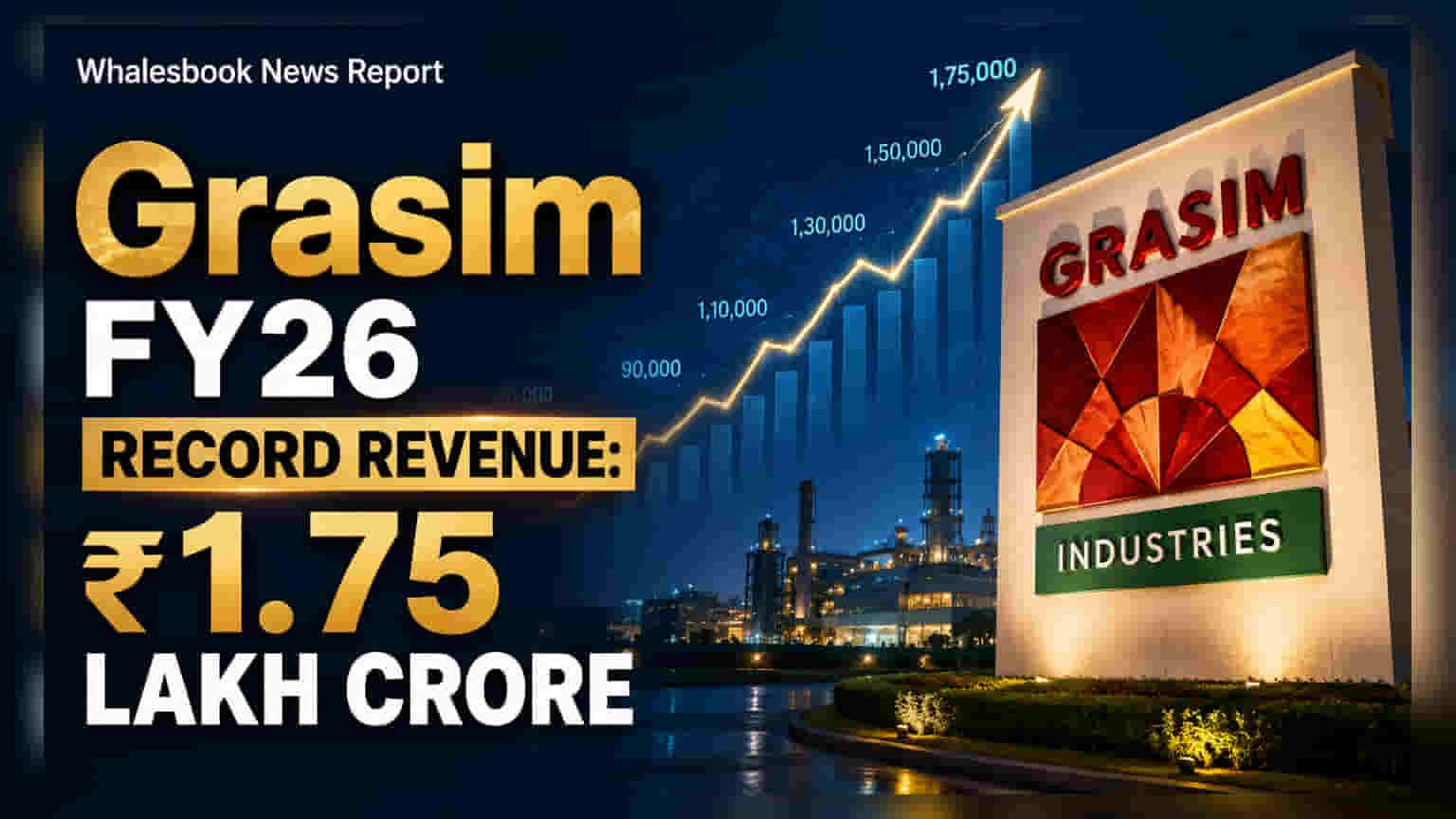

Grasim Industries reported a record-breaking FY26 with consolidated revenue of ₹1,75,431 crore, an 18% year-on-year jump. EBITDA grew 29% to ₹25,872 crore. The company highlighted strong performance in paints, B2B e-commerce, and cement, signaling a shift towards asset utilization and cash flow generation.

Grasim Industries Records Stellar FY26 Performance with Record Revenue

Consolidated Revenue: ₹1,75,431 crore (18% YoY growth)

Consolidated EBITDA: ₹25,872 crore (29% YoY growth)

Reader Takeaway: Strong growth driven by diversified businesses, now focusing on cash flow generation post-capex.

What just happened

Grasim Industries announced its financial results for Fiscal Year 2025-26, marking a period of record performance. The company achieved consolidated revenue of ₹1,75,431 crore, an 18.15% increase from the previous year. Consolidated EBITDA saw a significant jump of 29.21%, reaching ₹25,872 crore. The standalone business also showed robust growth, with revenue up 30.02% to ₹41,039 crore.

Why this matters

This performance highlights Grasim's operational strength and successful expansion across its diverse portfolio. The company's strategic focus is now shifting from heavy capital expenditure, particularly in the paint business, towards optimizing asset utilization and generating free cash flow. This transition is crucial for long-term shareholder value.

The backstory

Grasim Industries, a flagship company of the Aditya Birla Group, has been undertaking a significant investment cycle. Over the past five years, it has invested nearly ₹74,000 crore in capital expenditure, notably in developing its paints business (Birla Opus) and B2B e-commerce platform (Birla Pivot).

What changes now

With the major investment phase for new ventures nearing completion, Grasim's management plans to concentrate on maximizing the efficiency of its existing assets and accelerating free cash flow generation. This strategic pivot indicates a move towards optimizing profitability and strengthening the balance sheet.

Risks to watch

Potential risks identified include global macroeconomic headwinds, such as geopolitical tensions and inflationary pressures. In its commodity businesses, particularly chemicals, the company faces margin pressures due to global oversupply and intense competition.

Peer comparison

While not explicitly detailed in the filing, Grasim's diversified nature allows it to weather sector-specific downturns. Its paint business, Birla Opus, has rapidly gained market share, aiming to become a significant player. UltraTech Cement, a subsidiary, continues its global expansion, already crossing 200 MTPA capacity.

Context metrics (time-bound)

- Birla Opus (Paints) achieved a 10% market share by revenue in March 2026.

- Birla Pivot (B2B E-commerce) reached ₹8,500 crore in revenue, ahead of schedule.

- UltraTech Cement surpassed 200 MTPA grey cement capacity in April 2026.

- Net Debt-to-EBITDA ratio (excluding financial services) stood at 1.43x.

What to track next

Investors should closely monitor Grasim's ability to translate its scaled-up operations into sustained profitability and robust free cash flow generation. Continued vigilance on commodity price cycles and global economic stability remains important.