India's steel sector saw strong volume growth in May 2026, with crude steel production at 14.2 million tonnes. However, new EU tariffs and continued imports from Asia pose challenges for domestic producers and exporters.

India Steel Sector Sees Volume Growth Amidst Trade Challenges

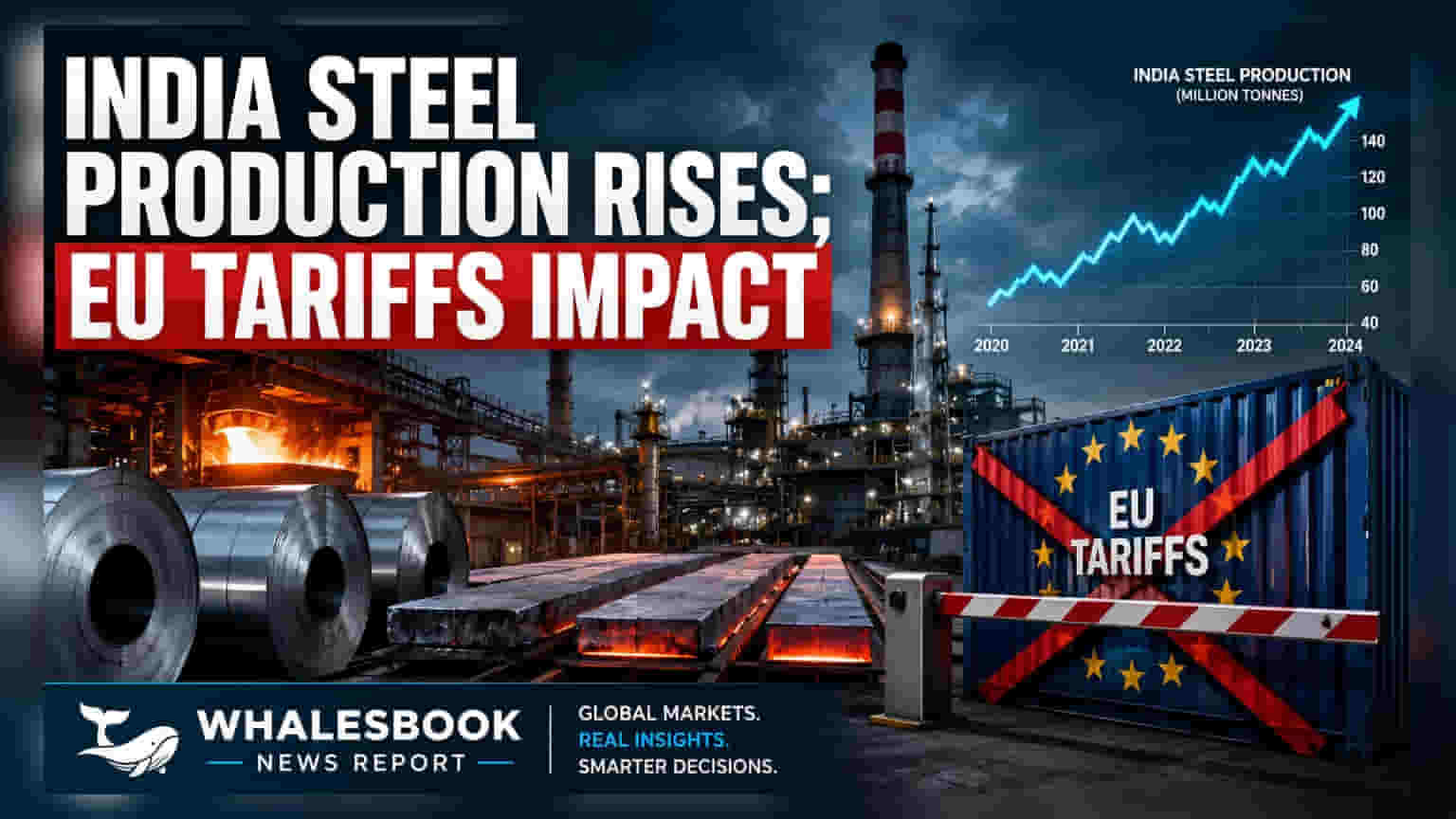

India's crude steel production reached 14.2 million tonnes in May 2026, with finished steel consumption at 14.3 million tonnes.

Reader Takeaway: Domestic demand is strong, but export markets and imports present significant headwinds.

What just happened

In May 2026, India's steel sector reported a crude steel output of 14.2 million tonnes and finished steel consumption of 14.3 million tonnes. The nation continued to be a net importer of finished steel, with 0.7 million tonnes imported during the month. Meanwhile, LME Aluminium prices stood at 3,070 USD/t in June 2026, influenced by a strengthening US dollar. Domestic HRC prices in Mumbai were 58,267 Rs/t in June 2026, supported by safeguard duties.

Why this matters

The robust domestic production and consumption figures indicate resilience in India's steel market. However, the persistent net import status highlights competitive pressures. The European Union's new country-specific tariff-rate quotas (TRQs) and Carbon Border Adjustment Mechanism (CBAM) introduce significant challenges for Indian steel exporters, potentially impacting their margins and volumes in a key market.

The backstory

The EU's trade measures, effective July-December 2026, will impose a 50% out-of-quota duty on steel exceeding defined limits. This adds to the complexity for Indian producers already navigating global commodity price fluctuations and domestic pricing influenced by safeguard duties against imports, particularly from China. LME Aluminium prices have been pressured by the US Federal Reserve's hawkish stance and a stronger dollar.

What changes now

Indian steel exporters may need to recalibrate their strategies, potentially diversifying export destinations away from the EU. Domestic producers continue to benefit from safeguard duties, which help maintain a price differential compared to landed costs of Chinese imports. Monitoring global supply changes, such as potential revisions in nickel mining quotas in Indonesia, will be crucial for anticipating future price volatility.

Risks to watch

Export limitations due to EU TRQs are a key concern, potentially restricting volume and realization for Indian exporters. The ongoing status as a net importer of finished steel continues to limit pricing power for domestic producers. Global supply dynamics, like nickel mining quota revisions, could lead to price volatility.

Peer comparison

While specific peer data for May-June 2026 is not detailed in the filing, the context points to a challenging export environment for Indian steel producers compared to markets less affected by EU protectionist measures. Domestically, producers benefit from safeguard duties which differentiate their pricing from landed costs of Chinese steel.

Context metrics (time-bound)

- May 2026: India Crude Steel Production: 14.2 million tonnes; Finished Steel Consumption: 14.3 million tonnes; Finished Steel Imports: 0.7 million tonnes.

- June 2026: LME Aluminium Price: 3,070 USD/t; India HRC Mumbai Price: 58,267 Rs/t.

- July-December 2026: EU TRQs with 50% out-of-quota duty.

What to track next

Investors should closely monitor the actual impact of EU trade regulations on Indian steel export volumes and profit margins. Tracking domestic steel price movements relative to import costs and updates on global commodity supply chains, especially nickel, will be important indicators of sector performance.