Godrej Consumer Products expects high-teens consolidated revenue growth in Q1 FY27, surpassing full-year guidance. International markets like Indonesia and GAUM show strong performance, but input cost volatility pressured margins.

Godrej Consumer Products Q1 FY27 Update

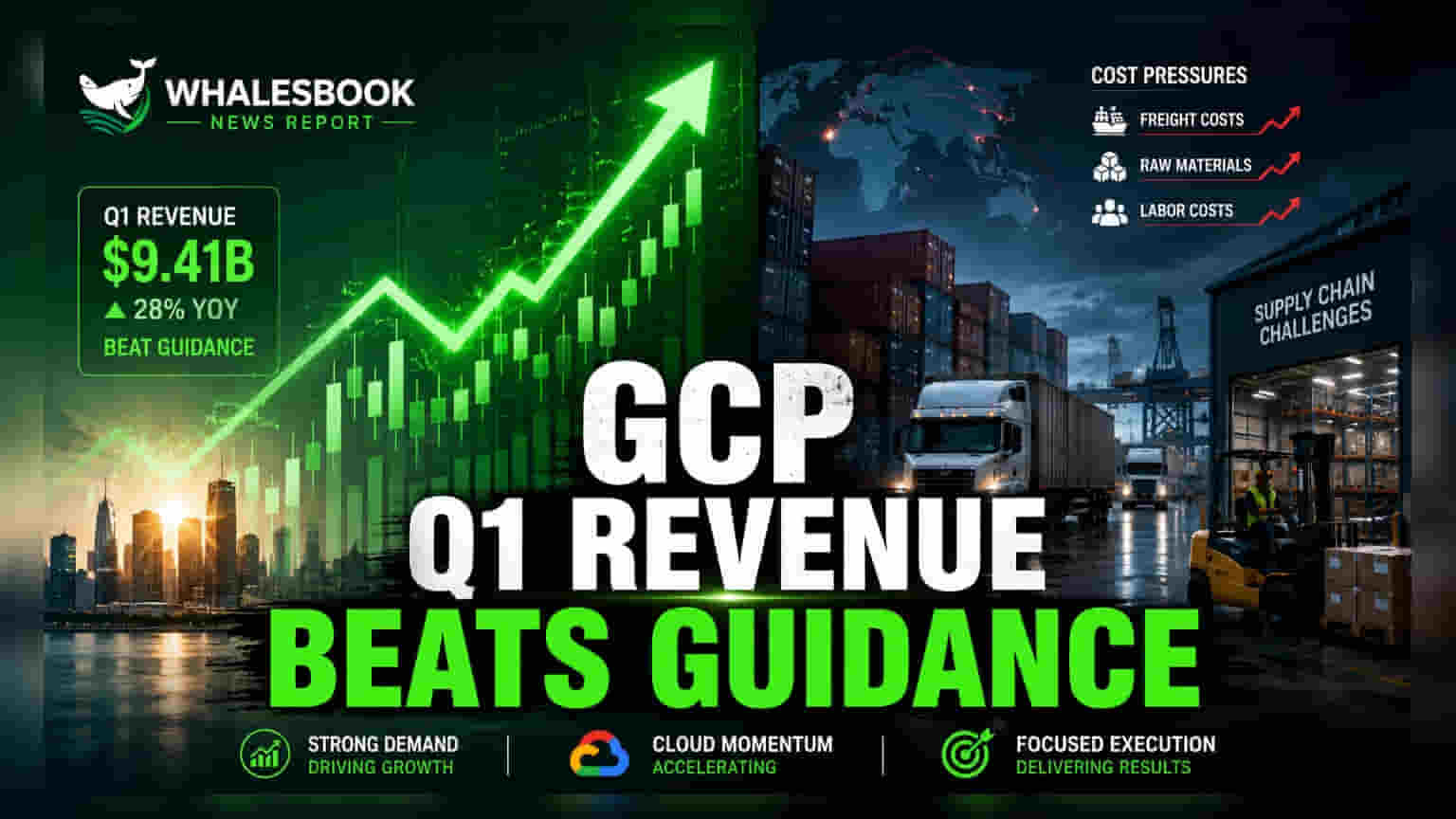

Consolidated revenue growth expected high-teens; Consolidated volume growth high single-digit.

Reader Takeaway: Strong revenue growth driven by international markets, but raw material costs pressured margins.

What just happened

Godrej Consumer Products (GCP) has provided a Q1 FY27 business update indicating strong top-line performance. The company anticipates consolidated revenue to grow in the high-teens, significantly exceeding its full-year double-digit guidance. This growth is supported by high single-digit underlying volume growth.

The standalone business also posted expected double-digit revenue growth with similar volume expansion, showing broad-based strength across its categories.

Why this matters

This update signals a robust start to the fiscal year for GCP, with growth momentum outpacing initial expectations. Strong performance in key international markets like Indonesia and the GAUM (Godrej Africa, USA, and Middle East) region highlights effective market penetration and strategy execution in these areas.

The backstory

GCP has been focusing on strengthening its presence in emerging markets and optimizing its product portfolio. The company's strategy involves leveraging growth in countries like Indonesia and expanding its reach in Africa, the USA, and the Middle East.

What changes now

The company is now positioned to potentially exceed its full-year financial targets. Management is implementing calibrated pricing actions and cost-saving measures to counter input cost pressures, which began to ease towards the end of the quarter. The focus will be on sustaining volume growth while managing margin recovery.

Risks to watch

Elevated raw material costs, particularly crude oil volatility, impacted margins and caused supply chain challenges like lower fill rates during the quarter. Potential El Niño conditions could also introduce weather volatility, affecting agricultural output and rural demand, although GCP's diversified sourcing offers some resilience.

Peer comparison

While specific peer results for Q1 FY27 are not yet available, GCP's performance shows strong regional execution. Other FMCG companies may face similar challenges with input cost inflation and weather-related demand fluctuations.

Context metrics (time-bound)

- Consolidated Revenue Growth (Q1 FY27): High-teens (Ahead of full-year guidance)

- Standalone Revenue Growth (Q1 FY27): Double-digit

- Consolidated Volume Growth (Q1 FY27): High single-digit

- Indonesia Revenue Growth (Q1 FY27): Mid-teens

- GAUM Sales Growth (Q1 FY27): Strong double-digit

What to track next

Investors will be keen to see margin recovery in subsequent quarters as input costs stabilize. Monitoring rural demand trends and the effectiveness of GCP's pricing and cost-saving strategies will be crucial.