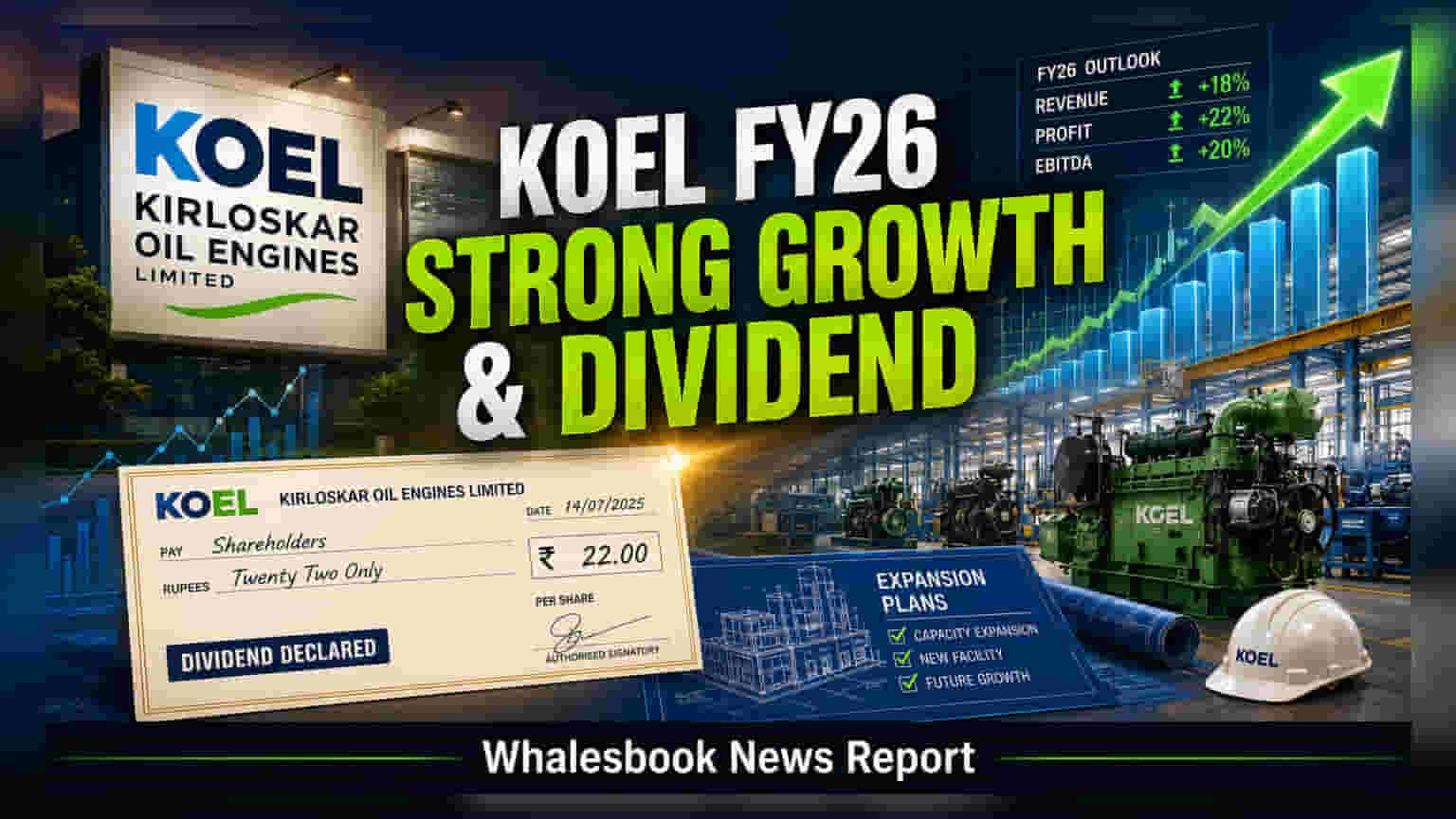

Kirloskar Oil Engines reported robust standalone performance for FY 2025-26 with net sales of ₹5,604 crore and PAT of ₹441 crore. The company announced a 350% dividend and a strategic business realignment to focus on its core B2B operations.

Kirloskar Oil Engines Ltd. Fiscal Year 2025-26 Performance

Net Sales (FY 2025-26): ₹5,604 crore

Profit After Tax (FY 2025-26): ₹441 crore

Reader Takeaway: Strong standalone growth and a significant B2B focus enhancement.

What just happened

Kirloskar Oil Engines Ltd. (KOEL) has reported strong financial results for the fiscal year 2025-26. The company achieved net sales of ₹5,604 crore and a Profit After Tax (PAT) of ₹441 crore. EBITDA stood at ₹737 crore, with a healthy margin of 13.06%. The Board has proposed a total dividend of 350% (₹7.00 per share).

Why this matters

These results demonstrate robust operational performance and profitability. The strategic transfer of the Business to Customer (B2C) segment to its subsidiary, KOEL Fluid Dynamics Private Limited, effective October 11, 2025, signals a clear focus on strengthening the core Business to Business (B2B) engineering and power generation operations. This aligns with the company's long-term revenue goals.

The backstory

KOEL has consistently focused on its core engineering and power solutions. The recent strategic realignment is a step to further sharpen management's attention on high-margin B2B segments, aiming for enhanced efficiency and market leadership. This follows a period of stable financial performance and strategic capacity planning.

What changes now

The transfer of the B2C segment is expected to streamline operations and allow for more targeted investment and management bandwidth towards the B2B business. Significant capital expenditure plans, including ₹700 crore for phase 1 engine capacity expansion at Kagal by April 2027 and ₹1,400 crore for phase 2, will support future growth.

Risks to watch

While performance is strong, KOEL faces risks from supply chain volatility in specialized components, impacting delivery schedules. Geopolitical uncertainties and trade volatility in export markets, along with potential carbon taxes, could also challenge future revenue and margin growth.

Peer comparison

KOEL operates in the engine and power generation equipment sector, competing with domestic and international players. Its focus on specialized engines and large-scale projects, like the NPCIL order, differentiates its market position.

Context metrics (time-bound)

For FY 2025-26, Net Sales were ₹5,604 crore compared to ₹5,073 crore in FY 2024-25. Profit Before Tax increased to ₹594 crore from ₹580 crore in the previous year. Earnings Per Share remained steady at ₹30.

What to track next

Investors will be keen to monitor the execution of the ₹700 crore Kagal expansion and the ₹1,400 crore phase 2 investment. Progress on the ₹798 crore NPCIL genset order, with revenue recognition starting FY 2026-27, will also be crucial for future performance.