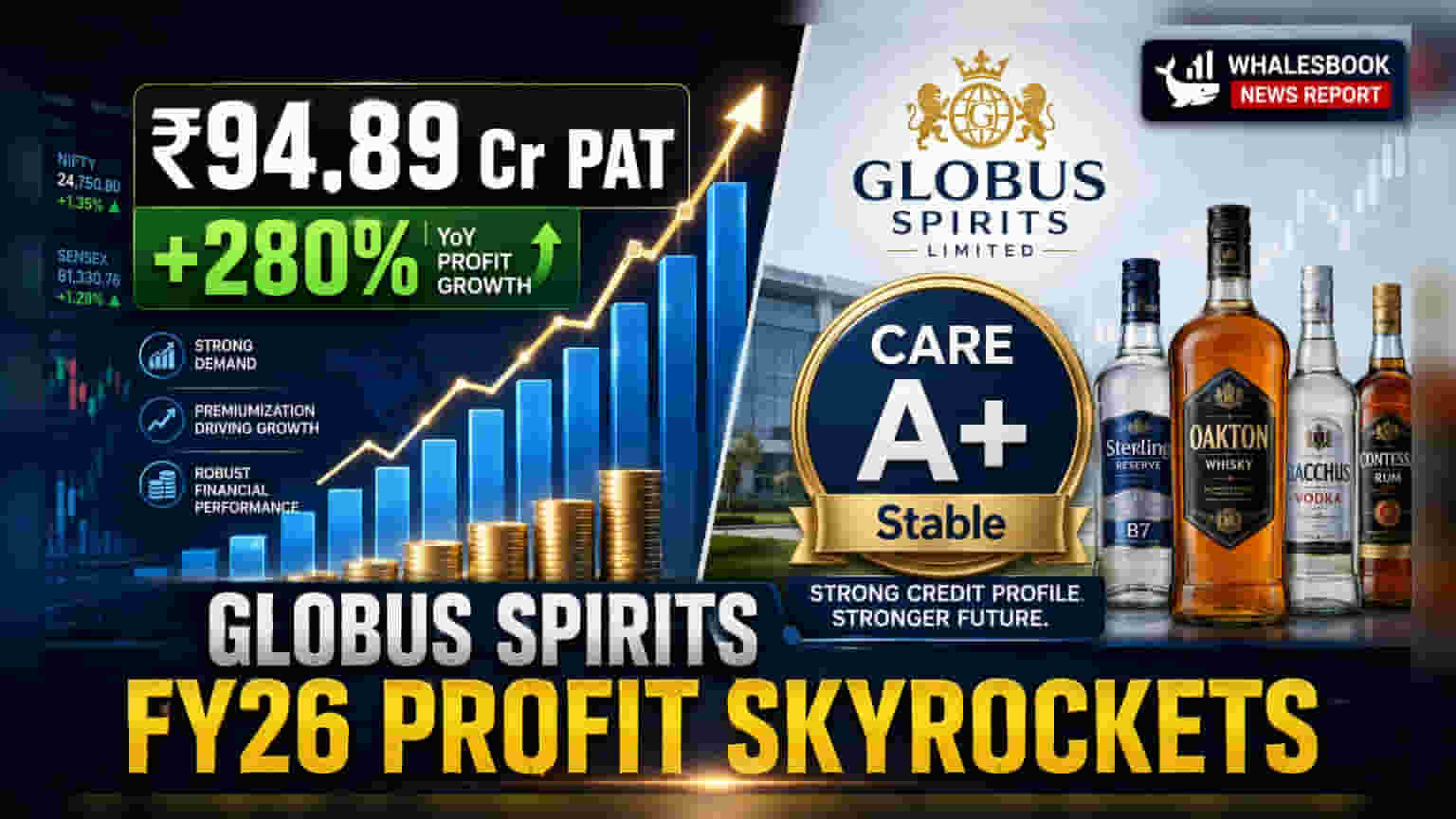

Globus Spirits reported a robust 280% surge in FY26 Profit After Tax (PAT) to ₹94.89 crore. The company's credit rating was reaffirmed at CARE A+ (Stable). This financial improvement is driven by higher capacity utilization and price hikes.

Globus Spirits FY26 Performance Boosted by Margin Expansion

Globus Spirits reported a Profit After Tax (PAT) of ₹94.89 crore for FY26, a significant jump of 279.9% from ₹24.97 crore in the previous year. Total Operating Income grew by 6.3% to ₹2,702.74 crore.

Reader Takeaway: Higher margins and debt reduction show operational strength; watch the loss-making P&A segment.

What just happened

Globus Spirits announced its financial results for FY26, revealing a substantial increase in profitability. Profit After Tax (PAT) rose by 279.9% to ₹94.89 crore, while Total Operating Income saw a 6.3% growth, reaching ₹2,702.74 crore. The company's credit rating was also reaffirmed at CARE A+ (Stable) and A1+ for short-term debt.

Why this matters

This financial performance indicates a significant turnaround for Globus Spirits, with improved efficiency and profitability. The reaffirmation of credit ratings suggests financial stability and confidence from rating agencies, which is crucial for future funding and investor sentiment.

The backstory

The company's core business of Bulk Alcohol & R&O contributed about 94% of its total turnover in FY26. This segment saw revenue grow by approximately 7% to around ₹1,644 crore, supported by a 6% increase in sales volume.

What changes now

Globus Spirits is planning a Qualified Institutional Placement (QIP) to raise up to ₹500 crore, with an initial target of ₹150 crore by Q2FY27. These funds are earmarked for debt repayment and working capital, which is expected to further strengthen the balance sheet and improve financial metrics.

Risks to watch

While the company shows strong operational improvements, the Prestige and Above (P&A) segment continues to be a concern, operating at a loss of -6% margin despite revenue growth. The highly regulated nature of the alcohol industry also poses a risk, with potential impacts on profitability due to input price volatility and limited pricing power.

Peer comparison

Information not available in the filing.

Context metrics (time-bound)

- PBILDT Margin: Expanded to 9.64% in FY26 from 6.06% in FY25.

- PAT Margin: Improved to 3.51% in FY26 from 0.98% in FY25.

- Overall Gearing: Improved to 0.66x in FY26 from 0.79x in FY25.

- Interest Coverage: Increased to 4.45x in FY26 from 3.30x in FY25.

- Capacity Utilization: Increased to 80% in FY26 from 74% in FY25.

What to track next

Investors should closely monitor the turnaround of the P&A segment, the success and execution of the planned QIP, and the full-year impact of the new Uttar Pradesh plant on FY27 revenues.