Jindal Stainless Reports Strong FY26 Results, Eyes 4.2 MTPA Capacity Expansion

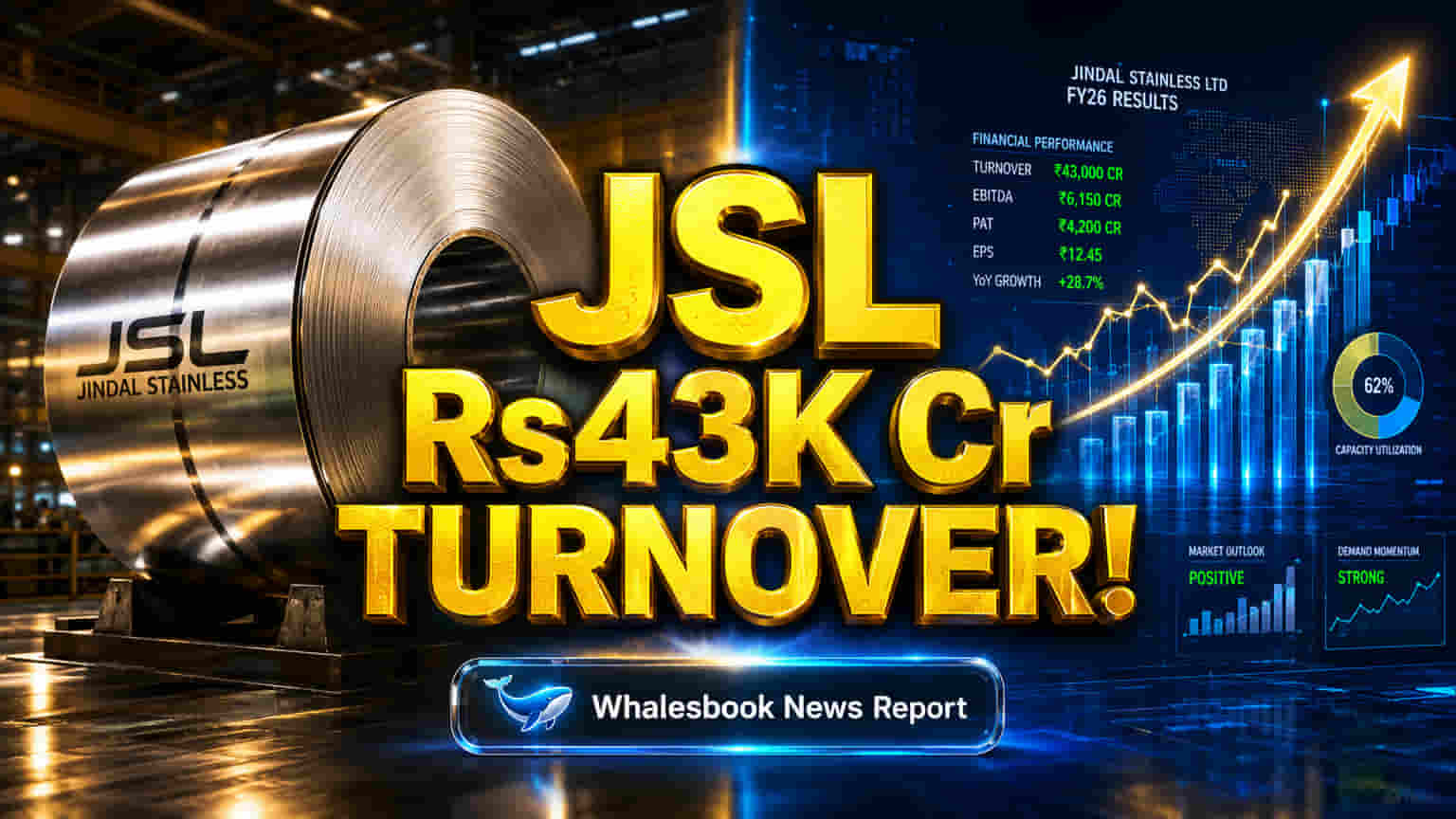

Jindal Stainless Limited announced its FY26 results, reporting an annual turnover of ₹42,955 crore. The company also achieved a strong Profit After Tax (PAT) growth, with a Compound Annual Growth Rate (CAGR) of 28% from FY21 to FY26.

Key Financials and Expansion Plans

India's leading stainless steel maker, Jindal Stainless, reported its FY26 performance, highlighting the ₹42,955 crore turnover. This follows a period of significant financial growth, marked by the 28% PAT CAGR between FY21 and FY26. The company is setting an ambitious target to increase its annual melt capacity to 4.2 million tonnes by FY27. This expansion is intended to meet growing demand and strengthen its market standing both in India and internationally.

Strategic Growth and Market Position

This significant capacity expansion underlines Jindal Stainless's commitment to future growth and its strategy to keep its leading position in the competitive stainless steel market. Reaching the 4.2 MTPA goal by FY27 will better equip the company to meet India's increasing industrial and consumer need for stainless steel. The company is also prioritizing balance sheet strength, aiming to optimize leverage ratios with a target of Net Debt to EBITDA below 1.5x. This dual focus on expansion and financial management shows a careful approach to growth.

Expansion and Supply Chain Focus

Jindal Stainless has consistently pursued growth, particularly through its strategic plans for capacity expansion to around 4.2 MTPA melt shop capacity by FY27. A key part of this strategy involves securing raw material supply chains. This is shown through investments, such as taking a stake in an NPI facility and setting up an SMS facility in Indonesia. Parallel to these growth projects, the company has focused on strengthening its balance sheet and managing financial leverage, aiming to keep Net Debt to EBITDA below 1.5x.

What Investors Can Expect

- Shareholders can expect increased production capabilities, supporting efforts to capture more market share.

- Improvements in operational efficiency from integrated processes may lead to better profit margins.

- Strategic capital allocation, with growth projects targeting an IRR of approximately 15%, indicates a focus on creating shareholder value.

- Optimized leverage ratios are projected to enhance the company's financial stability.

- Recent acquisitions and joint ventures are expected to strengthen raw material supply and broaden the company's geographical presence.

Potential Risks

The company's growth projections rely on forward-looking statements. These are subject to various known and unknown risks and uncertainties. Actual results could differ significantly from these projections.

Competitive Landscape

Jindal Stainless competes in the Indian steel industry with major players such as Tata Steel and Jindal Steel & Power (JSPL). While Tata Steel and JSPL have larger overall steel production capacities, Jindal Stainless is the leader specifically in the stainless steel segment within India.

Key Performance Metrics

- Consolidated Turnover: ₹42,955 crore for FY26.

- Consolidated Profit After Tax (PAT) CAGR: 28% (FY21-FY26).

- Consolidated Sales Volume CAGR: 14% (FY21-FY26).

- Consolidated Revenue CAGR: 17% (FY21-FY26).

- Consolidated EBITDA CAGR: 18% (FY21-FY26).

What to Watch

- Progress and successful commissioning of the 4.2 MTPA capacity expansion by FY27.

- The company's performance against financial targets, such as revenue, EBITDA, and leverage ratios.

- Integration and benefits from recent strategic acquisitions and joint ventures.

- The company's debt management and progress toward its Net Debt/EBITDA ratio target.

- Any future announcements regarding organic or inorganic growth opportunities.