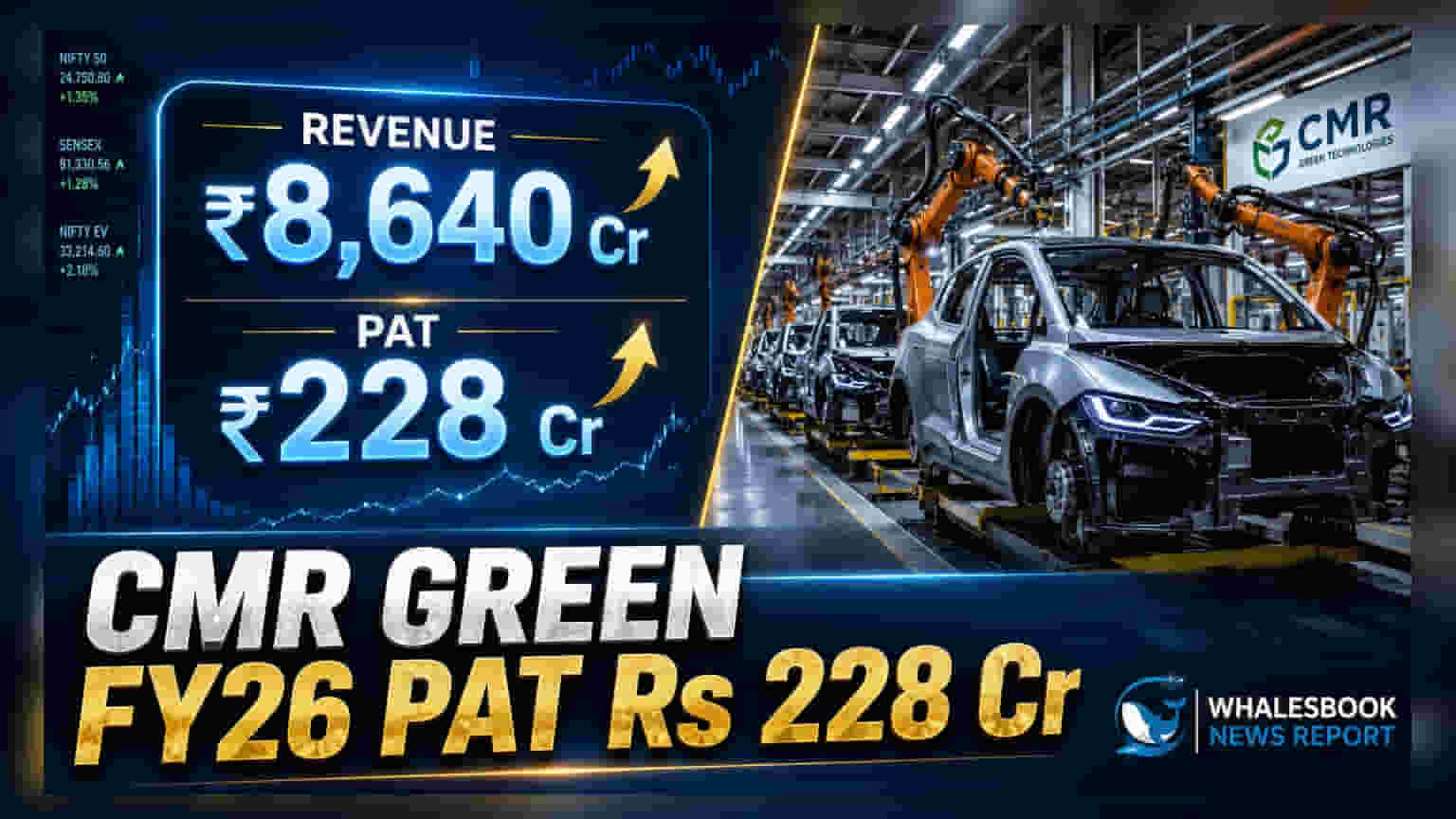

CMR Green Technologies reported strong performance for FY26, with revenue reaching INR 8,640 crore and Profit After Tax at INR 228 crore. The company saw a 24% volume growth and is investing INR 200 crore in capex for EV and diversification.

CMR Green Technologies Reports Strong FY26 Performance

CMR Green Technologies has announced its financial results for Fiscal Year 2026, with revenue reaching INR 8,640 crore and Profit After Tax (PAT) at INR 228 crore. The company also reported a Q4 FY26 PAT of INR 65.68 crore. Reader Takeaway: Volume growth and EV focus offer upside; managing aluminum price volatility is a key pressure point. ## What just happened CMR Green Technologies posted robust financial figures for FY26. Revenue stood at INR 8,640 crore, with EBITDA at INR 449 crore. For the fourth quarter of FY26, revenue was INR 2,364 crore and EBITDA was INR 128 crore. The company achieved a total volume of 80,381 metric tons in FY26, marking a significant 24% year-on-year increase. This growth was driven by a 27% rise in the Aluminum Segment and an 18% increase in the Non-Ferrous Segment. ## Why this matters These results indicate strong operational execution and demand for the company's products, particularly with the significant volume growth. The company's strategic investments in the EV sector and diversification into areas like beverage can recycling and green billets signal a forward-looking approach to capture emerging market opportunities and de-risk its revenue streams. ## The backstory CMR Green Technologies has been focusing on expanding its capacity and diversifying its product portfolio. The emphasis on EBITDA per ton, rather than percentage margins, highlights a focus on operational efficiency and profitability at a unit level. The company's strategy to mitigate aluminum price volatility through a geographically diversified sourcing approach is a key element of its financial management. ## What changes now The company plans a capital expenditure of INR 200 crore in FY27 to expand its installed capacity from 6.15 lakh metric tons to 7 lakh metric tons. New facilities in Shoolagiri and Bawal are being developed to cater to the growing demand from the electric vehicle (EV) industry. Expansion into beverage can recycling and green billets for construction and solar industries are also part of the growth strategy. ## Risks to watch While the company sources aluminum from six continents to manage price volatility, global scrap supply challenges and potential export restrictions remain risks. The mark-to-market impact on hedge contracts, reflected in Other Comprehensive Income (OCI), is a normal hedging process but can impact reported financials. ## Context metrics (time-bound) * FY26 Revenue: INR 8,640 crore * FY26 EBITDA: INR 449 crore * FY26 PAT: INR 228 crore * FY26 Total Volume: 80,381 metric tons (24% growth) * Q4 FY26 Revenue: INR 2,364 crore * Q4 FY26 EBITDA: INR 128 crore * Q4 FY26 PAT: INR 65.68 crore * FY26 EBITDA per ton: INR 11,000 * Q4 FY26 EBITDA per ton: INR 11,400 * FY27 Budgeted Capex: INR 200 crore * Current Installed Capacity: 6.15 lakh metric tons per annum * Target Capacity by FY27 end: 7 lakh metric tons per annum * Carbon Credits Stock (as of July 2026): 2.73 lakh tons ## What to track next Investors will be looking at the successful ramp-up of the new capacities in Shoolagiri and Bawal, the company's ability to maintain volume growth, and its progress in diversifying into new product segments. Monitoring the global scrap supply situation and the eventual monetization of carbon credits will also be crucial.