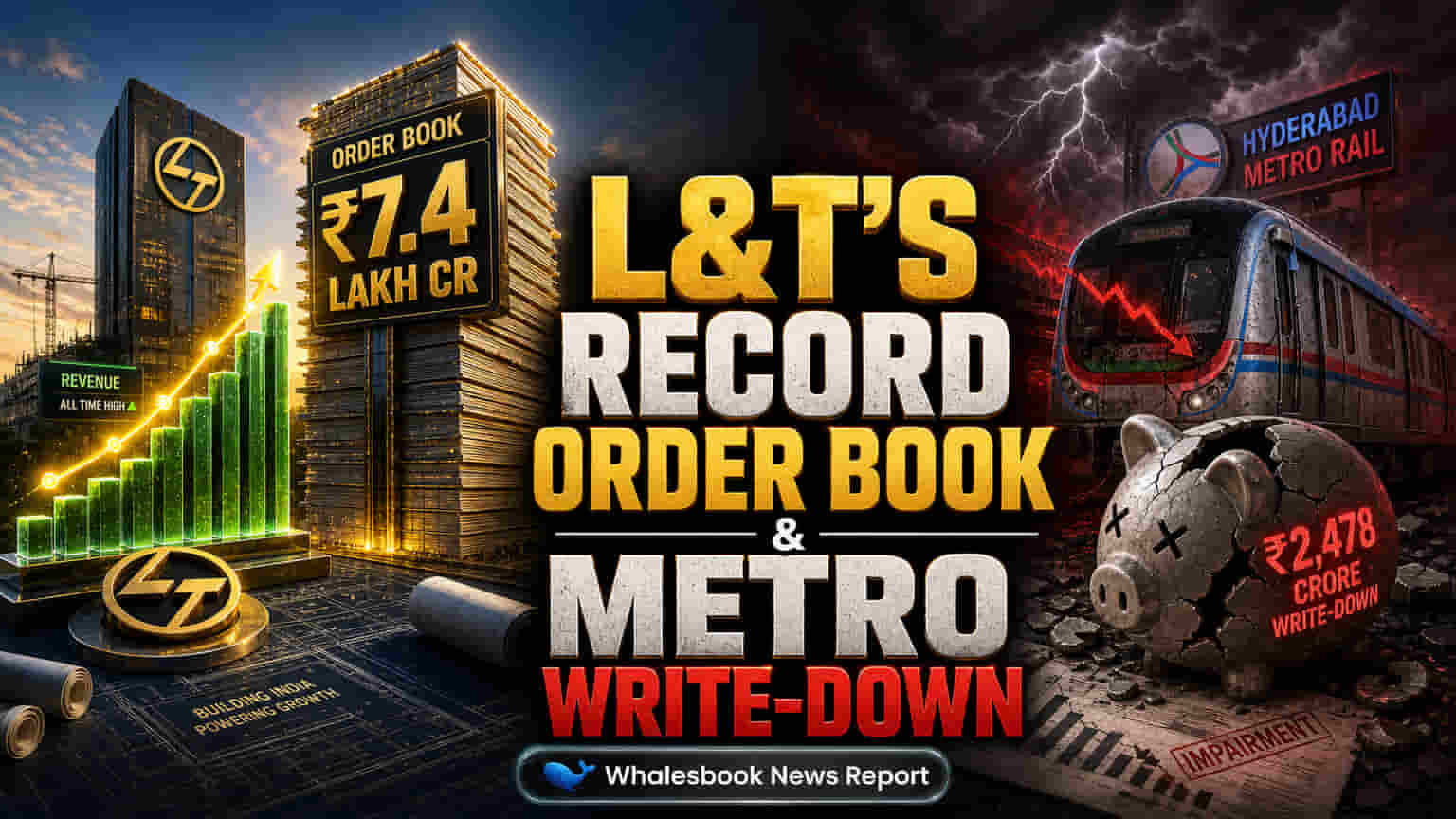

The company achieved an all-time high consolidated order book of ₹7,40,327 crore as of March 31, 2026, providing substantial revenue visibility for upcoming periods.

However, standalone results were heavily affected. Total income was ₹1,61,038.62 crore, but profit fell sharply to ₹6,287.13 crore due to significant exceptional items.

These exceptional items included a ₹6,013 crore write-down of L&T's investment in the Hyderabad Metro Rail project (LTMRHL). Additionally, a one-time provision of ₹1,155 crore (net of tax) was made for employee benefits stemming from new labour codes.

Why it matters

L&T's core EPC (Engineering, Procurement, Construction) and infrastructure businesses demonstrate strong execution and growth, as shown by the record order book and steady consolidated revenue increase. This highlights the company's strong market position in key sectors driving national growth.

However, the substantial standalone write-down on the Hyderabad Metro project underscores financial challenges tied to certain legacy development assets. The employee benefit provision, though a one-time charge, also suppressed reported profit growth for the year.

Company background

Larsen & Toubro is a leading Indian engineering and construction conglomerate with extensive experience in infrastructure development, heavy engineering, and manufacturing. The Hyderabad Metro Rail project has been a financially complex venture for L&T, involving significant investment and facing challenges that have led to financial provisioning previously. The company's consistent focus on securing large orders is a strategic priority for sustaining growth in its core EPC businesses.

Key changes for investors

- Shareholders can anticipate a proposed final dividend of ₹38 per share, an increase from ₹34 last year, signaling management confidence.

- The reported standalone profit figures for FY26 are notably lower than they would have been without the Hyderabad Metro write-down and employee provision.

- The large order book offers a strong base for revenue growth in FY27 and beyond, despite the one-off impacts.

- Investors gain clearer insight into the financial health of L&T's core EPC operations, distinct from its legacy asset challenges.

Potential risks

- The ongoing financial performance and potential resolution of the Hyderabad Metro Rail investment remain a key concern for standalone profitability.

- Execution risks associated with the record ₹7.4 lakh crore order book, particularly in managing large-scale, complex projects.

- Potential for unforeseen cost increases or project delivery delays, which could impact margins.

- Regulatory or policy changes affecting the infrastructure sector or specific project economics.

Peer comparison

L&T operates in a competitive sector with peers such as PNC Infratech, KNR Constructions, and Kalpataru Projects International, all active in India's infrastructure and EPC space. While these companies also focus on order book growth and project execution, L&T's scale, diversification across heavy industries (including defence, hydrocarbon, and IT), and its conglomerate status set it apart. The ₹7.4 lakh crore order book is significantly larger than those typically held by its pure-play infrastructure peers, reflecting its broader market dominance.

Financial context

- Consolidated Total Equity grew from ₹1,15,403.68 crore in FY25 to ₹1,28,530.46 crore in FY26.

What to watch next

- Management commentary during the post-results conference call regarding the Hyderabad Metro situation and future plans for the asset.

- Details on the composition of the ₹7.4 lakh crore order book and segment-wise inflow trends.

- Guidance for FY27 revenue growth, profit margins, and capital expenditure plans.

- Progress on divesting or resolving non-core/legacy assets weighing on standalone profitability.

- Performance updates from L&T's IT and technology services segments, which often provide stable earnings.