Banswara Syntex reported a 5% rise in revenue to ₹1,355.78 crore and a 33% jump in profit after tax to ₹28.40 crore for FY26. The company recommended a dividend of ₹1 per share.

Banswara Syntex Reports Strong FY26 Performance with Revenue Growth and Profit Surge

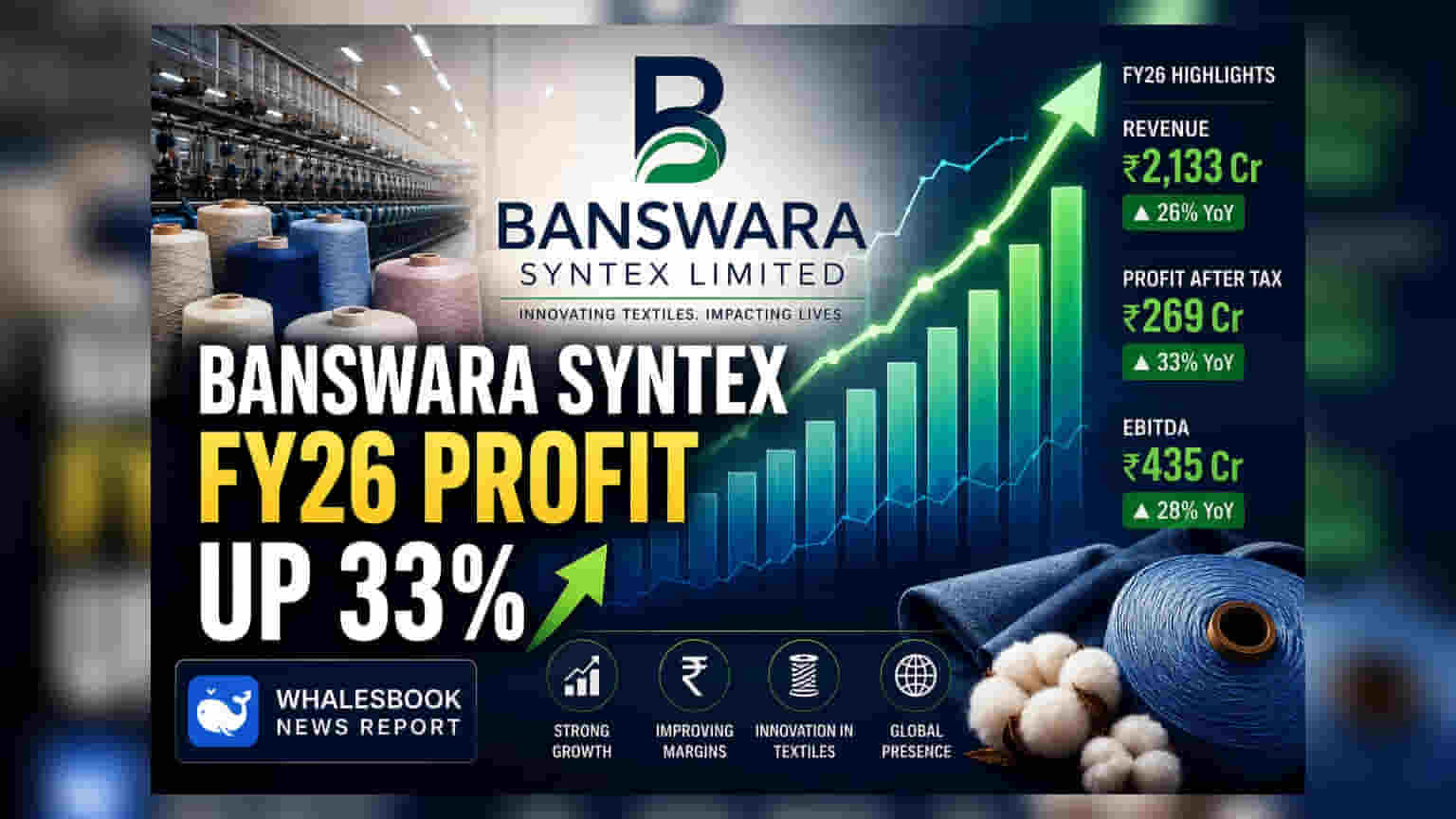

Revenue from Operations: ₹1,355.78 crore Profit After Tax: ₹28.40 crore Reader Takeaway: Top and bottom-line growth alongside export strength provide a positive outlook, though raw material costs remain a watch point. ## What just happened Banswara Syntex Ltd announced its financial results for the fiscal year ending March 31, 2026 (FY26). The company reported a revenue from operations of ₹1,355.78 crore, a 4.96% increase from ₹1,291.70 crore in the previous fiscal year (FY25). Profit After Tax (PAT) saw a significant jump of 32.77%, reaching ₹28.40 crore compared to ₹21.39 crore in FY25. Basic Earnings Per Share (EPS) improved to ₹8.30 from ₹6.25. The company also highlighted its export performance, with export turnover growing to ₹631.51 crore from ₹569.48 crore, representing 47% of total turnover, up from 44% in the prior year. ## Why this matters The financial performance indicates Banswara Syntex's ability to grow its business and enhance profitability. The increase in PAT and EPS suggests improved operational efficiency or better sales realisation. The growing contribution of exports to revenue diversification is a positive sign for its market reach. ## The backstory Banswara Syntex has been focusing on expanding its production capacity and modernizing its facilities. The company's strategy involves concentrating on higher-value product segments to drive future growth. Exports have consistently been a strong contributor to its financial results. ## What changes now Effective August 7, 2025, the company saw a leadership transition. Mr. Ravindrakumar Toshniwal moved from Managing Director to Vice Chairman, while Mr. Shaleen Toshniwal transitioned from Joint Managing Director to Managing Director. The Board has recommended a dividend of ₹1 per equity share for FY26, which is consistent with the previous year's payout. ## Risks to watch Management commentary points to ongoing risks related to the volatility of raw material prices, including cotton, man-made fibres, dyes, and chemicals. Energy and logistics costs also continue to put pressure on operating margins, which investors should monitor. ## Peer comparison (No specific peer comparison data was provided in the filing.) ## Context metrics (time-bound) * **Revenue from Operations:** ₹1,355.78 crore (FY26) vs ₹1,291.70 crore (FY25), a 4.96% increase. * **Profit After Tax:** ₹28.40 crore (FY26) vs ₹21.39 crore (FY25), a 32.77% increase. * **Export Turnover:** ₹631.51 crore (FY26) vs ₹569.48 crore (FY25), a 10.91% increase. * **Export Share:** 47% of total turnover (FY26) vs 44% (FY25). ## What to track next Investors will be keen to observe how Banswara Syntex manages raw material and energy cost pressures in the upcoming quarters. The company's ability to sustain growth in high-value segments and capitalize on export opportunities will be crucial. The effectiveness of the new leadership in steering the company will also be a key factor.

Disclaimer:This article is published for informational purposes only. While reasonable efforts are made to ensure accuracy, completeness, and timeliness, readers are encouraged to independently verify information before making any decisions based on the content. The views and information presented are subject to editorial review and may be updated without notice.