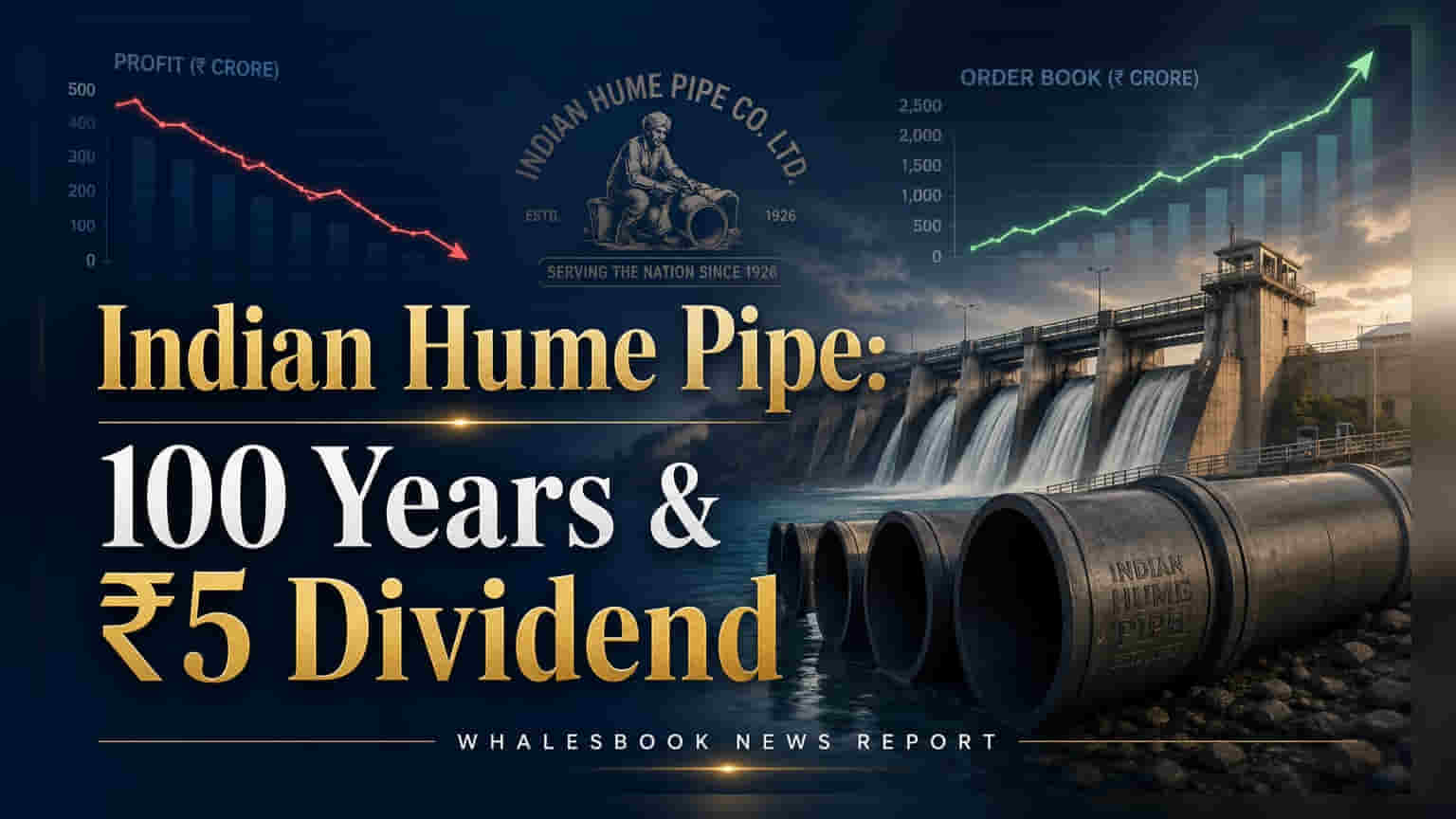

Indian Hume Pipe Company turns 100 with a robust ₹4,118.97 crore order book. The company recommended a ₹5 per share dividend, including a special centennial payout. Net profit saw a significant drop due to lower exceptional gains, not operational issues.

Indian Hume Pipe Company Marks Centennial Milestone

Indian Hume Pipe Company is celebrating its 100th year of incorporation, with revenues of ₹1,305.57 crore and a net profit of ₹141.11 crore for FY 2025-26. The company also announced a strong order book of ₹4,118.97 crore as of May 6, 2026.

Reader Takeaway: Robust order book and dividend payout offset by reduced exceptional gains impacting net profit.

What just happened

The Indian Hume Pipe Company has reported its financial results for FY 2025-26, coinciding with its 100th year of incorporation. The company achieved revenues of ₹1,305.57 crore and a net profit after tax of ₹141.11 crore. A significant order book of ₹4,118.97 crore provides a strong foundation for future growth.

The Board has recommended a dividend of ₹5 per equity share, comprising a normal dividend of ₹2 and a special centennial dividend of ₹3. This move aims to reward shareholders and celebrate the company's long history.

Why this matters

The company's transition to a full-spectrum EPC contractor is driving its long-term growth. The strong order book indicates sustained demand for its infrastructure projects, particularly in water supply management. Monetizing land banks provides additional liquidity and non-core revenue streams.

The recommended dividend, including a special payout, signifies confidence in the company's financial health and a gesture to shareholders commemorating the centennial.

The backstory

Indian Hume Pipe Company, incorporated in 1926, has evolved from a manufacturer to an EPC contractor. This strategic shift has deepened its involvement in end-to-end water supply projects. The company has also been actively leveraging its historical land assets for development projects, creating a dual revenue stream.

What changes now

Investors can look forward to continued execution on its substantial order book. The EPC focus is expected to drive deeper engagement in infrastructure projects. Monetization of land assets is likely to continue supporting the company's liquidity.

Risks to watch

Margin pressure remains a concern due to volatile raw material costs for steel, HDPE, and cement. The company's profitability was impacted by lower exceptional gains in FY 2025-26 compared to the previous year. Geopolitical risks, such as conflicts in West Asia, could lead to uncertainty in energy markets and increased logistical costs.

Peer comparison

While specific peer data is not provided in the filing, Indian Hume Pipe operates in the infrastructure and construction sector, competing with other EPC contractors focused on water infrastructure and allied projects.

Context metrics (time-bound)

- Revenue (FY 2025-26): ₹1,305.57 crore

- Net Profit (FY 2025-26): ₹141.11 crore

- Order Book (as of May 6, 2026): ₹4,118.97 crore

- Recommended Dividend: ₹5 per equity share (₹2 normal + ₹3 special)

- Exceptional Gains (FY 2025-26): ₹64.33 crore (compared to ₹545.22 crore in FY 2024-25)

- Operating Profit Margin (FY 2025-26): 9.65% (compared to 11.50% in FY 2024-25)

What to track next

Investors should monitor the company's ability to manage raw material price volatility, maintain project execution timelines, and effectively manage liquidity. The progress on land monetization and the successful integration of its EPC capabilities will be crucial for future performance.