Greaves Cotton FY26: Turnaround Profit of ₹35.29 Cr on ₹3,486.61 Cr Revenue

Financial Results Update

Greaves Cotton has reported its financial results for the quarter and year ended March 31, 2026. The company achieved a turnaround in its full-year consolidated performance.

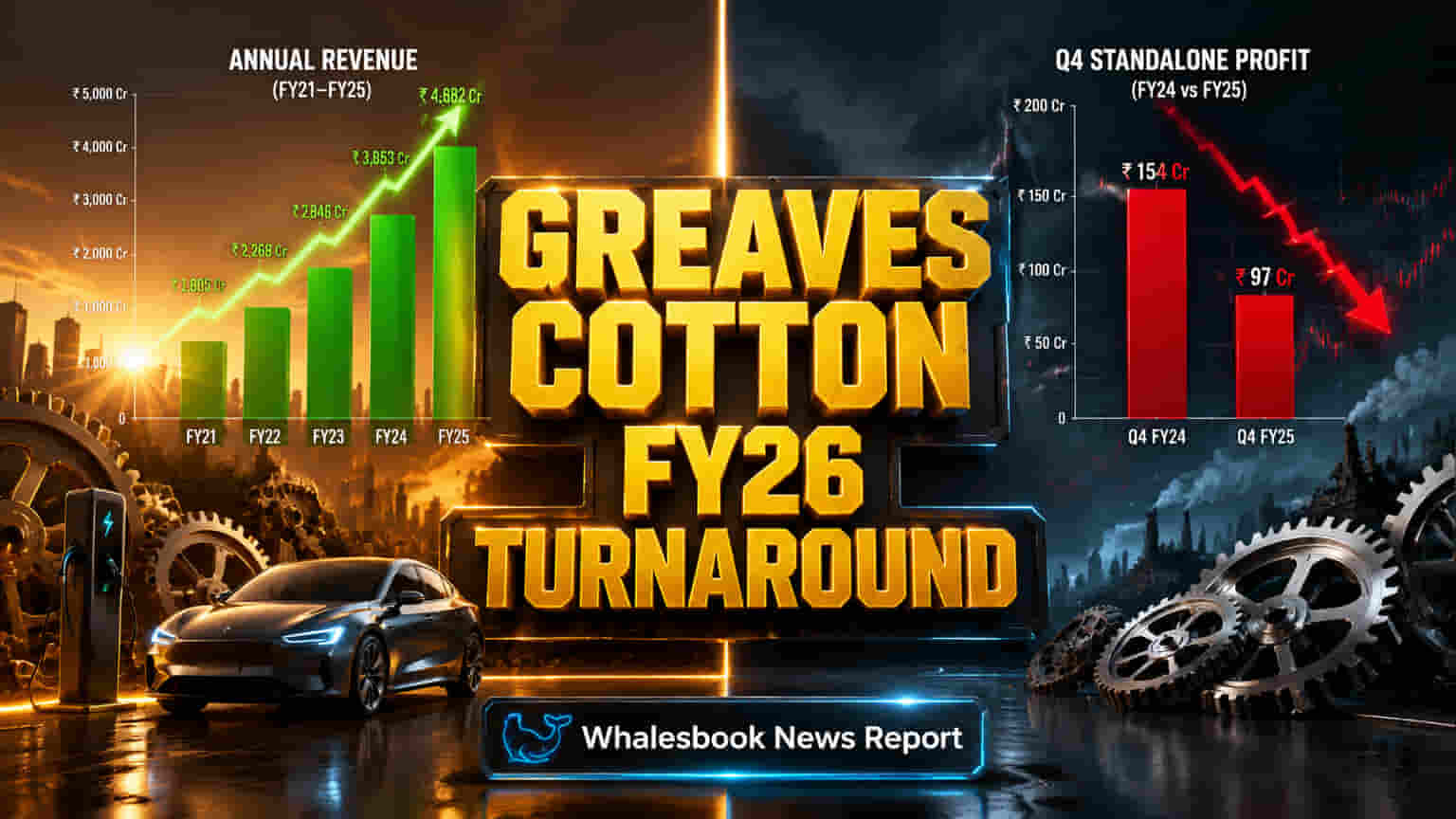

For the fiscal year 2026, consolidated total revenue grew 17.27% to ₹3,486.61 crore. This revenue growth helped the company achieve a consolidated profit of ₹35.29 crore, a significant improvement from a loss of ₹6.28 crore in the previous year.

However, the latest quarter (Q4 FY26) showed mixed results. Standalone profit declined 22.75% year-on-year to ₹47.75 crore, despite standalone revenue of ₹710.88 crore. Consolidated revenue for the quarter was ₹1,013.36 crore, with a profit of only ₹2.20 crore.

Why This Matters

The annual profit turnaround suggests successful cost controls or revenue generation strategies throughout the fiscal year, marking progress toward sustained profitability.

However, the drop in Q4 standalone profit and the low consolidated net profit raise questions about operational efficiency, subsidiary performance, and how specific provisions affected quarterly earnings.

Company Background

Greaves Cotton is an engineering conglomerate with operations spanning industrial engines and E-mobility. The company is investing in its E-mobility segment, notably through subsidiary Ampere Electric, to tap into the electric vehicle market. Historically, Greaves Cotton has reviewed its business units to improve profitability and streamline operations.

Key Developments

Shareholders will receive a recommended final dividend of Rs 2 per share, reflecting the improved annual performance.

This turnaround signals potential for future growth, provided the company can maintain revenue momentum and improve profitability in its subsidiaries.

Given recent provisions and increased debt, investors may expect a stronger focus on margin improvement.

Key Risks and Provisions

An impairment provision of ₹15.98 crore was recognized due to adverse changes in project execution and customer demand, affecting quarterly results.

Consolidated non-current borrowings increased significantly to ₹275.58 crore from zero in the prior year, adding to the company's debt load.

Consolidated profitability remains thin compared to the standalone entity, suggesting potential underperformance or high operational costs within subsidiary units.

A provision of ₹19.26 crore was set aside for the implementation of new Labour Codes.

Industry Context

Competitors such as Cummins India and Ashok Leyland operate in similar industrial engine and commercial vehicle markets. Cummins India typically shows strong profitability, while Ashok Leyland's engine division performance is linked to commercial vehicle market cycles.

Greaves Cotton's turnaround should be assessed within a competitive environment where operational efficiency and market demand are key factors.

Key Financial Metrics

Key figures show consolidated revenue for FY26 reached ₹3,486.61 crore, an increase from ₹2,973.10 crore in FY25. In the fourth quarter of FY26, standalone profit was ₹47.75 crore, down from ₹61.81 crore in the prior year's quarter. Additionally, consolidated non-current borrowings rose to ₹275.58 crore in FY26.

What to Watch Next

Investors will be watching the company's strategy for managing its increased debt and consolidated borrowings. Performance and profitability of subsidiary units, particularly in the E-mobility segment, will be key. Management commentary is also anticipated regarding the reasons for the Q4 standalone profit dip, the impact of new Labour Codes, and the sustainability of the annual profit turnaround going forward.