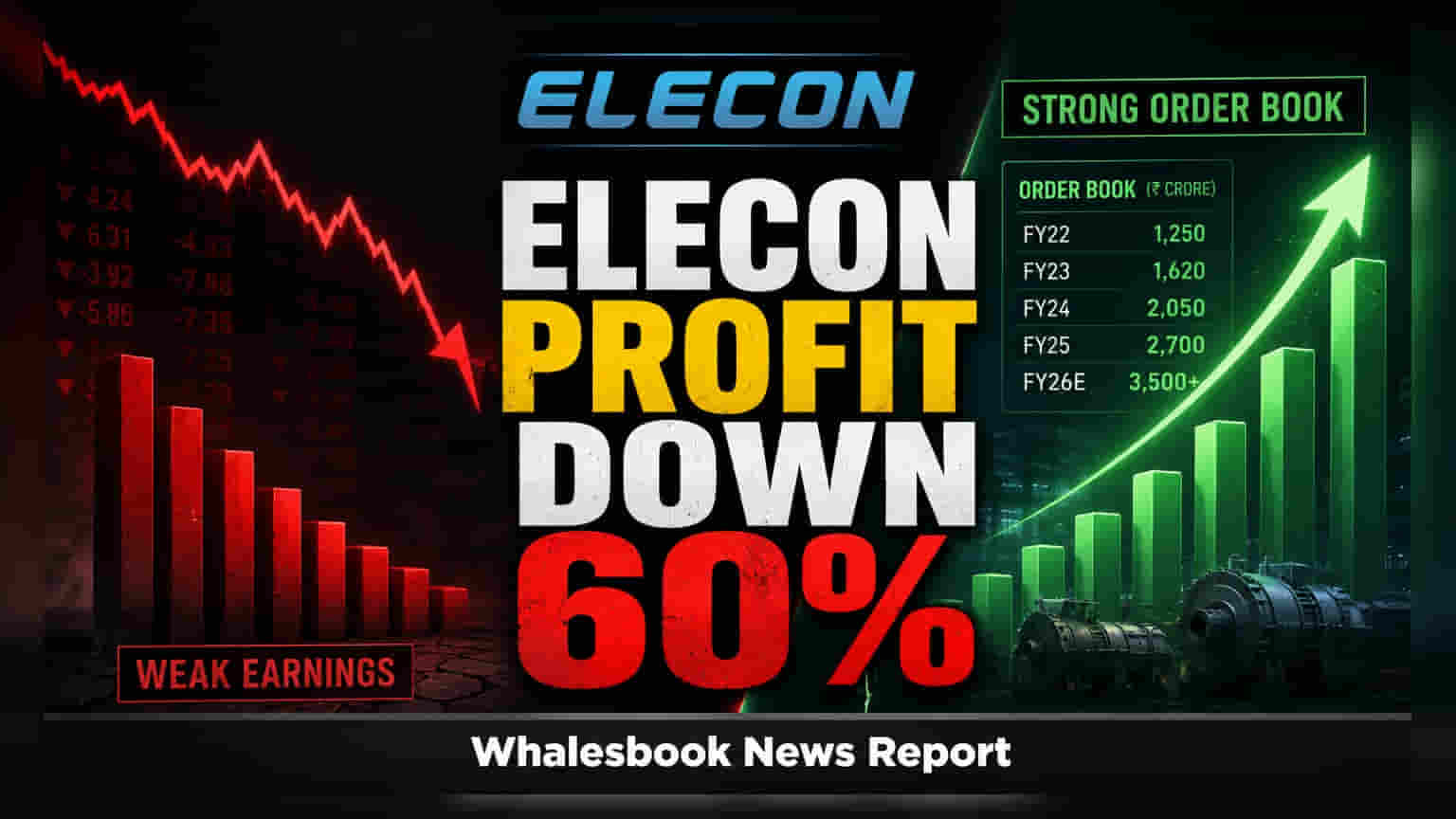

Elecon Engineering reported a 60% year-on-year drop in net profit to ₹70 crore for Q1 FY27. While revenue grew 6% to ₹521 crore, profit margins contracted due to an adverse product mix and higher raw material costs.

Elecon Engineering Reports 60% Profit Decline in Q1 FY27

Elecon Engineering's net profit for the first quarter of FY27 plummeted by 60% year-on-year to ₹70 crore. This decline comes despite a 6% rise in revenue, which reached ₹521 crore.

Reader Takeaway: Order book strength faces margin compression and execution delays.

What just happened

Elecon Engineering's financial results for Q1 FY27 showed a significant drop in profitability. Revenue increased by 6% to ₹521 crore, driven by the Gear division. However, EBITDA fell 16% to ₹109 crore, and net profit declined 60% to ₹70 crore compared to the previous year.

The company's EBITDA margin compressed to 21.0% from 26.6% in Q1 FY26. This was attributed to an unfavorable product mix and increased raw material costs, particularly affecting the Material Handling Equipment (MHE) division.

Why this matters

The substantial decrease in net profit and margin contraction indicates immediate challenges impacting the company's bottom line. Investors will be closely watching the company's ability to manage costs and improve product mix to recover profitability.

The backstory

In the previous fiscal year, Elecon Engineering had shown robust performance. However, the current quarter's results highlight a shift in operational dynamics, with macroeconomic uncertainties and execution hurdles becoming more prominent.

What changes now

Elecon Engineering has adopted a conservative outlook for FY27. The company is targeting low double-digit revenue growth and aims to maintain FY26 levels for EBITDA margins, with specific targets for its Gear and MHE divisions. Management remains optimistic about achieving a ₹5,000 crore topline by FY30.

Risks to watch

Key risks include ongoing macroeconomic uncertainties, near-term execution constraints, and the ability to recover margin compression in the MHE segment. The company's success will depend on navigating these challenges effectively.

Peer comparison

While specific peer comparison data is not provided in the filing, the results suggest that Elecon Engineering is facing industry-wide cost pressures and execution challenges.

Context metrics (time-bound)

- Revenue: ₹521 crore (+6% YoY)

- EBITDA: ₹109 crore (-16% YoY)

- Net Profit: ₹70 crore (-60% YoY)

- EBITDA Margin: 21.0% (vs 26.6% in Q1 FY26)

- Consolidated Order Book: ₹1,518 crore (+37% YoY)

- Quarterly Order Inflows: ₹755 crore (+23% YoY)

What to track next

Investors should monitor the company's performance in subsequent quarters, focusing on improvements in EBITDA margins, the execution of its order book, and the recovery of the MHE segment. The company's expansion into international markets will also be a key factor to track.